Author: Jack Inabinet, Bankless; Translated by: Baishui, Golden Finance

Michael Saylor’s MicroStrategy (MSTR) began accumulating BTC in 2020 and has been unstoppable, in the process transforming the software company into the best performing equity investment company of the past two bull market cycles.

Despite massive losses in every quarter of 2024, MSTR has still easily outperformed BTC, with its price parabolicly doubling since September and up another 200% year to date!

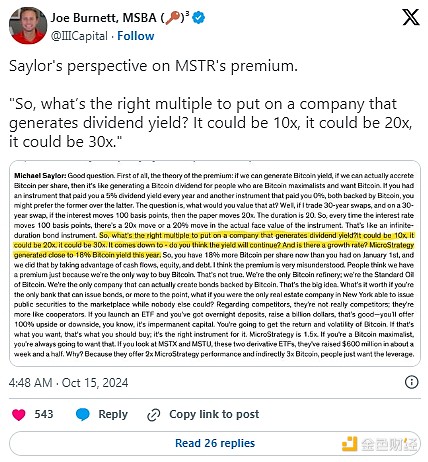

At MicroStrategy’s most recent earnings conference on October 30, company executives unveiled their “21/21 Plan,” a strategic move to raise $42B in capital (equal to 80% of MSTR’s market cap at the time of analysis) in a 50/50 split. The planned combination of stock sales and bond issuances became the largest secondary stock offering in the history of the U.S. stock market.

Today, we’ll decrypt Michael Saylor’s infinite money-making machine and explore how MicroStrategy plans to become a trillion-dollar company.

What is Saylor building?

MicroStrategy announced in August 2020 that it would spend $250 million to purchase 21,454 BTC, becoming the first public company to implement a BTC funding strategy. This initial investment has a return rate of nearly 500% over its 4-year life cycle.

As of September 2024, MicroStrategy holds 252,220 bitcoins.

Although MicroStrategy maintained its position as a BTC giant among direct corporate holders, the launch of the spot BTC ETF in January 2024 reshaped the landscape of the largest holders, with BlackRock replacing MicroStrategy as the fourth largest entity holding BTC, behind Binance, Sabase, and Coinbase.

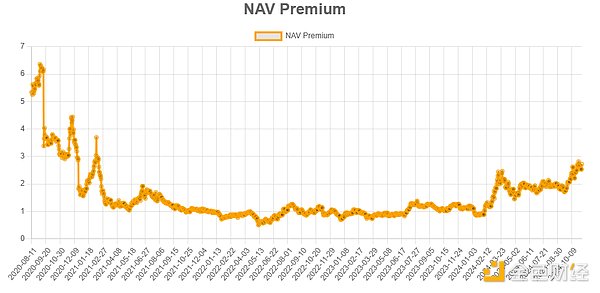

While the market initially valued Microstrategy at five times the value of its BTC assets, this premium began to disappear as holders gradually realized that they would always be diluted to fund additional BTC purchases, and by the end of 2021, as the bear market took hold, MSTR found itself trading below its net asset value (NAV).

Unlike in 2020 when MicroStrategy first began accumulating BTC, investors no longer need to exit traditional markets to gain crypto exposure, but even in the ETF era, MSTR stock has continued to trade at a persistent premium since February 2024.

Compared to spot ETFs that simply track BTC performance (minus management fees), MicroStrategy offers its shareholders the tools of a BTC accumulation strategy that increases the number of tokens per share.

When MSTR stock is trading at a premium to its BTC holdings, MicroStrategy can conveniently raise capital through two avenues: par stock offerings and convertible bond sales. The par stock offering authorization enables MicroStrategy to issue and sell new MSTR shares to the market to raise cash, while convertible bond sales allow MicroStrategy to borrow money on extremely desirable terms in exchange for debt obligations redeemable in cash or a certain number of MSTR shares in the future.

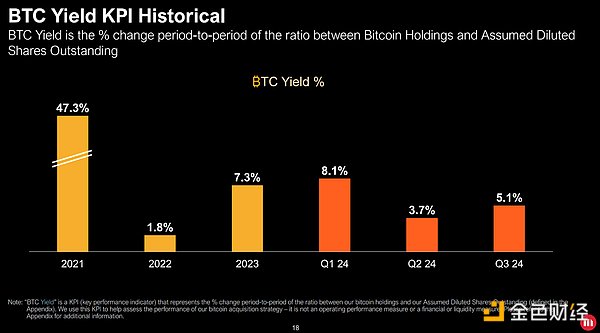

In its second quarter 2024 earnings report, Microstrategy introduced “BTC yield” as a key investor performance metric for the first time to highlight the quarter-over-quarter growth in BTC holdings per share.

Although MicroStrategy unorthodoxly obtained a $205 million BTC-collateralized term loan from Silvergate in March 2022 as the bear market persisted, crypto industry experts often compare the company to a money printing machine as its executives seemingly raise unlimited amounts of cash to purchase BTC through stock dilution during market booms.

In a recent interview with analysts at sell-side research firm Bernstein, Michael Saylor revealed his company’s ultimate goal: to transform into a full-fledged Bitcoin financial services provider.

When shareholders buy MSTR, they are not only buying BTC, they are buying management's ability to effectively use the capital markets and balance sheet to efficiently generate additional returns.

Investment considerations

MSTR will undoubtedly outperform BTC in 2024, but it has also historically exhibited higher volatility, experiencing sharper downside swings alongside large upside rallies. Speculators seeking leveraged BTC exposure would be better off leveraging the underlying asset directly.

While savvy use of public capital markets has enabled MSTR shareholders to accumulate more BTC, Microstrategy's ability to do so depends on investors' continued willingness to purchase its shares at a premium.

As 2022 has shown, MSTR stock could trade at a discount to NAV for extended periods of time. If the convertible bonds mature at a sustained discount to NAV, Microstrategy would be forced to sell an unexpectedly large amount of stock to dilute investors, or sell its BTC holdings to redeem the outstanding bonds.

The upcoming FASB rule changes, which will begin to be implemented this December, will allow digital assets to be reported at their fair market value. Although Microstrategy has reported three consecutive quarters of net losses in 2024, the adoption of these new accounting standards will have a positive impact on the company's financials, making MSTR a potential candidate for inclusion in the S&P 500. Adding it to this index, or an index like the Nasdaq 100, would unlock passive price-indiscriminate flows that can be sold to accumulate more BTC!

Compared to an investment in unproductive spot BTC, Microstrategy stock has the ability to accumulate additional tokens, and unlike companies in the extremely competitive cryptocurrency mining space, Microstrategy has a significant differentiation advantage due to its large BTC moat. As long as the desire to speculate in Bitcoin exists, investors can rest assured knowing that someone may be willing to buy shares at a premium or lend cash on ideal terms.