Author: Zach Pandl, Michael Zhao, Grayscale Rresearch; Translated by: 0xjs@Golden Finance

Key points:

●From a historical perspective, cryptocurrencies have shown a clear four-year cycle, with successive price increases and decreases. Grayscale Research believes that investors can monitor a variety of blockchain-based indicators and other metrics to track crypto cycles and provide a basis for risk management decisions.

●Cryptocurrencies are maturing into a mature asset class: new Bitcoin and Ethereum spot ETPs expand market access, and the incoming U.S. Congress may bring greater regulatory clarity to the industry. Given these factors, cryptocurrencies may finally break out of the four-year cycles that characterized early markets.

● Nevertheless, Grayscale Research determines that the current indicator combination fits the mid-term stage of the cycle. As long as the fundamentals are solid, such as the popularization of applications and the improvement of the macro market environment, the bull market is expected to continue until 2025 and beyond.

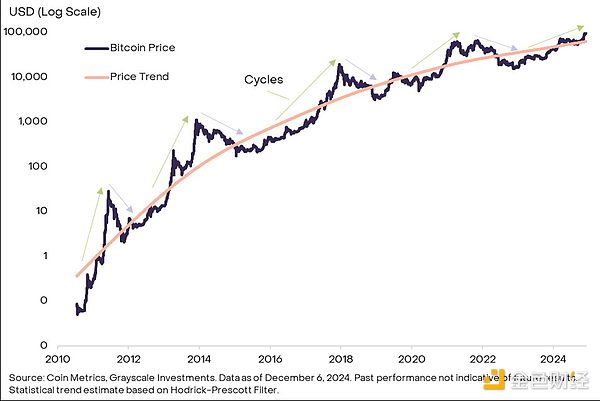

Similar to many physical commodities, the price of Bitcoin does not follow a strict "random walk" pattern. In fact, its price shows signs of statistical momentum: if it rises, it tends to continue to rise, and if it falls, it often falls. From a longer time span, the cycle of Bitcoin's rise and fall fluctuates around the historical upward trend line (Figure 1).

Figure 1: Bitcoin prices fluctuate cyclically around an upward trend

The driving factors of past price cycles vary, and future price returns may not replicate past experience. As Bitcoin matures and is accepted by more traditional investors, and the supply impact of the four-year halving event fades, its price cycle may be reshaped or even disappear. However, studying past cycles can help investors gain insight into Bitcoin's typical statistical characteristics and assist in risk management.

Measuring Momentum

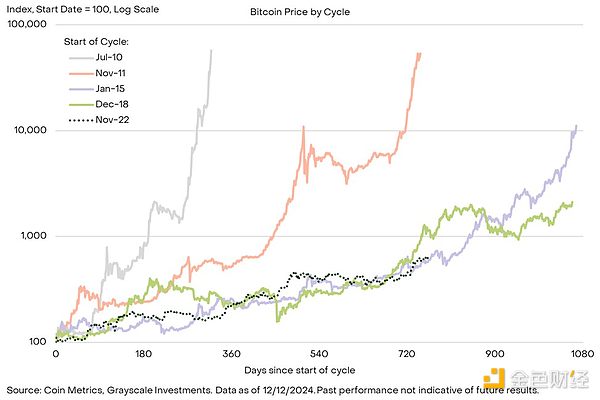

Figure 2 shows the price performance of Bitcoin in the rising phase of the previous cycles. The price is based on the cycle low point set as 100 (marking the beginning of the cycle appreciation phase) and tracked to the peak (marking the end of the appreciation phase). Figure 3 presents the same information in tabular form.

Bitcoin's early cycles were short and the growth was rapid: the first cycle was less than a year, and the second cycle was about two years. Both soared more than 500 times from the low point of the previous cycle. The last two cycles were nearly three years each. From January 2015 to December 2017, Bitcoin appreciated more than 100 times; from December 2018 to November 2021, it increased by about 20 times.

Figure 2: Bitcoin’s trend in this cycle is very similar to the trajectory of the previous two market cycles

After peaking in November 2021, the price of Bitcoin fell to a cycle low of about $16,000 in November 2022, and the current cycle began, which has lasted for more than two years. As shown in Figure 2, this round of price increases is similar to the trajectory of the previous two rounds of Bitcoin cycles, both of which took another year to reach the price peak. In terms of magnitude, this round of cycle has increased by about 6 times, which is also considerable, but far less than the past four rounds. In short, although it is impossible to be sure that future price trends will fit past cycles, history shows that this round of bull market has room for expansion in both duration and magnitude.

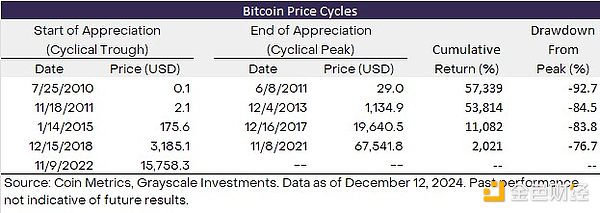

Figure 3: Four unique cycles in Bitcoin price history

Check key indicators

In addition to analyzing the price trends of past cycles, investors can use a variety of blockchain indicators to measure the progress of the Bitcoin bull market. Common indicators include the appreciation of Bitcoin buyers' costs, the scale of new capital inflows, and the relative level of prices and Bitcoin miners' income.

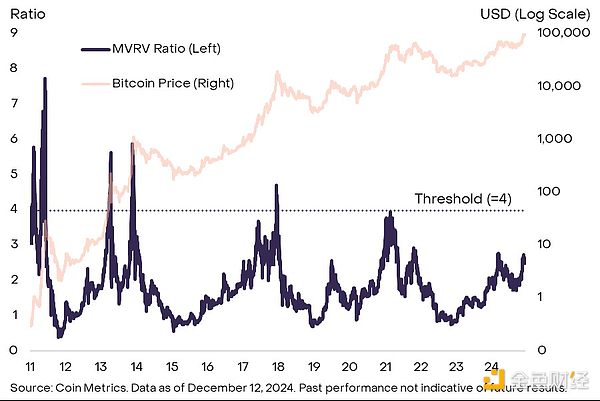

Among them, the most popular indicator is the ratio of Bitcoin market value (MV, calculated per coin at the secondary market price) to realized value (RV, calculated per coin at the most recent transaction price on the chain), that is, the MVRV ratio, which can be regarded as the degree to which Bitcoin market value exceeds the total market cost. In the past four cycles, this ratio has reached at least 4 (Figure 4). The current MVRV ratio is 2.6, indicating that there may be subsequent market trends in this cycle. However, the peak of this ratio has gradually decreased in each cycle, and it may not reach 4 before the price peaks. Figure 4: The MVRV ratio is at an intermediate level

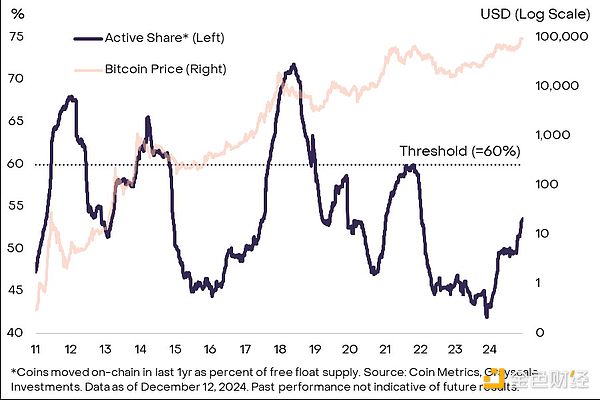

Other on-chain indicators consider the extent to which new funds are injected into the Bitcoin ecosystem, which are often referred to as "HODL Waves" by senior cryptocurrency investors. Price increases may be due to new capital purchasing coins from long-term holders at a higher price. There are many indicators, and Grayscale Research tends to select the ratio of the amount of coins transferred on the chain to the total circulating supply of Bitcoin in the past year (Figure 5). In the past four cycles, this indicator has reached at least 60%, which means that at least 60% of the circulating supply has changed hands in the appreciation phase of one year. The current level is about 54%, suggesting that we may see further increases in the on-chain turnover rate before the price peaks.

Figure 5: The activity of Bitcoin circulation in the past year is less than 60%

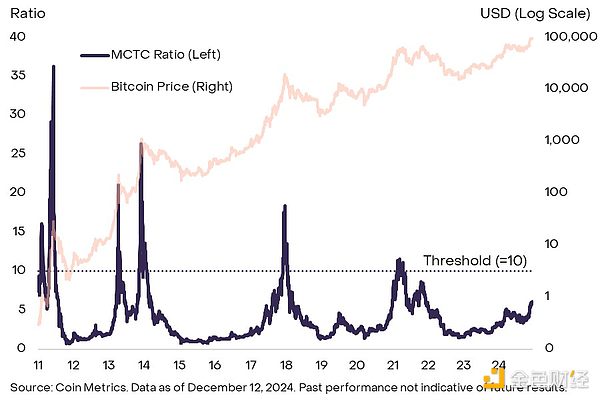

There are also cycle indicators that focus on Bitcoin miners, the professional service providers who maintain the Bitcoin network. For example, the commonly used ratio of miner market value (MC, the dollar value of miners' coins) to the "thermal cap" (TC, the cumulative value of Bitcoin earned by miners through block rewards and transaction fees). The principle is that miners' assets may be profitable when they reach a certain threshold. Historical data shows that after the MCTC ratio exceeds 10, the price in the cycle often peaks (Figure 6). It is currently about 6, indicating that it is in the middle stage of the cycle. However, similar to the MVRV ratio, this indicator has a decline in peak value in each cycle, and the price may peak before it reaches 10.

Figure 6: Bitcoin miner-based indicators are also below historical thresholds

There are many on-chain indicators, and different data sources may have differences. Moreover, these tools only roughly judge the similarities and differences between the current price appreciation stage and the past, and cannot ensure that the relationship between indicators and future price returns is constant. In general, common indicators of the Bitcoin cycle are still lower than the past price peak level. If the fundamental support is solid, the current bull market may continue.

Cryptocurrencies other than Bitcoin

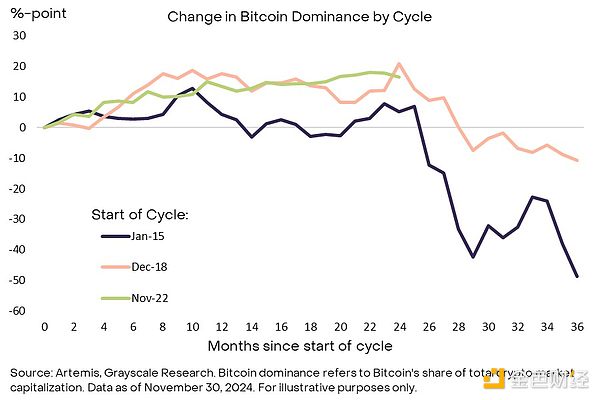

The crypto market is far beyond Bitcoin, and signals from other sectors of the industry can also guide market cycle trends. Given the relative performance of Bitcoin and other crypto assets, such indicators are particularly critical in the coming year. In the past two market cycles, Bitcoin's dominance (share of the total market value of the crypto market) peaked around the second year of the bull market (Figure 7). Its recent decline in dominance coincides with the two-year node of this round of market cycle. If this trend continues, investors should combine more indicators to determine whether crypto valuations are approaching the cycle high.

Figure 7: Bitcoin dominance began to decline in the third year of the first two cycles

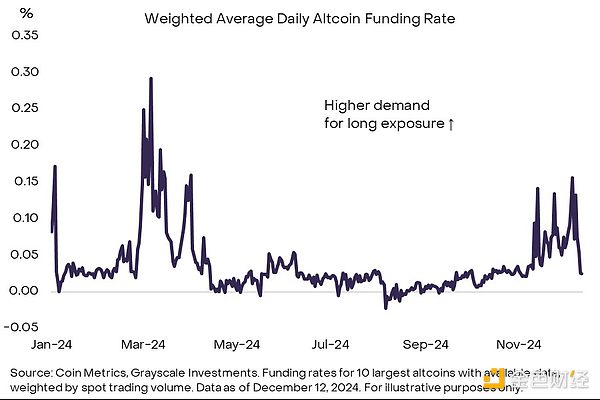

For example, investors can monitor funding rates, which are the cost of holding long positions in perpetual futures contracts. Funding rates rise when speculative traders have high leverage demand. Therefore, the level of market funding rates can measure the overall degree of speculative longs. Figure 8 shows the weighted average funding rate of the top ten crypto assets (the largest "altcoins") other than Bitcoin. The current rate is significantly positive, indicating strong demand for leveraged investors to hold long positions, despite a sharp drop when the market crashed last week. Even the local highs are lower than the peaks at the beginning of this year and the previous round. From this perspective, the current level is consistent with moderate speculative longs in the market, and is still far from the peak of the market cycle.

Figure 8: Altcoin funding rates show moderate speculative longs

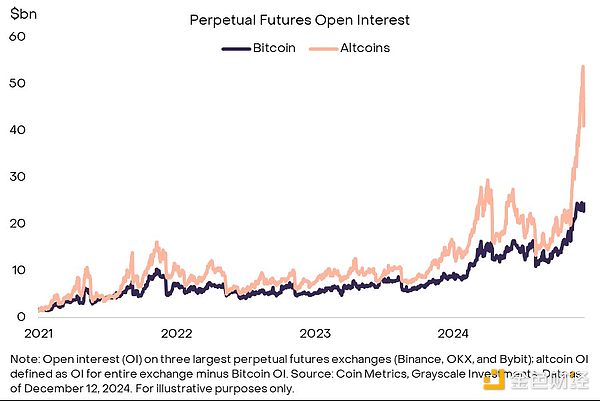

In contrast, the open interest (OI) of altcoin perpetual futures rose to a high level. Before the massive liquidation on Monday, December 9, the altcoin OI of the three major perpetual futures exchanges was nearly $54 billion (Figure 9), highlighting the high speculative long positions in the market. After the massive liquidation at the beginning of this week, OI fell by about $10 billion but remained high. High speculative long positions are consistent with the characteristics of the late market cycle, so they need to be continuously monitored.

Figure 9: Altcoin open interest is high before recent liquidations

Then play the music

Since the birth of Bitcoin in 2009, the digital asset market has made great strides, and this round of crypto bull market is different from the past in many aspects. The key is that the Bitcoin and Ethereum spot ETPs in the US market have been approved to introduce $36.7 billion in net capital inflows, promoting their integration into traditional investment portfolios. In addition, the recent US election is expected to increase the transparency of market supervision and consolidate the position of digital assets in the world's largest economy. This change is of far-reaching significance. The long-term prospects of crypto assets have been repeatedly questioned in the past. Therefore, the valuation of Bitcoin and other crypto assets may not repeat the mistakes of the early four-year cycle.

At the same time, crypto assets such as Bitcoin are similar to digital commodities, and their prices may have momentum characteristics. Therefore, analyzing on-chain indicators and altcoin holdings data can help investors make risk management decisions.

Grayscale Research determined that the current indicator combination fits the mid-term cycle of the crypto market: the MVRV ratio is higher than the cycle low and is still far from the previous market top. As long as the fundamentals are solid, such as the popularization of applications and a positive macro environment, there is no reason why the crypto bull market will not continue until 2025 and beyond.