Author: 0xjs, Golden Finance

Bitcoin breaks through $80,000! Bitcoin breaks through $90,000! Bitcoin breaks through $95,000! Bitcoin breaks through $99,000!

It is clear that Bitcoin is set to break through the $100,000 mark soon.

Common sense tells us that the direct reason for the sharp rise in prices is that someone is buying in large quantities with real money, after all, "Money Talks".

In this round of crypto bull market, crypto tokens are severely divided, and the two sectors with the best performance are Bitcoin and Solana. Solana's rise is mainly driven by the influx of crypto players into Meme, while Bitcoin's rise is mainly driven by the purchase of funds from US Bitcoin ETFs and some listed companies, especially MicroStrategy. In this article, we mainly focus on MicroStrategy.

On November 21, Golden Finance reporter spent an evening browsing the documents submitted by MicroStrategy since 2021 on the official website of the US SEC, deeply dissecting MicroStrategy's purchase of Bitcoin and the source of funds. The conclusion is that MicroStrategy is an enhanced version of "Grayscale + Luna".

Let’s first look at the overall situation of MicrosStrategy, then analyze the source of funds for MicroStrategy’s purchase of Bitcoin, and finally compare Grayscale and Luna. Below.

MicroStrategy is not afraid of bull and bear markets: it has spent more than $16 billion to buy Bitcoin

MicroStrategy has implemented the Bitcoin reserve strategy since September 2020, and has firmly implemented the Bitcoin reserve strategy across cycles without fear of bull and bear markets for four years. For example, it bought Bitcoin for more than US$59,000 in April and November of the bull market in 2021.

MicroStrategy continues to buy BTC

Golden Finance reporters found that as of November 22, 2024, MicroStrategy has spent a total of US$16.58 billion to buy Bitcoin and currently holds 331,000 Bitcoins with a market value of nearly US$33 billion.

Since the successful launch of the Bitcoin ETF in January 2024, the Bitcoin ETF has managed more than 1.24 million Bitcoins, with total assets exceeding $120 billion and total net capital inflows of approximately $30.3 billion. The Bitcoin ETF is an investment target for many investors, not just one investor.

As far as we can see, MicroStrategy may be the single entity that has spent the most on buying Bitcoin.

So the question is, where does MicroStrategy get so much money to buy Bitcoin?

Golden Finance reporter read the report submitted by MicroStrategy to the US SEC and found that its funds mainly come from two sources: Convertible Senior Notes and At-the-Market Equity Offerings.

Among them, Convertible Senior Notes are aimed at qualified institutional investors, and At-the-Market Equity Offerings are directly aimed at the secondary market.

Convertible Senior Notes: $7.26 billion from qualified institutional investors

Below are the notes issued by MicroStrategy since 2020. Except for the $500 million senior secured bonds issued in June 2021, the rest are convertible senior notes.

Among them, the cash from the newly issued $3 billion convertible bonds of MicroStrategy on November 21, 2024 can be used at any time to buy Bitcoin. Perhaps in the next one or two days, when MicroStrategy uses this $3 billion to buy Bitcoin, Bitcoin will break $100,000.

Understand what Convertible Senior Notes are and you will find that it is really a good financial tool.

A convertible senior note is a special debt security that contains an option to convert the note into a predetermined number of the issuer's shares. If the stock price rises, it can be converted into shares. If the stock price is low, the principal and interest will be paid according to the debt. In addition, the convertible senior note takes precedence over all other debt securities issued by the same organization and can be compensated first. Therefore, it is a bond with high returns on the top and a guaranteed bottom line.

Importantly, convertible preferred bonds are generally accompanied by a mandatory redemption clause. After the prohibited redemption period specified in the clause has passed or when the early redemption clause is triggered, the issuer can initiate a mandatory redemption. Before the specified redemption date, investors need to convert the convertible bonds into company stocks, otherwise the issuer has the right to force the redemption of the convertible bonds at the price of the bond face value plus accrued interest. In most cases, investors will take the initiative to convert to stocks.

Take the 2025 Convertible Notes that MicroStrategy has already redeemed as an example. The maturity date of the 2025 Convertible Notes is December 15, 2025. However, MicroStrategy issued an announcement on June 13, 2024, requiring the holders of the 2025 Convertible Notes to choose to convert the notes at the applicable conversion rate of 2.5126 shares of MicroStrategy Class A common stock for every $1,000 principal (reflecting a conversion price of $397.99 per share) before 5:00 p.m. New York time on July 11, 2024. Otherwise, MicroStrategy will force the redemption of all outstanding notes on July 15, with the redemption price equal to the principal + accrued unpaid interest.

The stock price of MicroStrategy on that day was about $1,300 (MicroStrategy completed a 1:10 stock split on August 8, and the price of $1,300 was the price before the split). Obviously, creditors will choose to convert debt into stocks. After receiving the stocks, creditors will complete arbitrage.

Why do institutional investors buy MicroStrategy's convertible bonds? Because the risk is minimal, and it is basically guaranteed to make money. The preferred convertible bonds have priority claims. Currently, MicroStrategy's total convertible bond liabilities are $7.26 billion, and the market value of Bitcoin held by MicroStrategy is nearly $33 billion. Even if Bitcoin falls by 75%, MicroStrategy's convertible bond creditors will not lose money.

It can be said that the most important motivation behind convertible bonds is that the issuer allows investors to actively choose to convert debt into stocks, so that the issuer does not have to use cash to repay the debt.

At-the-Market Equity Offerings: Nearly $10 billion in secondary markets

Below is MicroStrategy's market stock issuance data since 2020. In the past four years, MicroStrategy has raised a total of US$9.8235 billion directly through the issuance of new shares in the secondary market, and all of these funds have been used by MicroStrategy to buy Bitcoin.

The so-called ATM Equity Offering refers to the subsequent stock issuance conducted by a listed company after its IPO in order to raise funds. In an ATM offering, a listed company sells newly issued shares to the secondary trading market gradually over a period of time at the then current market price through a designated broker. The broker sells the issuing company's shares on the open market for cash proceeds, which are then delivered to the issuing company.

Let's take MicroStrategy's ATM Equity Offering as an example. On August 1, 2024, MicroStrategy signed a sales agreement (the "August 2023 Sales Agreement") with TD Securities (USA), The Benchmark Company, BTIG, Canaccord Genuity, Maxim Group and SG Americas Securities brokers. Under the agreement, MicroStrategy may issue and sell its Class A common stock from time to time through sales agents, with a maximum of $2 billion in stock issued. According to the 8-K filing MicroStrategy provided to the U.S. SEC on November 11, 2024, MicroStrategy issued a total of 7,854,647 new shares, received a total of $2.03 billion, and bought all 27,200 bitcoins.

On October 30, 2024, MicroStrategy released the 21/21 plan, saying that it would raise $42 billion in capital in the coming years, including $21 billion in equity and $21 billion in fixed-income securities, to invest in Bitcoin. MicroStrategy disclosed on the same day that MicroStrategy and TD Securities (USA), Barclays Capital, The Benchmark Company, BTIG, LLC, Canaccord Genuity, Cantor Fitzgerald & Co., Maxim Group, Mizuho Securities USA, and SG Americas Securities reached a sales agreement to issue $21 billion of MicroStrategy shares at market price. The 8-K filing submitted by MicroStrategy to the SEC on November 18, 2024 showed that MicroStrategy sold 13.594 million shares between November 11 and 17, earning approximately $4.6 billion and buying all 51,780 bitcoins.

Under MicroStrategy's plan, brokers still have about $16.4 billion in newly issued MicroStrategy shares to sell.

Why MicroStrategy is an enhanced version of "Grayscale+Luna"

Now that you are familiar with MicroStrategy's "convertible bonds" and "market-priced stock issuance" cheat codes, think back and wonder if they are very similar to Grayscale and Luna in the last bull market, and they are enhanced versions.

Grayscale Vs. Convertible Bonds:

Let's review Grayscale's operating mechanism before it was converted into an ETF. Grayscale Trust shares are only issued to qualified investors. Investors use over-the-counter cash to purchase GBTC shares (Grayscale Trust's underlying assets must be corresponding Bitcoin assets) or exchange physical Bitcoin for GBTC shares. After locking up for 6 months, they can be traded publicly to complete arbitrage. At the same time, GBTC shares are isolated from the underlying Bitcoin assets and investors cannot redeem them.

MicroStrategy's Convertible Senior Notes are also for qualified investors. Investors use over-the-counter cash to buy convertible bonds, and when they are redeemed, they are converted into MicroStrategy shares to complete arbitrage. Convertible Senior Notes are also isolated from MicroStrategy's Bitcoin.

During the Bitcoin bull market in 2020 and 2021, the premium of GBTC attracted a large amount of arbitrage funds, and GBTC once accumulated more than 650,000 bitcoins, which was called an "open bull market" by many industry insiders at the time.

During this bull market, MicroStrategy has attracted more than $7 billion in qualified institutional investor funds through convertible bonds, and MicroStrategy's 21/21 plan also plans to issue more bonds.

The difference is that MicroStrategy's convertible bonds have a long maturity date, with the nearest maturity date being in 2027, which is enough to last until the next cycle. If necessary, MicroStrategy can force the redemption of convertible bonds, allowing investors to convert convertible bonds into newly issued MicroStrategy shares at almost 0 cost, without MicroStrategy really having to pay back the money. Even if it is redeemed until the maturity date, MicroStrategy can issue new convertible bonds to replace the old ones, just as MicroStrategy redeemed the 2028 Secured Notes with cash from the 2028 Convertible Notes issued on September 20, 2024. Obviously, MicroStrategy's convertible bonds are more stable.

Luna Vs. Market-Priced Equity Offerings:

In the case of Luna, burning $1 of LUNA can mint $1 of algorithmic stablecoin UST. As long as the price of LUNA rises, more UST can be minted. With more UST, more Bitcoin can be purchased as reserves, stabilizing 1UST=1USDT. Luna is directly available to ordinary investors without permission.

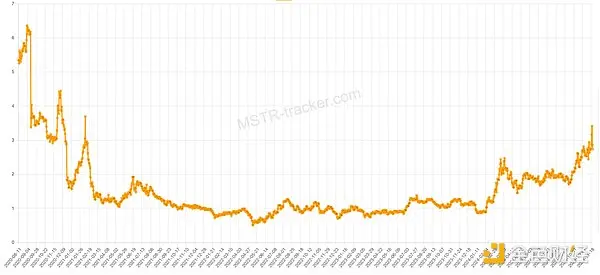

MicroStrategy's market-priced stock offering is very similar to this, and is also directly aimed at ordinary investors in the secondary market. The higher MicroStrategy's stock price is, the more US dollars it can obtain through market-priced stock offerings, and more US dollars can buy more Bitcoin. "Left foot on right foot" goes up all the way. After the Bitcoin ETF established a bull market in January 2024, MicroStrategy's net asset premium (market price per share/corresponding Bitcoin value-1) climbed all the way to 2.7. MicroStrategy currently holds a total of 331,200 bitcoins, worth approximately US$32.84 billion, and MicroStrategy's total market value once exceeded US$100 billion.

Luna and UST can be minted in both directions. If UST is decoupled, arbitrageurs can buy UST at a discount and mint LUNA at 1UST=1USDT, forming a "death loop" and causing LUNA to collapse. In fact, if the Luna Foundation LFG bought more Bitcoin earlier in the rising cycle (it only bought $1.5 billion in Bitcoin), and if UST to LUNA could be minted in one direction temporarily, Luna would probably not collapse.

MicroStrategy goes one step further. MicroStrategy's market-priced stock issuance is one-way, will not fall into a death spiral, and is almost 0 cost. MicroStrategy is obviously safer than Luna. Even during the bear market in 2022, MicroStrategy's net asset premium is at least 60%.

Source: mstr-tracker

As long as someone is willing to buy MicroStrategy shares issued at market prices, the more Bitcoin MicroStrategy buys during its high NAV premium, the thicker MicroStrategy's safety cushion will be. At the extreme, MicroStrategy's market value is exactly equal to its Bitcoin market value, and MicroStrategy itself will not have any risk because the risk has been transferred to stock investors.

To sum up, can we say that MicroStrategy is an enhanced version of "Grayscale+Luna"?

Conclusion: Triple Maximalism

At the Bitcoin Conference held in Nashville at the end of July 2024, MicroStrategy CEO Michael Saylor delivered a keynote speech on "Bitcoin Revolution".

After four years of practice, he proposed a methodology for individuals, companies, institutions and countries to deal with the Bitcoin revolution. He proposed a triple maximalist strategy. For companies, it is to buy Bitcoin through three channels: cash flow, issuing stocks when the stock price is overvalued, and issuing debt when the interest rate is low.

He said it and did it.

MicroStrategy has hoarded 331,200 bitcoins.