Source: CryptoVizArt, UkuriaOC, Glassnode

Compiled by: Baishui, Golden Finance

summary

- Strong capital inflows from ETFs and spot markets have driven Bitcoin to $93,000. More than $62.9 billion has entered the market in the past 30 days, with BTC dominating the demand inflow.

- The increase in unrealized profits among long-term holders triggered a massive spending campaign, with 128,000 Bitcoins sold between October 8 and November 13.

- US cash ETFs played a key role, absorbing approximately 90% of the selling pressure from long-term holders during the analysis period. This highlights the growing importance of ETFs in maintaining liquidity and stabilizing markets.

Capital inflows surge

Bitcoin’s price performance has been phenomenal since the beginning of November, with new ATHs being formed throughout the month. When comparing the current cycle’s price performance to the 2015-2018 (blue) and 2018-2022 (green) cycles, striking consistent similarities can be seen. Despite widely varying market conditions, both the magnitude and duration of the rallies have been surprisingly consistent.

This long-term consistency across cycles remains interesting, providing insights into Bitcoin’s macro price behavior and cyclical market structure.

Historically, past bull markets have lasted between 4 and 11 months from the current point, providing a historical framework for assessing cycle duration and momentum.

A new ATH was set this week at $93,200, which brings Bitcoin’s quarterly performance to an impressive +61.3%. This is an order of magnitude higher than the relative performance of gold and silver, which posted quarterly gains of +5.3% and +8.0%, respectively.

This stark contrast suggests that capital may be shifting from traditional commodity store of value assets to younger, emerging, and digital assets such as Bitcoin.

Bitcoin’s market capitalization also expanded to a staggering $1.796 trillion, making it the world’s seventh-largest asset. This move puts Bitcoin above two symbolically important global assets: silver, valued at $1.763 trillion, and Saudi Aramco, valued at $1.791 trillion.

As of now, Bitcoin is only 20% behind Amazon, making it the next major milestone on its way to becoming the world’s most valuable asset.

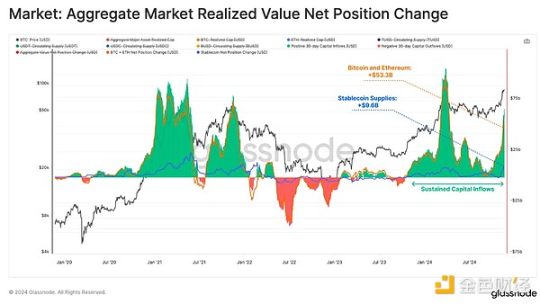

Following Bitcoin’s 90-day outperformance, the broader digital asset market is beginning to experience a massive influx of capital. Over the past 30 days, total inflows reached $62.9 billion, with the Bitcoin and Ethereum networks absorbing $53.3 billion, while the supply of stablecoins increased by $9.6 billion.

This is the highest level since the peak in March 2024, reflecting restored confidence and new demand after the U.S. presidential election.

Expanding on the observed capital inflows, the vast majority of the $9.7 billion in stablecoins minted in the past 30 days were deployed directly to centralized exchanges. This inflow is closely correlated with total capital flows of stablecoin assets over the same period, highlighting their key role in stimulating market activity.

The surge in stablecoin balances on exchanges reflects strong speculative demand from investors to capitalize on the trend, further reinforcing the bullish narrative and post-election momentum.

Investigate investor profitability

So far, we have explored the trend of rising market liquidity, which supports Bitcoin's outperformance. In the next section, we will use the MVRV ratio to evaluate how this price behavior affects the unrealized profitability (paper gains) of market investors.

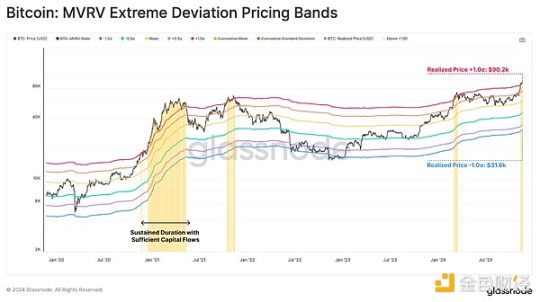

When comparing the current value of the MVRV ratio (orange) to its annual moving average (blue), we can see an acceleration in investor profitability. This phenomenon is often a supportive environment for continued market momentum, but it also creates conditions where investors are more likely to start taking profits to realize paper gains.

As investor profitability in the market increases, the potential for new sell-side pressure grows. By overlaying the MVRV ratio with a ±1 standard deviation band, we can construct a framework to assess overheated and underheated market conditions.

- Overheat (Warm): MVRV trading above +1SD

- Underheating (cold colors): MVRV trading below -1SD

The price of Bitcoin recently broke above the +1σ range at $89,500. This indicates that investors are currently holding statistically significant unrealized profits and suggests an increased likelihood of profit-taking activity.

However, historically markets have remained in this overheated state for long periods of time, especially when supported by sufficiently large capital inflows to absorb the selling pressure.

Extreme spending by long-term holders

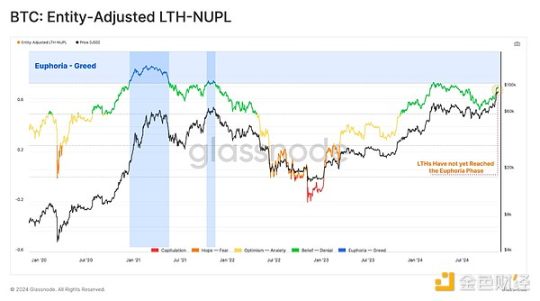

During the euphoric phase of a market cycle, the behavior of long-term investors becomes critical. LTH controls a large portion of the supply, and its spending dynamics can greatly influence market stability, ultimately forming local and global tops.

We can assess the book gains held by LTH using the NUPL indicator, which is currently at 0.72, just below the threshold of 0.75 for conviction (green) to excitement (blue). Despite the sharp price increase, sentiment among these investors remains low compared to previous cycle tops, suggesting there may be further room for growth.

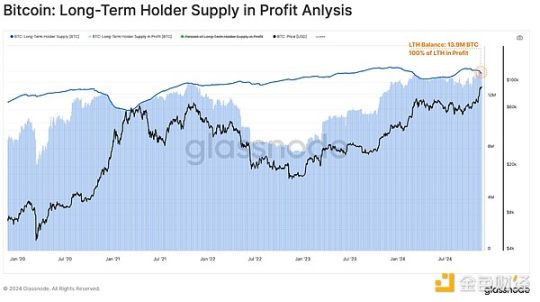

As Bitcoin surpassed $75,600, 100% of the 14m Bitcoin held by long-term holders turned into profits, spurring an acceleration in spending. This has resulted in a balance drop of +200k BTC since the ATH break.

This is a classic and repeating pattern where long-term holders start to take profits whenever price action is strong and demand is high enough to absorb profits. Since LTH still holds a large amount of Bitcoin, it is likely that many LTH are waiting for higher prices before releasing more Bitcoin back into liquid circulation.

We can assess the intensity of LTH seller pressure using the Long Term Holder Spending binary indicator. This tool assesses the percentage of days in the past two weeks that the herd spent more than it accumulated, resulting in a net decline in its holdings.

Since the beginning of September, long-term holder spending has steadily increased as the price of Bitcoin has risen. With the recent surge to $93,000, the metric reached a value that showed LTH balances falling in 11 of the past 15 days.

This highlights increasing pressure on long-term holders to distribute, although not yet to the extent observed around the March 2021 and March 2024 peaks.

Having identified the increased spending behavior of long-term holders, we can look to the next tool to gain more insight into their activity around key market points. The interplay of profit taking and unrealized profits helps highlight their role in shaping cycle shifts.

This chart visually shows:

- LTH Realized Price (blue): Average acquisition price by long-term holders.

- Profit/Loss Pricing Range (blue): Range representing extreme profit (+150%, +350%) and loss (-25%) levels that typically trigger significant spending activity.

- Profit Taking (Green): The stage where long term holders hold profits of more than 350% and increase their spending.

- Sell-offs (red): Periods of high spending where long term holders are at a -25%+ loss.

The price of Bitcoin has surged to over 350% profit territory at $87,000, prompting significant profit-taking behavior from this group. As the market rises, distribution pressures are likely to increase, and these unrealized gains will expand accordingly. That said, this has historically marked the beginning of the most extreme phase of previous bull markets, with unrealized profits growing to over 800% in the 2021 cycle.

Institutional Buyers

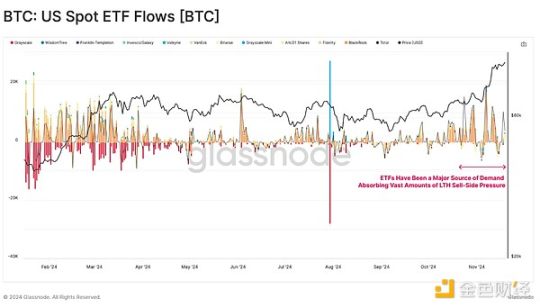

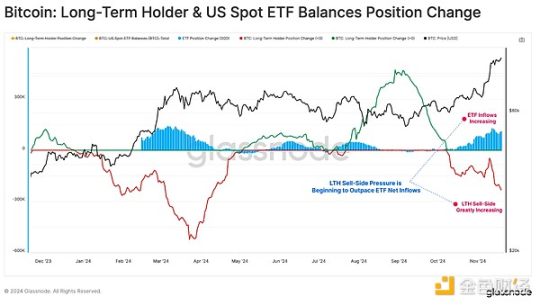

We will now turn our attention to the role of institutional buyers in the market, particularly through US spot ETFs. ETFs have been the primary source of demand in recent weeks, absorbing the majority of LTH sellers. This dynamic also highlights the growing influence of institutional demand in shaping the structure of the modern Bitcoin market.

Since mid-October, weekly ETF inflows have surged to between $1 billion and $2 billion per week. This represents a significant uptick in institutional demand and one of the most significant periods of inflows to date.

To visualize the balancing force of LTH selling pressure and ETF demand, we can analyze the 30-day change in Bitcoin balance for each cohort.

The chart below shows that the ETF absorbed approximately 128,000 BTC, or about 93% of the 137,000 BTC net selling pressure exerted by LTH, between October 8 and November 13. This highlights the key role of the ETF in stabilizing the market during periods of increased selling activity.

However, since November 13, LTH sell-side pressure has begun to outpace ETF net inflows, echoing a pattern observed in late February 2024, when supply-demand imbalances led to increased market volatility and consolidation.

Summarize

Bitcoin’s rally to $93,000 was supported by strong capital inflows, with about $62.9 billion worth of capital flowing into the digital asset space over the past 30 days. This demand was led by institutional investors through U.S. spot ETFs, even as capital flowed out of gold and silver.

ETFs have played a key role, absorbing more than 90% of the sell-side pressure from long-term holders. However, as unrealized profits reach more extreme levels, we can expect LTH payouts to increase and its inflows to exceed ETF inflows in the short term.