Author: 0xTodd

First, let’s get excited about our beloved Bitcoin hitting $98,000!

There is no doubt that the contributor to the 40K-70K is the Bitcoin ETF, and the contributor to the 70K-100K is MicroStrategy.

Many people now compare MicroStrategy to the BTC version of Luna, which makes me a little embarrassed because Bitcoin is my favorite cryptocurrency, and Luna happens to be the cryptocurrency I hate the most.

I hope this post will help you better understand the relationship between WeStrategy and Bitcoin.

First, a few conclusions are put at the beginning:

- WeCare is not Luna, and its safety cushion is much thicker.

- MicroStrategy increased its Bitcoin holdings by purchasing bonds and selling stocks.

- WeStrategy’s nearest debt repayment date is 2027, which is more than two years away.

- The only soft threat to WeStrategy is Bitcoin whales.

WeCare is not Luna, but it has a much thicker safety cushion than Luna

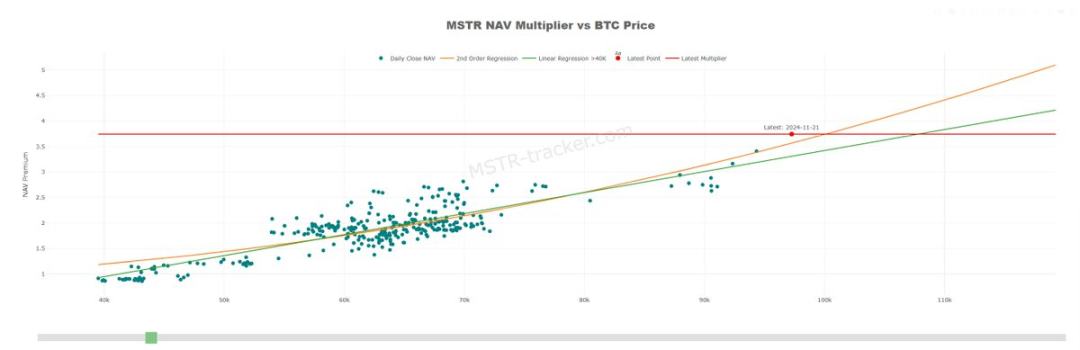

MSTR Net Worth vs Bitcoin Price

WeCare was originally a software company with a lot of unrealized profits in its accounts and no longer wanted to invest in production, so it began to move away from the real economy and started buying Bitcoin out of its own pocket in 2020.

Later, WeStrategy used up all the money in its account and started to leverage. It leveraged in an off-market way and was determined to borrow money to buy Bitcoin by issuing corporate bonds.

The essential difference between it and Luna is that Luna and UST print each other, and UST is essentially meaningless unanchored money printing, which is barely maintained by the fake interest rate of 20%.

But WeStrategy is equivalent to bottom-up fixed investment + leverage, which is the standard of borrowing money to go long, and it bets on the right direction.

The popularity of Bitcoin far exceeds that of UST, and the impact of MicroStrategy on Bitcoin is significantly lower than that of Luna on UST. It is a simple truth. As the saying goes, 2% daily profit is a Ponzi scheme, and 2% annual profit is a bank. Quantitative change leads to qualitative change. MicroStrategy is not the only factor that determines Bitcoin, so MicroStrategy is definitely not Luna.

MicroStrategy increases Bitcoin holdings by selling bonds and stocks

In order to raise funds quickly, MicroStrategy has issued multiple bonds totaling US$5.7 billion (for your intuitive understanding, this is equivalent to 1/15 of Microsoft's debt).

And almost all of this money is used to continuously increase Bitcoin holdings.

Everyone has used on-exchange leverage, where you have to use Bitcoin as a deposit before the exchange (and other users in the exchange) will lend you money. But off-exchange leverage is different.

All creditors in the world are only worried about one thing, that is, debtors will not repay their debts. Without collateral, why would people be willing to lend money to WeCe in the off-market?

MicroStrategy’s bond issuance is very interesting. In recent years, it has issued a convertible debt.

This convertible bond is very interesting. Let's take an example:

Bondholders have the right to convert their bonds into MSTR shares in two phases:

1. Initial stage:

- If the trading price of the bond falls by >2%, the creditor can exercise the option to convert the bond into MSTR shares and sell it back for the principal;

- If the bond's trading price is normal or even increases, the creditor can resell the bond in the secondary market at any time to recoup the investment.

2. Later stage: When the bonds are about to mature, the 2% rule no longer applies, and the bondholders can get their cash back or convert the bonds directly into MSTR shares.

Let's analyze it again. This is generally a business that is sure to make money for creditors.

- If Bitcoin falls and MSTR has money, creditors can get their cash back

- If Bitcoin falls and MSTR has no money, creditors can still have a final guarantee, that is, convert it into stocks and cash it out;

- If Bitcoin goes up, MSTR will go up, and creditors can give up cash and get more stock returns.

In a nutshell, this is a deal with a high lower limit and a very high upper limit, so naturally WeCe raised the money smoothly.

Fortunately, no, it should be said that WeStrategy chose Bitcoin.

Bitcoin has lived up to it.

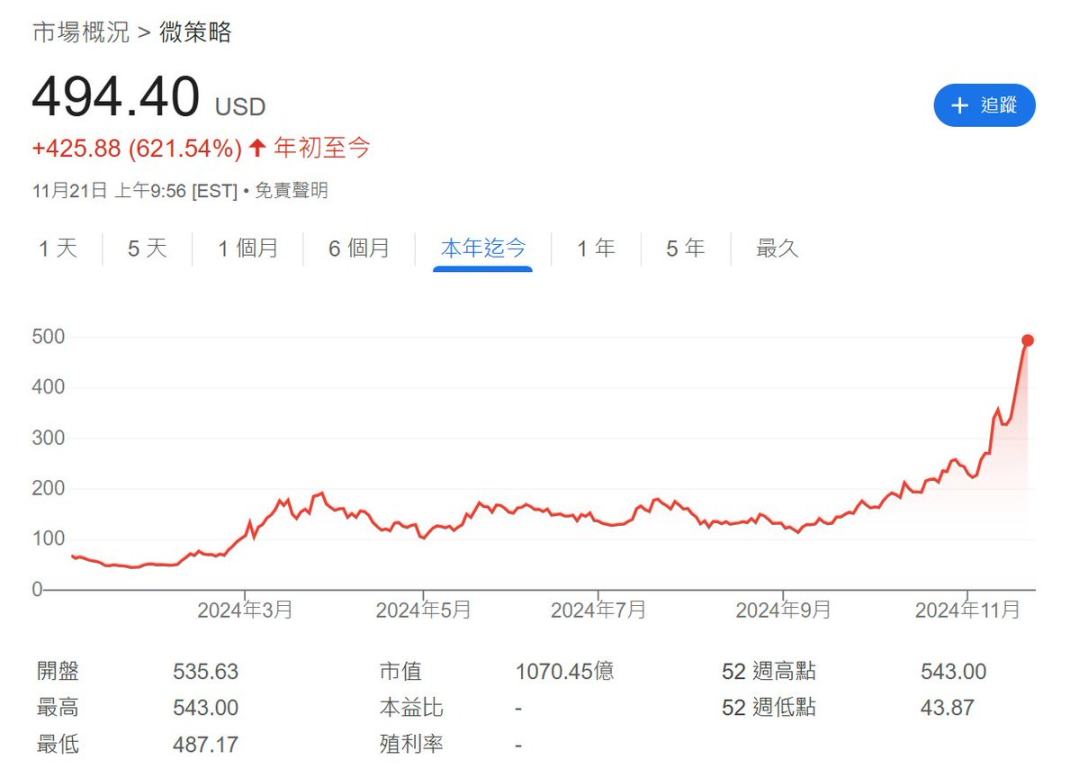

2024 MicroStrategy Stock Price Trend

As Bitcoin continues to grow, the Bitcoin accumulated by MicroStrategy in the early days has also risen in value. According to the simple and classic stock principle, the more assets a company has, the higher its market value should be.

Therefore, WeCare’s stock price also soared to the sky.

The daily trading volume of MicroStrategy has exceeded that of Nvidia, the absolute blue chip of this year. Therefore, MicroStrategy now has more choices.

Now MicroStrategy not only relies on issuing bonds, but can also directly issue additional stocks and sell them to make money.

Unlike many meme coins or Bitcoin developers who do not have the authority to mint coins, traditional companies can issue additional shares after complying with relevant procedures.

Last week, Bitcoin was able to rise from just over 80K to 98K today, all thanks to the help of MicroStrategy. Yes, MicroStrategy issued additional shares and sold them for $4.6 billion.

PS: Companies with a higher trading volume than Nvidia are naturally entitled to this liquidity.

Sometimes, if you admire a company for making great profits, you need to admire its great courage.

Unlike many cryptocurrency companies that sell stocks and then cash out, WeCare has gone all out as usual. WeCare reinvested all the money from the sale of stocks into Bitcoin, pushing Bitcoin to 98K.

By now, you should have understood Wei Ce's magic:

Buy Bitcoin → Stock price rises → Take on debt to buy more Bitcoin → Bitcoin rises → Stock price rises further → Take on more debt → Buy more Bitcoin → Stock price continues to rise → Issue additional shares and sell for cash → Buy more Bitcoin → Stock price continues to rise…

Presented by the great magician Wei Ce.

MicroStrategy's nearest debt repayment date is 2027, so we still have at least 3 years to go.

As long as you are a magician, there will come a time when your magic tricks are exposed.

Many MSTR bears believe that it has now reached the left side of the standard and even suspect that it has reached the Luna moment.

However, is this really the case?

According to recent statistics, MicroStrategy's average cost of Bitcoin is US$49,874, which means that it is now close to a floating profit of 100%, which is a super thick safety cushion.

Let’s assume the worst case scenario. Even if Bitcoin drops 75% (almost impossible) to 25,000, what will happen?

MicroStrategy borrowed off-market leverage and had no liquidation mechanism. Angry creditors could at most convert their bonds into MSTR stocks at a specified time and then angrily dump them into the market.

Even if MSTR is smashed to zero, it still does not need to be forced to sell these bitcoins, because the earliest due date for MicroStrategy's debt repayment is February 2027.

Look carefully, this is not 2025, nor 2026, but Tom's 2027.

In other words, it will take until February 2027, and if Bitcoin plummets, and no one wants MicroStrategy's stock anymore, then MicroStrategy will need to sell part of its Bitcoin in February.

All in all, there are still more than two years to continue playing music and dancing.

This is the magic of off-market leverage.

You may ask, is it possible that WeStrategy will be forced to sell Bitcoin due to interest rates?

The answer is still no.

Since the creditors of MicroStrategy's convertible bonds are generally guaranteed to make money, the interest rate is quite low. For example, the interest rate for this bond due in February 2027 is 0%.

The creditors are simply after MSTR's stock.

The interest rates of several debts it subsequently issued were also 0.625% and 0.825%. Only one debt was 2.25%, which has a very small impact, so there is no need to worry about its interest.

MicroStrategy's main bond interest, source: bitmex

The only soft threat to WeStrategy is the Bitcoin whale

At this point in the process, WeStrategy and Bitcoin have become mutually causal.

More companies are ready to start learning from the great David Copperfield (Saylor) of Bitcoin.

For example, MARA, a listed Bitcoin mining company, has just issued $1 billion in Bitcoin convertible bonds, specifically for the purpose of bottom fishing.

So I think the bears had better act with caution. If more people start to follow MicroStrategy’s lead, Bitcoin’s momentum will be like a runaway horse, after all, there is a vacuum above.

Therefore, WeStrategy’s biggest rivals now are only those ancient Bitcoin whales.

As many people have predicted before, retail investors have already handed over all the bitcoins they had. After all, there are too many opportunities, such as the meme trend. I don’t believe that everyone will just sit there with empty eyes.

Therefore, there are only these whales in the market, and as long as these whales do not move, this momentum will be difficult to stop. If they are luckier, the whales and WeStrategy will form some small tacit understandings, which will be enough to push Bitcoin into a greater future.

This is also a major difference between Bitcoin and Ethereum: Satoshi Nakamoto theoretically owns nearly 1 million bitcoins mined in the early days, but there has been no news to this day; and for some reason, the Ethereum Foundation sometimes particularly wants to sell 100 ETH to test liquidity.

As of the date of writing, WeStrategy has achieved a floating profit of US$15 billion, all thanks to loyalty and faith.

Since it is making money, it will invest more, it can’t turn back, and more people will follow suit. At the current momentum, 170K is the medium-term target for Bitcoin (not financial advice).

Of course, we are used to seeing conspiracy groups designing conspiracies in memes every day. Occasionally, we see a truly top-notch conspiracy, and we are truly amazed.