Recently, the price of Bitcoin has fluctuated violently around the $100,000 mark, especially after it surged to $104,000 last week, it crashed to $90,500, which was considered by many to be a signal of peak sentiment and loosening of chips. Some institutional investors who have made huge profits have begun to choose to gradually withdraw. For example, Meitu has liquidated all its crypto assets, and the market is worried that this wave of profit-taking may accelerate.

While market sentiment was generally bearish, MicroStrategy bucked the trend and announced on Monday that it had bought another $2.1 billion worth of Bitcoin. This aggressive strategy, while giving the market a shot in the arm, also sparked controversy about the sustainability of its investment strategy. The market is concerned that if the price of Bitcoin continues to fall sharply, MicroStrategy may get into trouble, triggering a black swan event that affects the entire crypto market.

MicroStrategy: Bitcoin holding giant and market activist

As the listed company with the most Bitcoin in the world, MicroStrategy's strategy has always attracted much attention. Data shows that the current circulation of Bitcoin is increasingly concentrated in the hands of a few large institutions. The top five Bitcoin holding entities other than Satoshi Nakamoto control a total of 9.9% of the circulation. Among them, Coinbase holds 1.12 million BTC, worth more than US$112 billion; Binance holds 687,000 BTC, worth nearly US$68.9 billion; BlackRock, Microstrategy and Bitfinex also rank third to fifth respectively. In addition to Satoshi Nakamoto, the top ten holding entities currently control about 14.82% of the total circulation of Bitcoin. The holdings of these institutions directly affect the trend of the market.

Compared with other institutions, MicroStrategy's investment strategy is particularly aggressive. If the rise of Bitcoin in the $40K-70K range is due to the promotion of ETFs, then the rise in the $70K-100K range is inseparable from the promotion of MicroStrategy. MicroStrategy is known as the "perpetual financing machine", and its strategy of increasing positions has played a key role in the rise of Bitcoin prices.

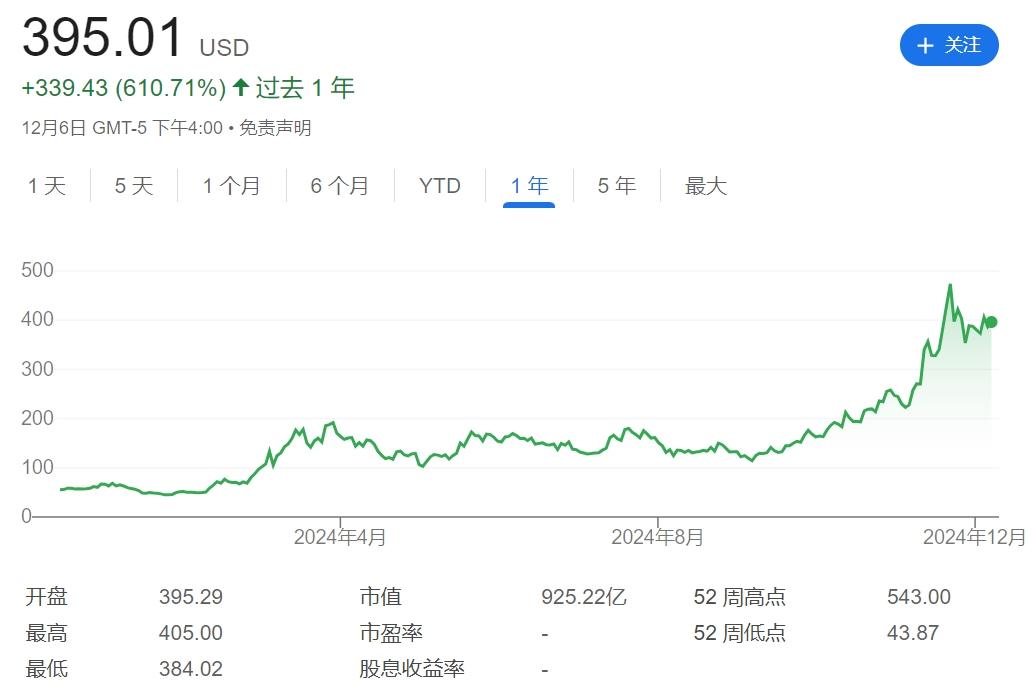

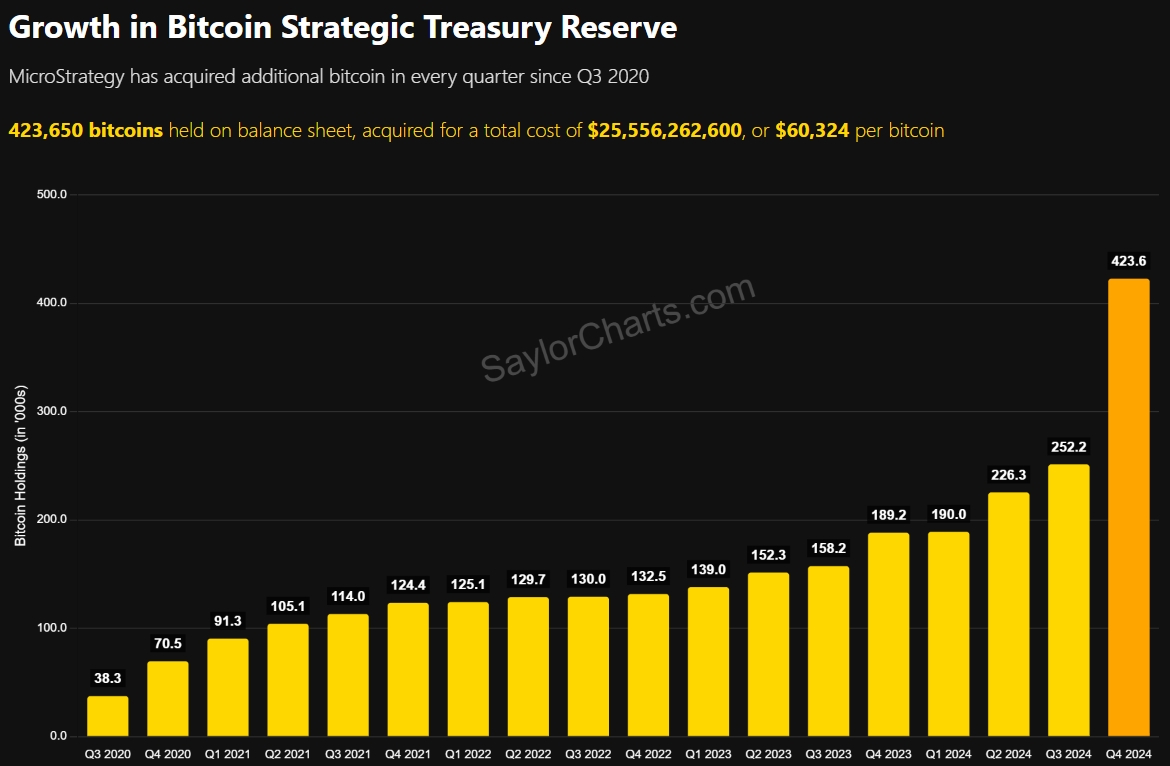

MicroStrategy's goal is to use prudent leverage to acquire as much BTC as possible, increase its stock price, and outperform Bitcoin itself. As of December 8, 2024, MicroStrategy holds a total of 423,650 bitcoins, with a cumulative investment of approximately US$25.6 billion and an average cost of US$60,324. So far this year, its quarterly BTC yield has reached 43.2%, and its year-to-date yield is 68.7%. At the same time, MicroStrategy's stock price has far outperformed Bitcoin, rising 613% this year, becoming the most powerful "Bitcoin shadow stock."

MicroStrategy's Unlimited Funds Model

MicroStrategy (MSTR) is a software company listed on the US stock market. It started all in BTC in 2020. Initially, it purchased Bitcoin through its own cash flow, and later mainly raised funds through the issuance of convertible senior notes, and continued to purchase Bitcoin on a large scale. These notes usually have fixed maturity dates and low interest rates. As the price of Bitcoin rises, the value of MSTR's Bitcoin assets increases, thereby pushing up its stock price, forming a positive feedback loop. Through continuous debt issuance and Bitcoin purchases, MSTR has established a self-reinforcing funding chain.

MSTR's financing model has the characteristics of low risk and high return. The convertible note is essentially equivalent to a contract with a free call option superimposed on it. For creditors, this is a sure-win business: if Bitcoin falls and MSTR has money, creditors can get cash back; if Bitcoin falls and MSTR has no money, creditors can still have a final guarantee, that is, convert it into stocks to cash out and recover their capital; if Bitcoin rises, MSTR will rise, and the stock exchange can be executed, and creditors can get more stock returns. The worst result is that if MSTR goes bankrupt, they are still "more senior" than common stocks, and holders will benefit first in bankruptcy or liquidation events.

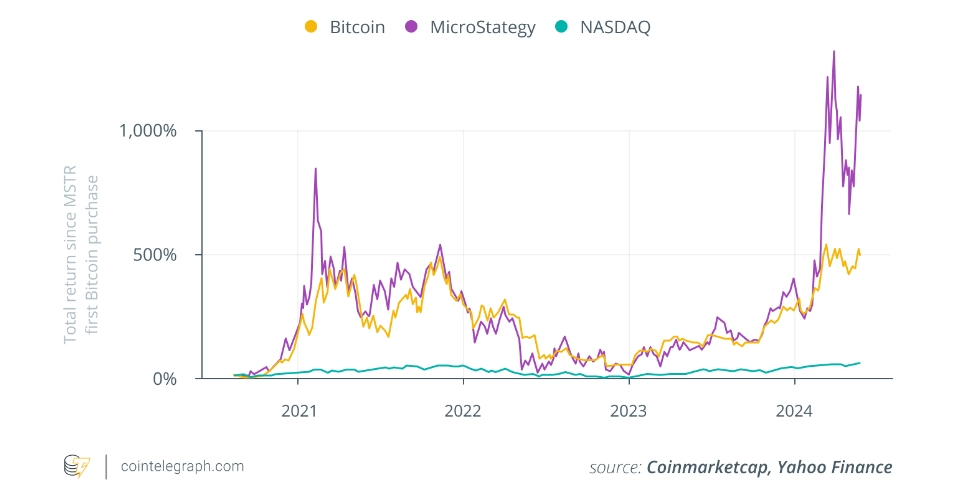

MSTR's strategy has been a huge success. Since the company went all-in on Bitcoin, its stock price has skyrocketed, with an annualized return of 80%. The stock has risen more than 2,600% since August 2020, and its current market value is nearly $93 billion, far outperforming Bitcoin itself and all other major US stocks.

The outstanding performance puts MSTR on a path of unremittingly attracting global capital and investing in Bitcoin. On October 30, while announcing its third-quarter report, MSTR announced a "21/21 Plan", which is to raise $42 billion through $21 billion in equity and $21 billion in notes in the next three years to buy more Bitcoin. So far in November, MSTR has invested approximately $13.5 billion in increasing its holdings of BTC through this model, accounting for 32% of the total funds of the "21/21 Plan", showing the market's strong confidence in MSTR.

Will MicroStrategy become the black swan in the cryptocurrency world?

In recent years, the crypto market has experienced many fluctuations and dramatic crashes, especially the bankruptcies of Luna and FTX, which have made investors particularly sensitive to the risks of similar companies.

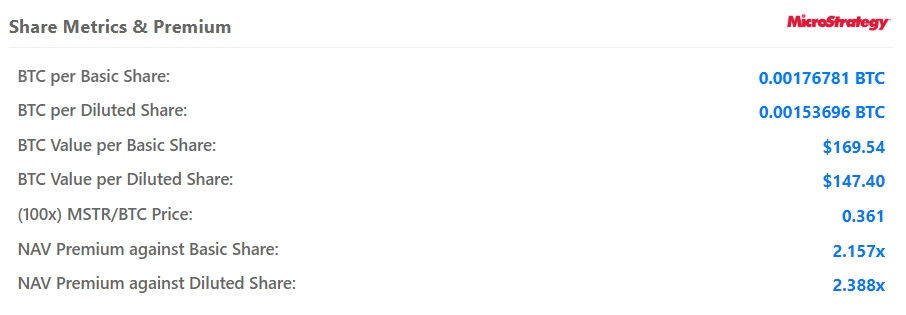

MSTR's current market value is $93 billion, about 2.2 times its Bitcoin holdings (Q3 main business revenue was only $116.1 million). When Bitcoin rises, the stock price soars, and the financing capacity is strong, which can form a positive cycle. However, once the Bitcoin price enters a volatile phase or falls, it will continue to erode the market's confidence in the subsequent BTC price development, thereby affecting the stock price, which will turn into doubts about MSTR's financing ability. Under the resonance of these two, MSTR's positive premium will converge quickly. This valuation difference is also the reason why Citron and other funds short MSTR stocks.

As we all know, leverage is a double-edged sword. If the price of BTC falls, the worst outcome for MSTR may be that it has to sell its Bitcoin holdings to repay its debts, thus triggering a "vicious death spiral". Fortunately, MSTR's debt is unsecured and does not directly rely on its Bitcoin holdings. Although the company once issued notes collateralized by Bitcoin, these notes have been fully repaid as of the third quarter of 2024. In addition, its earliest debt maturity date is February 2027, and there is no major debt repayment pressure in the short term.

In terms of annual interest repayment, MSTR's total debt is currently approximately US$7.3 billion, with an average interest rate of only 0.476%. The annual interest expenditure is approximately US$34.6 million, and the cost is relatively controllable.

That is to say, MSTR borrowed OTC leverage and had no liquidation mechanism. In theory, even if MSTR's stock price was smashed to zero, it still did not need to be forced to sell these bitcoins. However, for Michael Saylor, CEO of MSTR, the long-term value of the company is far higher than the value of the BTC he holds. After several rounds of additional issuance, his equity ratio is not high at present. Assuming that the company faces bankruptcy and liquidation, he can't get much BTC, which forces him to assume the responsibility of its market value management. When MSTR's price-to-earnings ratio is undervalued due to panic, it is a cost-effective operation to sell BTC in exchange for funds and repurchase MSTR from the market.

Whether MSTR is a guardian or a risk maker of Bitcoin ultimately depends on the performance of Bitcoin. At present, it does not seem to face major direct risks, and its financing is also progressing smoothly. However, the price cycle of Bitcoin has always been consistent with its 4-year halving cycle. Referring to historical rules, 2025 will still be a very exciting year, but there is a high possibility of a bear market afterwards, and the risk level of MSTR will become higher at that time.

Summarize

In the current context of Bitcoin price correction, MicroStrategy's strategy of increasing its holdings has injected confidence into the market, but it has also raised deep doubts about its sustainability. Although MicroStrategy's risks seem to be controllable at present, the future trend of Bitcoin prices will determine whether it will be a Bitcoin guardian or a risk maker. For investors, timely assessment of possible risks, especially when Bitcoin enters an adjustment cycle, and good risk management have become crucial issues.