Written by: 0xWeilan

The information, opinions and judgments on markets, projects, currencies, etc. mentioned in this report are for reference only and do not constitute any investment advice.

In 2024, global macro-finance will reach a turning point amid turmoil.

With the 50 basis point drop in September, the US dollar entered a cycle of interest rate cuts. However, with the US presidential election and global geopolitical conflicts, US economic employment data began to be "distorted", which increased the differences among traders on the future market. The US dollar, US stocks, and US bonds all experienced sharp fluctuations, making short-term trading more difficult.

The differences and concerns were reflected in the U.S. stock market as the three major indexes all fluctuated violently without direction. On the contrary, BTC, which lagged behind in the rise, caught up in October, soaring 10.89%, and made a major breakthrough in technology, taking down multiple important technical indicators in one fell swoop and approaching the upper edge of the "new high consolidation zone" again, once reaching $73,000.

BTC's internal structure remains perfect and is ready for a complete breakthrough, but it is still "suppressed" by the U.S. stock market, which is trapped by the uncertain prospects of the election. But the election is just an episode and will not change the cycle. We believe that after the November election, after necessary conflicts and choices, the U.S. stock market will resume its rise. If so, BTC will break through the historical high and start the second half of the crypto asset bull market.

Macro Finance: US Dollar, US Stocks, US Bonds and Gold

In October, after falling for three consecutive months, the US dollar index "unexpectedly" rebounded sharply by 3.12%, from 100.7497 to 103.8990, returning to the level of January last year. This rebound was triggered by "Trump's victory". Traders believe that Trump's election will intensify the decoupling between China and the United States, push up inflation, and make it difficult to smoothly implement interest rate cuts. We believe that this rebound has exceeded expectations and priced in the expectation of "slowing interest rate cuts", so the rebound of the US dollar index is unsustainable.

Monthly trend of US dollar index

The expectation of "tax cuts" and "decoupling between China and the United States" in Trump's economic policies will inevitably lead to a further increase in the size of US debt. As the probability of Trump's victory increases, the yield on 2-year US Treasury bonds has risen by 14.48% after falling for five consecutive months, and the yield on 10-year bonds has risen by 13.36%. The sell-off of US Treasury bonds is very serious.

At present, U.S. stocks are traded around two main lines: whether Trump or Harris will be elected, the divergence in asset trends that may be caused by their economic policies, and whether the U.S. economy will have a soft landing, a hard landing, or no landing.

The low CPI and unemployment rates in October have made people more and more confident that the economy is heading for a soft landing, which has kept the US stock market near its historical highs. However, the ultra-low non-farm payrolls data and the fact that pricing was completed in advance and the election was undecided have caused traders to lose their trading direction. The Q3 financial reports of the "Big 7" have been released one after another, with mixed results. Against this backdrop, the Nasdaq fell after hitting a new high in the middle of the month, down 0.52% on the month, and the Dow Jones fell 1.34% on the month. Considering the sharp rebound in the US dollar index, this is already a good result.

Only gold has received support from safe-haven funds, with London gold rising 4.15% on a monthly basis to $2,789.95 per ounce. The current strength of gold comes not only from safe-haven funds, but also from the continued increase in holdings by central banks of many countries (replacing part of the US dollar as a value reserve for their own currencies).

Crypto assets: Effective breakthrough of two major technical indicators

In October, BTC opened at $63,305.52 and closed at $70,191.83, a monthly increase of 10.89% and an amplitude of 23.32%, with a moderate increase in volume. This is the first time that the price has risen for two consecutive months since the adjustment in March.

BTC daily trend

In terms of technical indicators, BTC has achieved several major breakthroughs this month; it has effectively broken through the 200-day moving average and the downward trend line since March (white line in the above figure). The breakthrough of these two major technical indicators means an improvement in the long-term trend, which can temporarily eliminate the doubts about the crypto market turning bearish.

Currently, the market is in the stage of retreating after testing the upper edge of the "new high consolidation zone". Next, we focus on two technical indicators, one is the upper edge of the "new high consolidation zone" (US$73,000) and the rising trend line (currently around US$75,000). In previous reports, we emphasized that an effective breakthrough of the "new high consolidation zone" means the end of the long consolidation of 8 months, and re-entering the rising trend line means the arrival of a new market (the second wave of the bull market, i.e. the main rising wave).

BTC monthly trend

On the monthly chart, we can see that the low price of BTC has continued to rise since August. This turning point is based on two points: the continuous improvement of global liquidity since the interest rate cuts by the Federal Reserve, the European Union and China, and the internal adjustment of crypto assets, that is, the completion of the "short to long" coin holding structure.

Long-short game: Increased liquidity may trigger the start of a second wave of selling

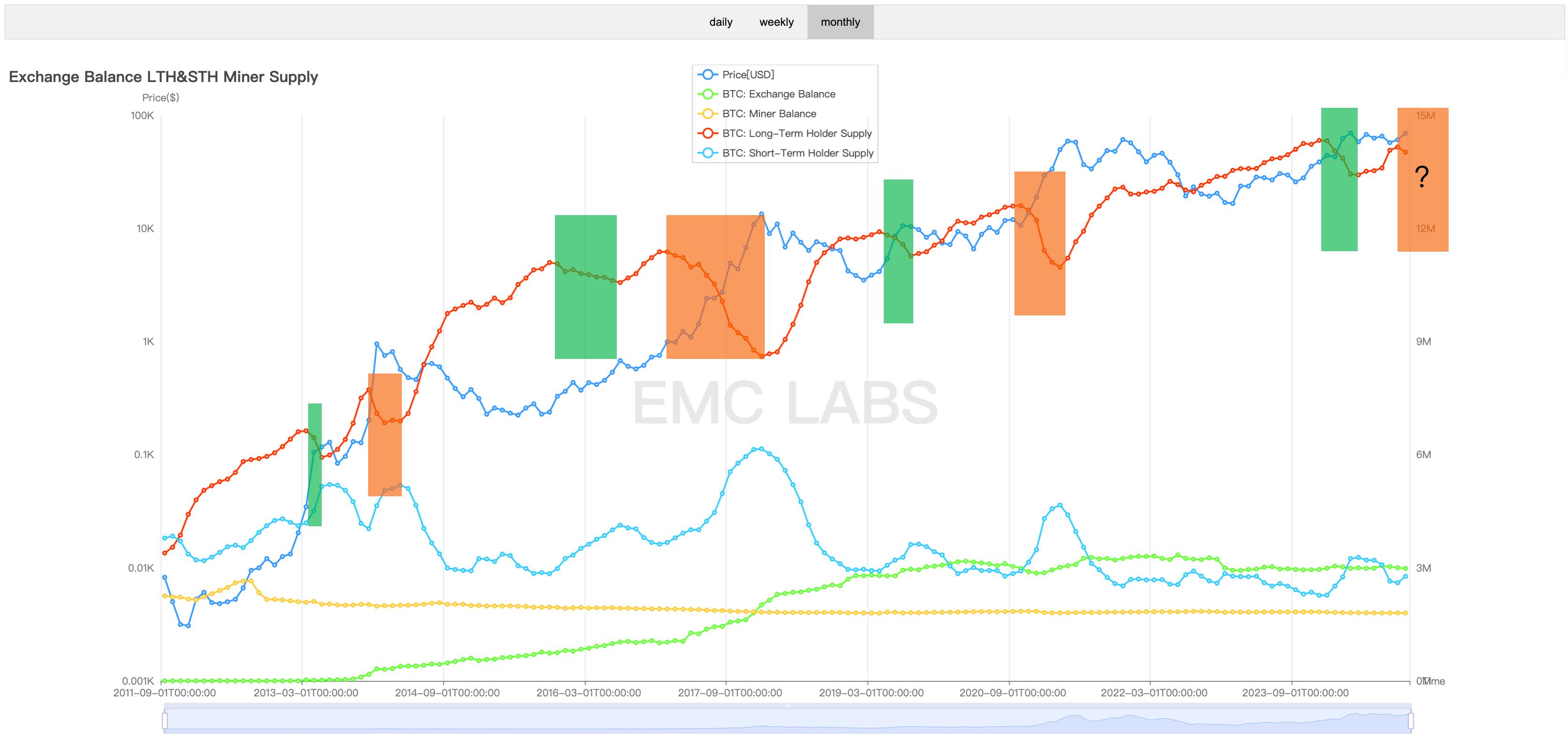

Long, short, CEX and Miner BTC holdings distribution (monthly)

In a previous report, EMC Labs pointed out that as the bull market in crypto assets unfolds and adjusts, long holders will experience two rounds of selling, thereby throwing the chips accumulated during the market downturn back into the market.

In this cycle, the first wave of long-term selling started in January and ended in May, and then turned to re-accumulation until October. The Federal Reserve cut interest rates for the first time in September, and the liquidity of the crypto market improved. Long-term holders began to sell again, pushing the holding structure from long to short. The scale of selling this month is close to 140,000 coins.

This is the result of the Fed's interest rate cuts to improve liquidity, and it is also a necessary stage in the cycle. Of course, we need more time to confirm the sustainability of this sell-off. Overall, we tend to think that the second wave of sell-offs has begun. Unless the Fed's interest rate cuts change direction, this process will continue in the medium and long term.

This is accompanied by the continued strengthening of market liquidity.

Liquidity Enhancement: Buying Power Comes from BTC ETF Channel

For the crypto market, the start of the interest rate cut cycle is of great significance. To some extent, the upward momentum of BTC last year came from the expectation of interest rate cuts and the early pricing of the opening of the BTC ETF channel. The adjustment since March can also be understood as a market correction before the start of the interest rate cut.

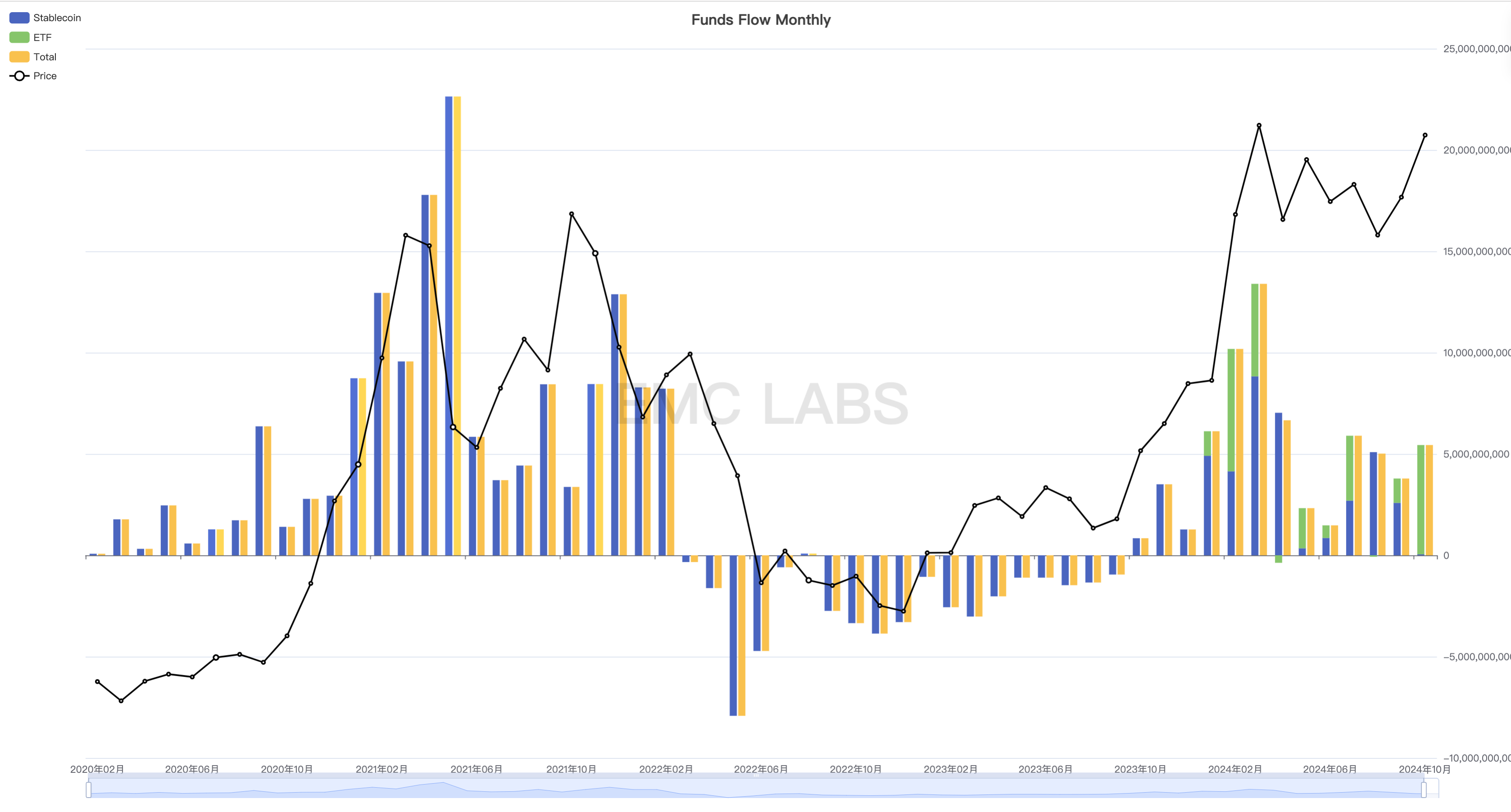

Monthly statistics of capital inflow and outflow in the crypto asset market (Stablecoins + BTC ETF)

This judgment is based on our statistics on the inflow and outflow of funds in the BTC ETF channel. From the above chart, we can see that after March, the funds in this channel showed signs of slowing down inflow or even outflow. This downward trend improved in October.

EMC Labs monitors that in October, 11 BTC ETFs in the United States recorded a total inflow of $5.394 billion, the second largest inflow month on record, second only to $6.039 billion in February this year. This large inflow provides fundamental impetus for BTC prices to challenge previous highs.

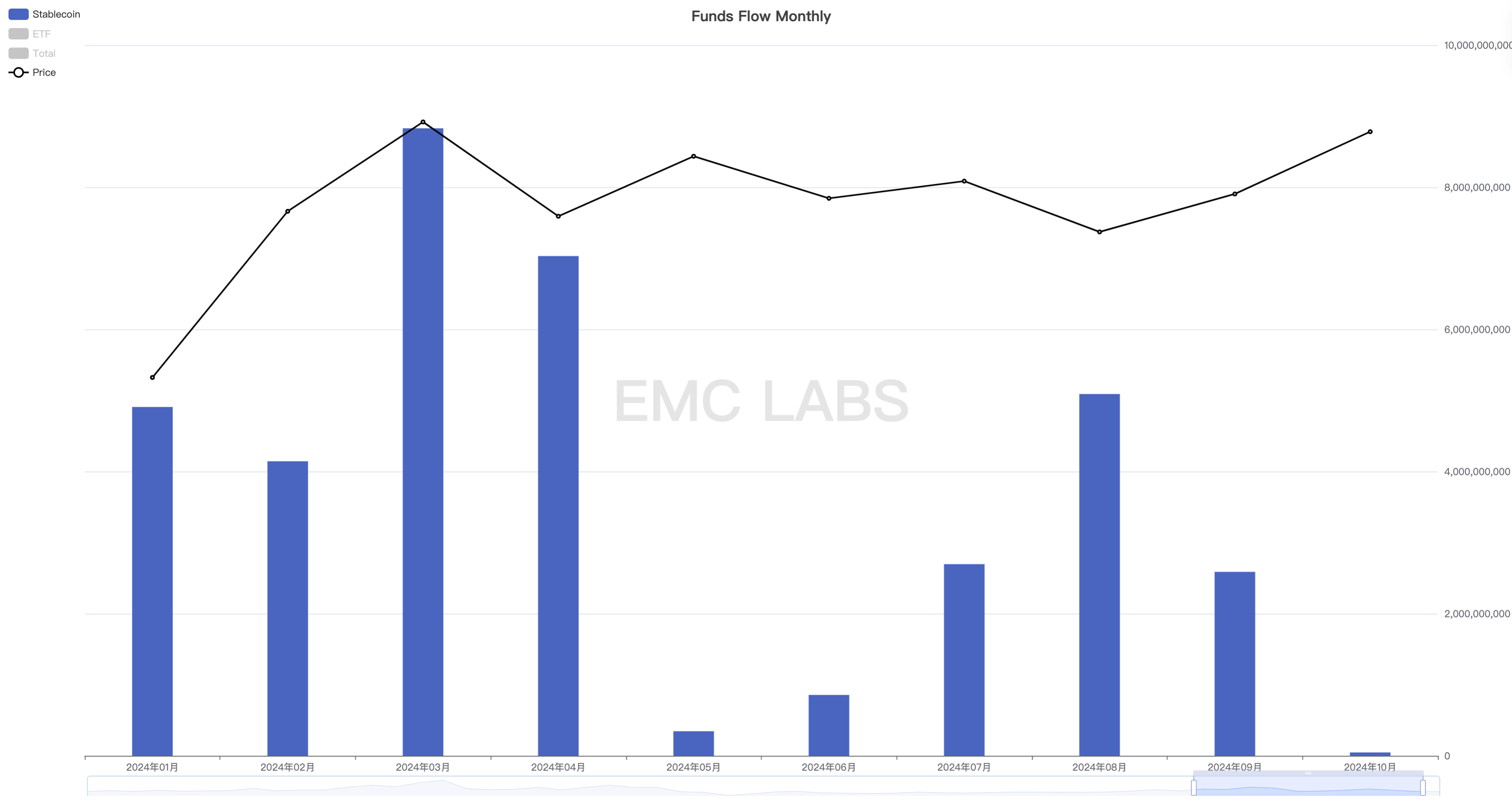

Stablecoin channel funds performed very weakly in October, with only US$47 million inflows for the entire month, recording the worst monthly performance so far this year.

Stablecoins monthly inflow and outflow statistics

The weak stablecoin channel funds can be used to explain why Altcoins performed very poorly despite BTC challenging its previous high. The funds from the BTC ETF channel cannot benefit Altcoins, which is one of the huge changes in the structure of the crypto asset market and deserves close attention.

Among them, the sharp increase in funds in the BTC ETF channel includes the "Trump transaction" component. Because of Trump's pursuit of Crypto, people speculate and buy in the hope of short-term profit. This is worth paying attention to. With the US presidential election on November 4, the US time, the market may fluctuate violently in the short term.

Conclusion

According to the 13F report submitted by US institutional investors, there were 1,015 institutions holding BTC ETFs in Q1 2024, with a holding scale of US$11.72 billion; in Q2, there were more than 1,900 institutions holding BTC ETFs, with a holding scale of US$13.3 billion, and 44% of institutions chose to increase their holdings. Currently, the scale of BTC managed by BTC ETFs has exceeded 5% of the total supply, which is a noteworthy breakthrough.

The BTC ETF channel has already taken control of the medium- and long-term pricing power of BTC. In the long run, funds are expected to continue to flow into the BTC ETF channel during the interest rate cut cycle, providing material support for the long-term trend of BTC prices. However, there are still many uncertainties in the medium and short term.

Taking into account the structure of the market and macro-financial trends, EMC Labs maintains its previous judgment that BTC is likely to break through the previous high in Q4 and start the second half of the bull market. In the Crypto market, the start of the second half of the Altcoin bull market is based on the recovery of stablecoin channel capital inflows.

The biggest risk comes from the results of the US election, whether the interest rate cut can be carried out smoothly in line with the expectations of all market parties, and the stability of the US financial system.