Figure Markets recently received approval from the U.S. Securities and Exchange Commission (SEC) to launch the first interest-bearing stablecoin YLDS. This move not only marks the U.S. regulator's recognition of crypto financial innovation, but also indicates that stablecoins are evolving from a simple payment tool to a compliant income asset. This may open up greater imagination space for the stablecoin track, making it the next innovative field that can attract large-scale institutional funds after Bitcoin.

Why did the SEC give YLDS the green light?

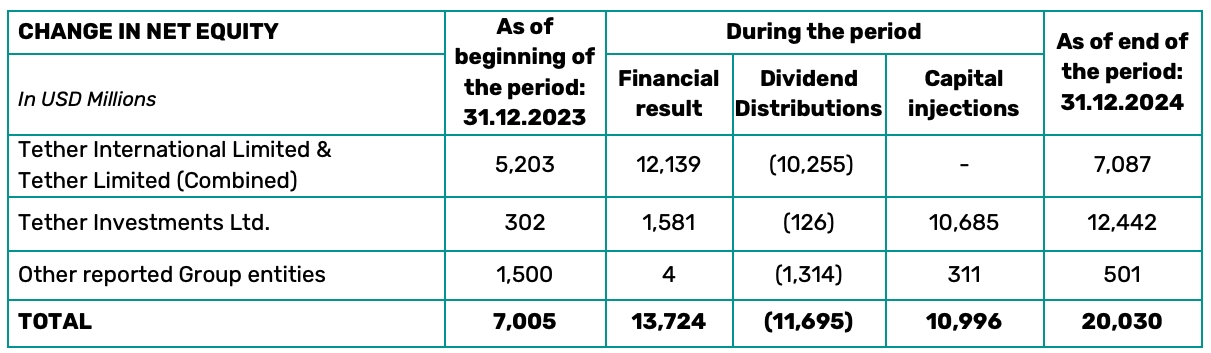

In 2024, Tether, the issuer of the stablecoin USDT, made a profit of $13.7 billion for the whole year, which even exceeded the traditional financial giant Mastercard (about $12.9 billion). Its profits mainly come from investment income generated by reserve assets (mainly US Treasury bonds), but these have nothing to do with the holders, and users cannot use USDT to obtain asset appreciation and investment returns - this is exactly the breakthrough that interest-bearing stablecoins see as enough to subvert the existing situation.

Tether’s Financial Report (2024)

The core of interest-bearing stablecoins lies in the "redistribution of asset income rights": under the traditional stablecoin business model, users sacrifice the time value of funds in exchange for stability, but interest-bearing stablecoins can maintain stability while allowing holders to directly enjoy the income by tokenizing the income rights of the underlying assets. More importantly, interest-bearing stablecoins hit the pain point of the "silent majority": although traditional stablecoins can also obtain income through staking, complex operations and security and compliance risks hinder large-scale user use. However, stablecoins such as YLDS, which "earn interest by holding coins", make capital income threshold-free and truly realize the "democratization of income."

Although the transfer of underlying asset returns will reduce the profit of the issuer, it also greatly increases the attractiveness of interest-bearing stablecoins. Especially at a time when the global economic environment is unstable and inflation levels remain high, both on-chain users and traditional investors have an increasing demand for financial products that can generate stable returns. Products such as YLDS, which are both stable and can provide returns far higher than traditional bank interest rates, will undoubtedly become a "hot commodity" in the eyes of investors.

But these are not the main reasons why the SEC approved YLDS. The key reason why YLDS can get the green light from the SEC is that it circumvents the core controversy of SEC supervision and makes it comply with the current securities laws in the United States . Since a systematic stablecoin regulatory framework has not yet been introduced, the regulation of stablecoins in the United States is currently mainly based on existing laws, but many institutions including the SEC and CFTC have different definitions of stablecoins, trying to gain the dominant position in stablecoin regulation. The struggle between different regulatory agencies and the differences in recognition between regulation and the market have led to a chaotic situation in the regulation of stablecoins in the United States, making it difficult to form a basic consensus. However, interest-bearing stablecoins such as YLDS that can generate income have a structure similar to traditional fixed-income products. Even under the current legal framework, they clearly belong to the category of "securities" and there is no controversy. This is a prerequisite for interest-bearing stablecoins such as YLDS to be regulated by the SEC.

But this also means that although the approval of YLDS shows that the US crypto regulatory attitude continues to improve, regulatory agencies including the SEC are actively adapting to the rapidly developing stablecoin and crypto financial markets, and the regulation of stablecoins has also shifted from "passive defense" to "active guidance", but this cannot change the regulatory dilemma faced by traditional stablecoins such as USDT/USDT in the short term. More changes still need to wait until the US Congress formally passes the stablecoin regulatory bill . The industry generally expects that the US stablecoin regulatory bill may be gradually implemented in the next 1 to 1.5 years.

However, YLDS distributes the interest income of the underlying assets (mainly U.S. Treasury bonds, commercial paper, etc.) to the holders through smart contracts, and uses a strict KYC verification mechanism to bind the income distribution to the compliance identity, reducing regulatory concerns about anonymity. These compliance designs provide a reference for other similar projects to seek regulatory approval. In the next 1-2 years, we may see more compliant interest-bearing stablecoin products, and force more countries and regions to consider the necessity of developing and regulating interest-bearing stablecoins. For regions such as Hong Kong and Singapore that have already introduced stablecoin regulations and mostly regard stablecoins as payment tools, when faced with interest-bearing stablecoins that clearly have securities attributes, in addition to adjusting the existing regulatory system, it may also be considered to limit the types of underlying assets of interest-bearing stablecoins, thereby bringing them into the regulatory scope of tokenized securities.

The rise of interest-bearing stablecoins will accelerate the institutionalization of the crypto market

The SEC's approval of YLDS not only demonstrates the openness and friendliness of U.S. regulation at this stage, but also indicates that in the mainstream financial context, stablecoins may evolve from "cash substitutes" to new assets with the dual attributes of "payment tools" and "income tools", and will accelerate the institutionalization and dollarization of the crypto market.

Although traditional stablecoins meet the needs of crypto payments, most institutions only use them as short-term liquidity tools due to the lack of interest income; interest-bearing stablecoins can not only generate stable income, but also improve capital turnover through intermediary-free and all-weather on-chain transactions, and have significant advantages in capital efficiency and instant settlement capabilities. Ark Invest pointed out in its latest annual report that hedge funds and asset management institutions have begun to incorporate stablecoins into their cash management strategies, and the approval of YLDS by the SEC will further dispel the compliance concerns of institutions and raise the acceptance and participation of institutional investors in such stablecoins to a new level.

The massive influx of institutional funds will further promote the rapid growth of the interest-bearing stablecoin market, making it an even more indispensable part of the crypto ecosystem. In order to cope with competition and meet market demand, OKG Research optimistically predicts that interest-bearing stablecoins will usher in explosive growth in the next 3-5 years and occupy about 10-15% of the stablecoin market, becoming another crypto asset class that can attract large-scale institutional attention and capital investment after BTC .

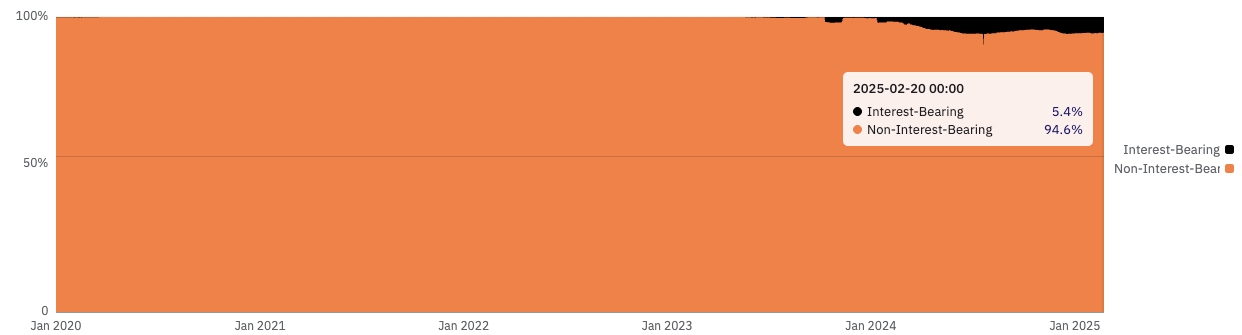

Percentage of interest-bearing stablecoins in the Ethereum ecosystem (@21co, as of 2025/2/20)

The rise of interest-bearing stablecoins will further consolidate the dollar's dominance in the crypto world. There are three main sources of income for interest-bearing stablecoins on the market, namely, through investment in U.S. Treasuries, blockchain staking rewards, or structured strategy income. Although the synthetic U.S. dollar stablecoin USDe launched by Ethena Labs was a great success in 2024 and became a major player in the interest-bearing stablecoin market, it does not mean that staking and structured strategies as a source of income will become mainstream. On the contrary, we believe that interest-bearing stablecoins backed by U.S. Treasuries will still be the first choice for institutional investors in the future.

Although the physical world is accelerating the de-dollarization: China and Japan have sold a large number of U.S. debts in the past few years, and Saudi Arabia announced in June 2024 that it would not renew the "Petrodollar Agreement" that has been maintained for half a century, making the dollar decoupled from oil after decoupling from gold, and the BRICS countries are constantly trying to bypass the SWIFT network to reduce their dependence on dollar payments, the digital on-chain world continues to move closer to the dollar. Whether it is the large-scale application of the U.S. dollar stablecoin or the tokenization wave set off by Wall Street institutions, the United States continues to strengthen the influence of U.S. dollar assets in the crypto market, and this trend of dollarization is being strengthened.

This trend is unlikely to be reversed in the short term, because in terms of liquidity, stability and market acceptance, there are no more alternatives to tokenized innovation and crypto-financial markets except for US dollar assets represented by US Treasuries. The SEC's approval of YLDS also shows that US regulators have given the green light to US Treasury-based interest-bearing stablecoins at this stage, which will undoubtedly attract more projects to launch similar products in the future. This is also an important reason why we still believe that US Treasuries, as risk-free assets, will still dominate the underlying asset pool of interest-bearing stablecoins, even though we know that the income model of interest-bearing stablecoins will definitely be more diversified in the future, and reserve assets may also expand to more types of RWAs such as real estate, gold, and corporate bonds.

Conclusion

The approval of YLDS is not only a compliance breakthrough for crypto innovation, but also a milestone in financial democratization. It reveals a simple truth: under the premise of controllable risks, the market demand for "money making money" will always exist. With the improvement of the regulatory framework and the influx of institutional funds, interest-bearing stablecoins may reshape the stablecoin market and enhance the dollarization trend of crypto financial innovation. However, this process also needs to balance innovation and risk to avoid repeating past mistakes. Only in this way can interest-bearing stablecoins truly realize "letting everyone make money while lying down."