Author: Alice@ForesightVentures

In the previous article, we analyzed the overall ecological landscape of the PayFi track. This time, let’s take a deep look at several new application scenarios with great potential: AI payment, micropayments for consumers, and innovative deposit and withdrawal solutions.

1. AI Payment

We firmly believe that AI and crypto payment have huge market potential. AI payment is expected to subvert many industries outside of traditional finance, such as data annotation, model training, and content creation. As AI agents gradually integrate into daily life, the application scope of crypto payment will also expand to mainstream industries. In the future, AI assistants will even be able to help you proactively order takeout, buy clothes and groceries, arrange taxis to meetings, etc.

Market Opportunities

- Sources of income for AI payment platforms: Transaction fees, subscription fees, or micropayment systems for various AI services are all revenue channels for AI payment platforms.

- Stablecoin settlement advantages: Stablecoin transactions can achieve real-time settlement of cross-border remittances around the clock. Compared with the traditional banking system, it is not only faster but also has lower fees, which is very suitable for AI-driven small transaction needs.

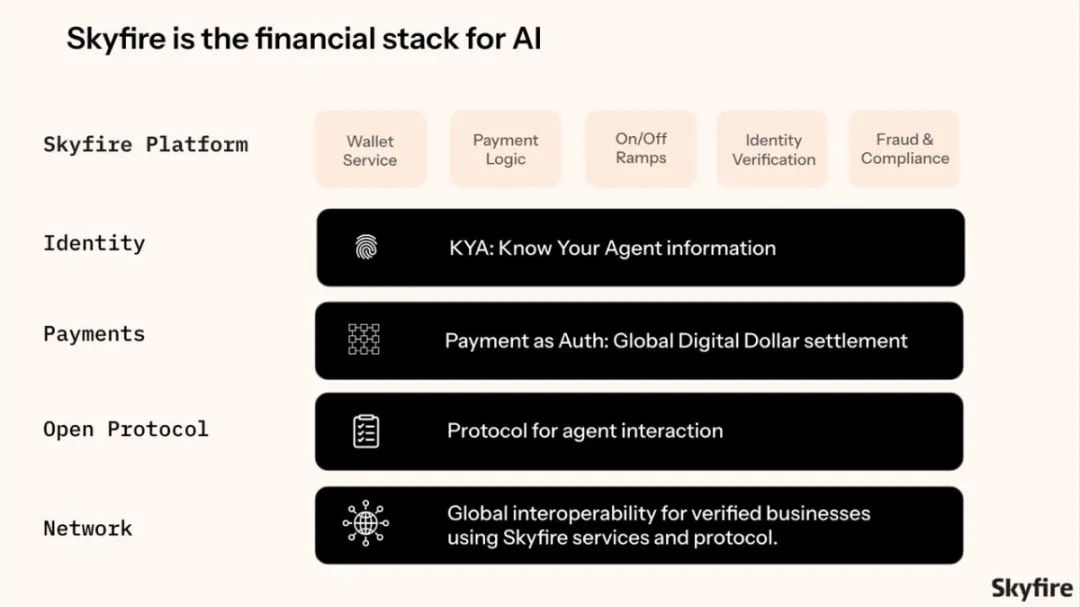

Example: Skyfire

Skyfire Technology is committed to building a powerful and scalable payment infrastructure for AI agents and users. It mainly includes the following key parts:

Payment and wallet infrastructure:

Skyfire Wallet Service: Provides access to funds for global transactions.

Payment-as-Auth: Enables real-time settlement of USDC.

Micropayment support: Enables AI agents to conduct permissionless, high-frequency, low-value transactions.

Open Protocol (AI Market): Integrate all AI-related products and services. AI agents can connect to the resources they need to work through the Skyfire open protocol (market) and pay for these services with the Skyfire API. For example, decentralized computing power market, decentralized data annotation market, automated data sets, AI model API, etc.

Identity and verification layer: Give each AI agent an identity (KYA), and provide identity identification for all agents, users, and enterprises using Skyfire products. KYA can track transaction history, ensure compliance and accountability, and verify the identity of each transaction to ensure security.

Integration Tools: Support for over 160 Large Language Models (LLMs), API access to datasets, premium content, and web services, and tools for developers to integrate Skyfire into their systems.

Key success factors

AI payment layer network effect: Skyfire is a platform that integrates AI market and payment layer. On the one hand, by integrating various AI markets and service providers, it attracts more users and AI agents to use its products; on the other hand, it also creates income for more Web2 and Web3 AI service providers (with the help of stablecoin transactions, the efficiency and frequency of transfers can be significantly improved), thus forming a bilateral flywheel effect.

Compliance and security: Verifiable identity (KYA) and transaction history ensure the security of transactions and effectively prevent fraud. The payment authorization system further enhances transaction trust.

Strong community: Collaboration with LLM providers, data markets, and enterprise AI companies has consolidated its ecosystem. Currently, more than 1,500 developers are using Skyfire's tools and services.

2. Small-value payments for consumers

Crypto-based consumer micropayments, combined with innovative models like Moonshot (buying and selling Meme coins with crypto) and Sidekick (providing Web3 payment gateways for live streamers), demonstrate the huge potential of global instant settlement and decentralized protocols. By cutting out intermediaries and costs, this model has the potential to disrupt industries such as cryptocurrency trading, content creation, gaming, and live streaming, especially in emerging markets. Low commission rates, cross-border payment convenience, and high mobile penetration make cryptocurrency an ideal solution.

Market Opportunities

Target market: Covering daily consumer transaction scenarios such as taxi-hailing, gaming, digital media, live streaming, content creators, and online communities.

Revenue sources: transaction fees, revenue from cooperation with content platforms, and revenue from the integration of decentralized finance (DeFi).

Example: Moonshot

Moonshot is a trading platform that supports users to buy and sell Meme tokens using Apple Pay and other methods. Its main features are as follows:

Self-hosted wallets: Users can create accounts with email and password (with Touch ID, Face ID or password). Moonshot uses its multi-party computation (MPC) partner Turnkey.com to generate embedded wallets for supported blockchains.

Fee structure: Moonshot charges fees for transactions to cover administrative costs and ensure a smooth experience. Fees are tiered based on transaction amount, and network fees are paid by the platform to prioritize orders. For example, transactions between $1 and $250 are charged 2.5%, with a minimum of about $0.40; transactions over $250 are charged 1%.

Referral Program: Users can get rewards by recommending friends to use the platform. When the referrer and the referee complete identity verification, both parties can get rewards. Currently, this program is only available to iOS users in some regions.

Key Success Factors

User-friendly interactive design: Moonshot’s interface is simple and intuitive, simplifying the buying and selling process of Meme cryptocurrency. By supporting legal payment methods such as Apple Pay, credit cards, and PayPal, it lowers the entry barrier for new users.

Token launch speed: The ability of the platform to quickly launch popular Meme tokens is crucial. For example, the launch of MOODENG has greatly increased user engagement and transaction volume, demonstrating Moonshot’s ability to grasp market trends.

Efficient referral mechanism: Moonshot’s referral system drives user growth, enhances community interaction, and accelerates platform adoption by rewarding referrers and new users.

Compliance and security: The platform strictly abides by local regulations and has taken strong security measures such as working with MoonPay for identity verification and transaction processing. This compliance and security construction enhances user trust and lays the foundation for sustainable development.

Case: Sidekick

Sidekick is a Web3 gaming companion platform and payment gateway where streamers can receive micropayments and rewards via Crypto.

Key Success Factors

- Solve the creator payment problem: Traditional streaming platforms (such as YouTube, Twitch and TikTok) take a commission of up to 30%, have a long payment cycle (usually taking several weeks), and are subject to geographical restrictions. Sidekick provides instant, low-cost blockchain payments, effectively solving these problems. For global content creators, especially those in areas where traditional payment systems are not well covered, it solves a very big pain point.

- Low-cost transactions promote income equality: Sidekick allows mid-level influencers to earn higher incomes in transactions. By eliminating the Web2 platform's commission, Sidekick ensures a more equitable and reasonable income distribution. This is very attractive to gig economy workers who are looking for better income sharing and faster payments.

- Scalability through Web3 infrastructure: Sidekick uses the Web3 protocol to ensure that its payment gateway is decentralized, scalable, secure and reliable. The transparency and security of the blockchain provide a foundation of trust for creators and users, while also enabling Sidekick to meet the needs of transactions ranging from a small amount to millions of transactions per day.

- The future of the creator economy: As the creator economy grows, platforms like Sidekick are taking the lead in decentralized, cryptocurrency-native monetization. With the growing popularity of NFTs, digital assets, and Web3 applications, Sidekick can serve as a comprehensive payment solution. Streamers and creators can not only earn income through regular live broadcasts, but also monetize their influence through tokenized content and fan tokens.

(III) Innovative deposit and withdrawal solutions

Efficient deposit and withdrawal solutions play a key role in the mass adoption of cryptocurrencies. These solutions build a bridge for users and institutions that rely on fiat currencies to enter crypto assets or participate in decentralized finance (DeFi).

Market Opportunities

- Rising demand for stablecoins: The increasing use of stablecoins (such as USDC, USDT, DAI) in remittances, DeFi, and cross-border trade has given rise to demand for conversion between fiat currencies and stablecoins. After the US election, the laws and regulations related to stablecoins are expected to be more complete, and there will be greater room for development after compliance.

- Layer-2 and multi-chain expansion: The deposit and withdrawal platform can be combined with Layer-2 networks (such as Optimism, Arbitrum) and cross-chain support (such as Solana, Avalanche) to reduce costs, increase transaction speed, and enable users to access a diverse crypto ecosystem.

- Improved accessibility: Embedded payment solutions and wallet-free access (via email or mobile) simplify onboarding to cryptocurrencies, attracting new users and driving wider adoption.

- Emerging market potential: Deposit and withdrawal platforms often use mobile products to penetrate emerging markets with weak financial infrastructure, while providing enterprise-level tools and collaborating with partners such as Visa and Stripe to enter institutional and traditional payment networks.

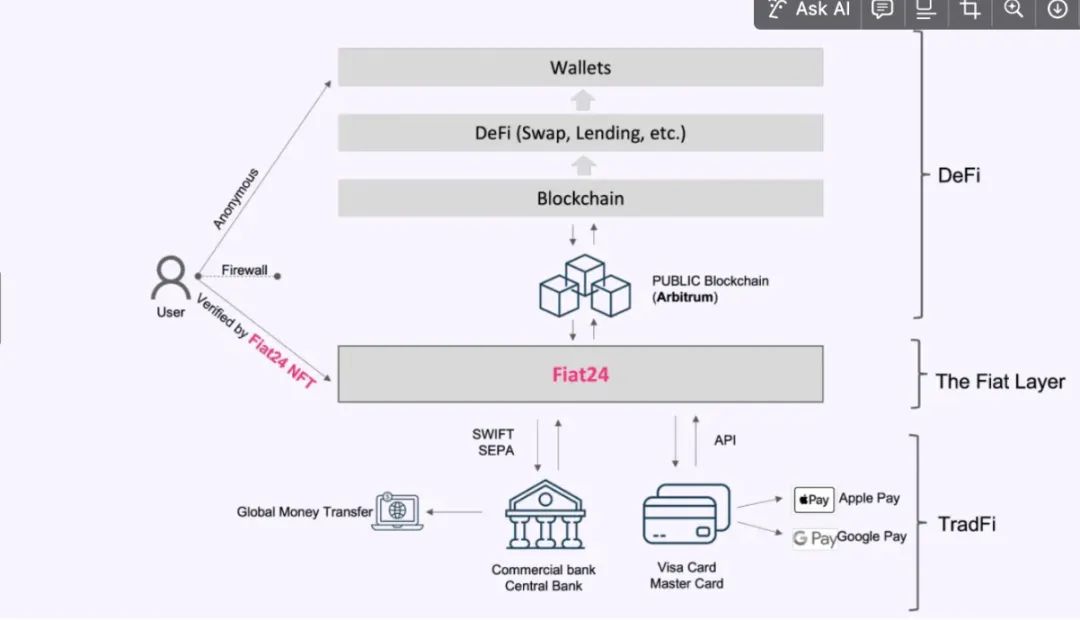

Case: Fiat24

Fiat24 is a Web3 neo-bank that provides users with a seamless, zero-cost conversion experience between fiat and cryptocurrency. Its main product features include:

- Tokenized deposits: Fiat24 presents fiat currencies (such as CHF, EUR, USD, GBP) in the form of ERC-20 tokens on the Ethereum blockchain. Each token corresponds 1:1 to the managed fiat currency, ensuring stability and credibility. The system supports instant and transparent transactions and can be seamlessly connected with DeFi services.

- NFT-based account access: Users are given a unique non-fungible token (NFT) as their digital identity to access their Fiat24 account. This replaces traditional usernames and passwords, increasing security and user control. NFTs are stored in the user's Arbitrum (Ethereum) wallet and used to access Fiat24 services.

- Visa Debit Card Integration: Fiat24 provides Visa debit cards that are linked to user accounts and support global spending at over 40 million merchants. Users can top up their cards through Fiat24’s decentralized application (dApp) and display their balance in a specified currency.

- Compliance assurance: Fiat24 is operated by SR Saphirstein AG and is regulated by the Swiss Financial Market Supervisory Authority (FINMA). The platform complies with anti-money laundering (AML) requirements and undergoes regular financial and regulatory audits by Swiss Grant Thornton to ensure user compliance and fund security.

Fiat24's key success factors

- Strong network effects: The key to Fiat24’s success is establishing its tokenized deposits as a universal standard. This foundational role promotes interoperability and builds a self-reinforcing ecosystem for connecting traditional finance (TradFi) and decentralized finance (DeFi).

- Regulatory advantages and cost leadership: With a Swiss banking license, Fiat24 has the endorsement of the traditional financial system and access to the SWIFT/SEPA network. This regulatory status enables it to offer highly competitive prices to partners and users, becoming a trusted and efficient web3 banking solution.

- Fiat-Crypto Fusion: Through tokenized bank deposits (such as USD24), instant fiat-crypto conversions, and synchronized on-chain/off-chain ledgers, Fiat24 seamlessly bridges traditional and decentralized finance, creating a smooth and user-friendly ecosystem.

- Scalable Partnerships: Fiat24 offers an all-in-one Web3 banking solution that is easily integrated with major wallets and exchanges, expanding adoption through a profit-sharing model, driving network growth, and enhancing the platform’s utility.

Conclusion

We believe that blockchain has great potential to redefine the global payment system. From AI-driven micro-transactions to consumer micro-payments to fiat-to-cryptocurrency conversion solutions, PayFi's innovations solve the long-standing inefficiencies in traditional finance and open up broad market opportunities. The integration of cryptocurrencies, stablecoins, and decentralized finance paves the way for scalable, secure, and cost-effective solutions.

PayFi is like a bridge, leading us to a more inclusive, transparent and efficient financial future. Although there are still challenges in regulation and infrastructure, the prospects are bright and the future is promising.