Article author: DC | In SF

Article translation: Block unicorn

Ethena is the most successful protocol in the history of DeFi. About a year ago, its total locked value (TVL) was less than $10 million, and today it has grown to $5.5 billion. It is integrated into multiple protocols in various ways, such as @aave, @SkyEcosystem (IE Maker/Sparklend), @MorphoLabs, @pendle_fi, and @eigenlayer. There are so many protocols working with Ethena that I have had to change covers several times when recalling another partner. Six of the top ten protocols by TVL are either working with Ethena or are Ethena themselves (Ethena ranks ninth). If Ethena fails, it will have a profound impact on many protocols, especially AAVE, Morpho, and Maker, which will fall into varying degrees of functional insolvency. At the same time, Ethena has significantly increased the usage of DeFi as a whole through its multi-billion dollar growth, similar to the impact of stETH on Ethereum DeFi. So, is Ethena destined to destroy DeFi as we know it, or will it usher in a new renaissance for DeFi? Let’s dive into this question.

How does Ethena work?

Despite being out for over a year, there is still widespread misunderstanding about how Ethena works. Many people claim it is the new Luna and then refuse to elaborate further. As someone who warned about Luna, I find this view very biased, but I also believe that most people lack sufficient understanding of the details of how Ethena works. If you think you fully understand how Ethena manages delta neutral positions, custody, and redemptions, please skip this section, otherwise it is important reading to fully understand.

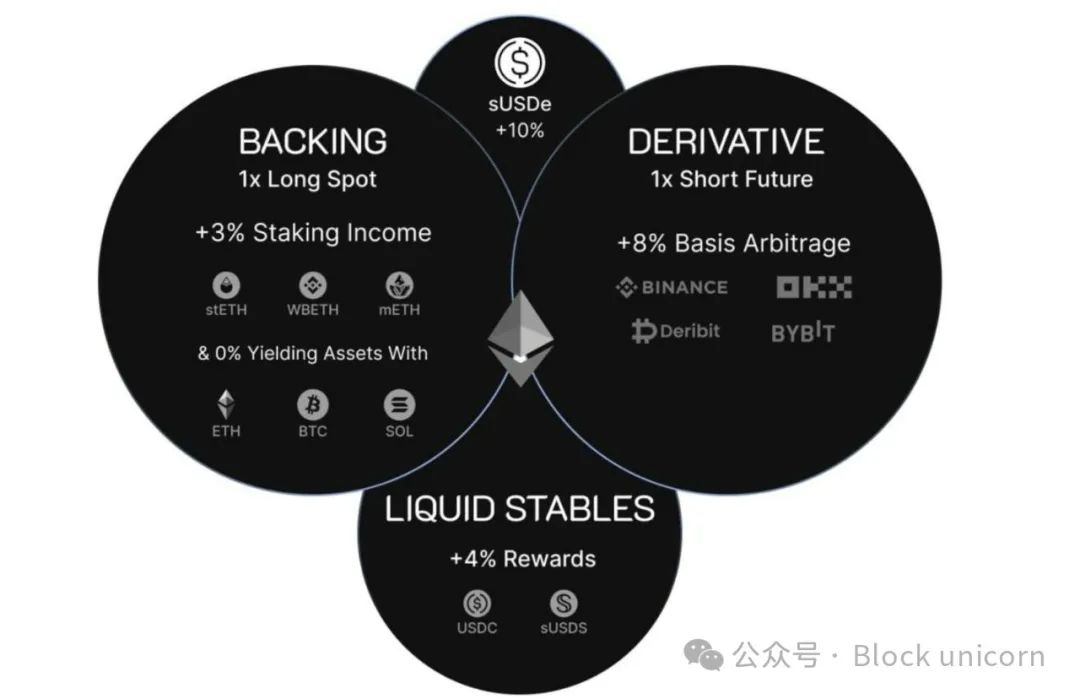

Overall, Ethena benefits from financial speculation and the cryptocurrency bull run, just like BTC, but in a more stable way. As cryptocurrency prices rise, more and more traders want to go long on BTC and ETH, while fewer and fewer traders are willing to go short. Due to supply and demand, traders who go short are paid by traders who go long. This means that a trader can hold BTC while shorting the same amount of BTC, thereby achieving a neutral position, where the gains and losses of the long and short positions cancel each other out when the price of BTC rises, while the trader still earns interest income. Ethena operates entirely on this mechanism; it takes advantage of the lack of sophisticated investors in the crypto market who prefer to profit by earning yield rather than simply going long on BTC or ETH.

However, a significant risk to this strategy is the custodial risk of exchanges, which was demonstrated by the collapse of FTX and its impact on the first generation of Delta Neutral managers. Once an exchange fails, all funds may be lost. This is why mainstream managers who manage capital efficiently and safely have been greatly negatively affected by the collapse of FTX, the most obvious example being @galoiscapital, which was not their fault. Exchange risk is one of the important reasons that prompted Ethena to choose to use @CopperHQ and @CeffuGlobal. These custodians act as trusted middlemen, holding assets and facilitating Ethena's interaction with exchanges while avoiding exposing Ethena to the custodial risk of exchanges. Exchanges in turn can rely on Copper and Ceffu because they have legal agreements with custodians. The total profit and loss (i.e. the amount Ethena needs to pay to long traders, or the amount that long traders owe Ethena) is settled regularly by Copper and Ceffu, and Ethena systematically rebalances its positions based on these settlement results. This custody arrangement effectively reduces exchange-related risks while ensuring the stability and sustainability of the system.

Minting and redeeming USDe/sUSDe is relatively simple. USDe can be purchased or minted using USDC or other major assets. USDe can be staked to generate sUSDe, which earns yield. sUSDe can then be sold to the market by paying the corresponding swap fee, or redeemed for USDe. The redemption process usually takes seven days. USDe can then be exchanged for supporting assets at a 1:1 ratio (corresponding to $1 in value). These supporting assets come from the asset reserve and the collateral used by Ethena (mainly BTC and ETH/ETH derivatives). Given that some USDe are not staked (many of which are used in Pendle or AAVE), the yield generated by the assets backing these unstaked USDe helps enhance the yield of sUSDe.

To date, Ethena has been able to handle a large number of withdrawals and deposits with relative ease, although at times the slippage on USDe-USDC has been as high as 0.30%. This slippage is relatively high for a stablecoin, but it is far from a significant decoupling and far from being dangerous to lending protocols, so why are people so worried?

Well, if there is a large withdrawal demand, say 50%

How to make Ethena "fail"?

Given that we now understand that Ethena's yields are not "fake" and how it works at a more granular level, what are the main real concerns about Ethena? Basically, there are a few scenarios. First, the funding rate could go negative, in which case Ethena would end up losing money instead of making money if Ethena's insurance fund (currently around $50 million, enough to withstand a 1% slippage/funding loss at current TVL) is not enough to cover losses. This scenario seems relatively unlikely, as most users would likely stop using USDe when yields decrease, which has happened in the past.

Another risk is custody risk, which is the risk that Copper or Ceffu attempts to operate with Ethena's money. This risk is mitigated by the fact that the custodian does not fully control the assets. The exchange does not have signing authority and cannot control any wallets holding the underlying assets. Both Copper and Ceffu are "omnibus" wallets, which means that all institutional users' funds are mixed in hot/warm/cold wallets, and there are multiple risk protection measures such as governance (i.e. controls) and insurance. From a legal perspective, this is a bankruptcy remote trust structure, so even if the custodian goes bankrupt, the assets held by the custodian are not the property of the custodian, and the custodian has no claim on these assets. In practice, there is still a simple negligence and centralization risk, but there are indeed many protections to avoid this problem, and I think the possibility of this happening is equivalent to a black swan event.

The third and most commonly discussed risk is liquidity risk. To manage redemptions, Ethena must sell both its derivatives positions and its spot positions. This can be a difficult, expensive, and potentially time-consuming process if the price of ETH/BTC fluctuates wildly. Currently, Ethena has prepared hundreds of millions of dollars to be able to redeem USDe for USD at a 1:1 ratio because it holds a large stable position. However, if Ethena accounts for an increasing proportion of total open interest (i.e. all open derivatives), this risk is relatively serious and could cause Ethena's net asset value (NAV) to fall by several percentage points. However, in this case, the insurance pool is likely to fill the gap, and this alone is not enough to cause a catastrophic failure of the protocol that uses it, which naturally leads to the next topic.

What are the risks of using Ethena as a protocol?

Broadly speaking, Ethena's risks can be divided into two core risks: USDe liquidity and USDe solvency. USDe liquidity refers to the actual cash available, willing to buy USDe at a base value of $1 or 1% below that base value. USDe solvency means that even if Ethena may not have cash at a certain moment (such as after a long period of withdrawals), it can obtain this cash if there is enough time to liquidate the assets. For example, if you lend your friend $100,000 and he has a house worth $1 million. It is true that your friend may not have ready money and he may not be able to take it out tomorrow, but if he is given enough time, he will most likely be able to raise enough money to pay you back. In this case, your loan is healthy, and your friend is just illiquid, that is, his assets may take a long time to sell. Bankruptcy essentially means that liquidity should be non-existent, but limited liquidity does not mean that assets are bankrupt.

Ethena, in partnership with some protocols such as EtherFi and EigenLayer, would only face significant risk if Ethena were to become insolvent. Other protocols, such as AAVE and Morpho, could face significant risk if Ethena’s products were illiquid for an extended period of time. Currently, on-chain liquidity for USDe/sUSDe is approximately $70 million. While quotes are available through the use of aggregators that say up to $1 billion of USDe can be exchanged for USDC at a 1:1 ratio, this is likely due to the current huge demand for USDe, as it is intent-based demand, and this liquidity could dry up in the event of large-scale redemptions on Ethena. When liquidity dries up, Ethena will be under pressure to manage redemptions to restore liquidity, but this may take time, which AAVE and Morpho may not have enough time.

To understand why this happens, it is important to understand how AAVE and Morpho manage liquidations. Liquidations occur when the debt position on AAVE and Morpho is unhealthy, i.e. exceeds the required loan-to-value ratio (ratio between loan amount and collateral). Once this happens, the collateral is sold to repay the debt, a fee is charged and any remaining funds are returned to the user. In short, if the value of the debt (principal + interest) approaches a predetermined ratio compared to the value of the collateral, the position will be liquidated. When this happens, the collateral is sold/converted into debt assets.

Currently, a lot of people use these lending protocols, depositing sUSDe as collateral to borrow USDC as debt. This means that if a liquidation occurs, a large amount of sUSDe/USDe will be sold for USDC/USDT/DAI. If this all happens at the same time, and accompanied by other violent market fluctuations, it is very likely that USDe will lose its peg to the dollar (if the liquidation is very large, certainly in the case of around $1 billion). In this case, a large amount of bad debt could theoretically be generated, which is acceptable for Morpho because vaults are used to isolate risks, although some income-generating vaults will be negatively affected. For AAVE, the entire core pool will be negatively affected. However, in this potential scenario where it is purely a liquidity issue, adjustments may be made to the way liquidations are managed.

If a liquidation could result in a bad debt, instead of immediately selling the underlying asset into an illiquid market and leaving AAVE holders with the difference, the AAVE DAO could assume responsibility for the tokens and position but not sell the collateral immediately. This would allow AAVE to wait until the price and Ethena’s liquidity stabilize, allowing AAVE to make more money on the liquidation (rather than a net loss) and for users to receive funds (rather than nothing because there was a bad debt). Of course, this system only works if USDe returns to its previous value, and if not, the bad debt situation will be worse. However, if there is an as-yet-undiscovered high-probability event that could cause the token value to go to zero, then it is unlikely that liquidation would gain more value than waiting, with perhaps a 10-20% difference as individual holders realize and start selling positions faster than the parameters change. This design choice is important for assets that could have liquidity issues in a frothy market, and could also be a good design choice for stETH before withdrawals are enabled on the Beacon Chain, and could also be a great way to augment the AAVE treasury/insurance system if successful.

Insolvency risk is relatively mitigated, but not zero. For example, suppose one of the exchanges Ethena uses goes bankrupt. Sure, Ethena's collateral is safe with the custodian, but it suddenly loses its hedge and now has to hedge in potentially volatile markets. It's also possible that the custodian could go bankrupt, as @CryptoHayes pointed out when I spoke to him in Korea. No matter what kind of protections are around the custodian, there could be a serious hack or other problem, and crypto is still crypto, and there are still potential risks, even if those risks are extremely unlikely and might be covered by insurance, but they are still non-zero risks.

What are the risks of not using Ethena?

Now that we’ve discussed the risks of Ethena, what are the risks to protocols that don’t use Ethena? Let’s look at some stats. Half of Pendle’s TVL (at the time of writing) is attributed to Ethena. For Sky/Maker, 20% of revenue is attributed to Ethena in some way. About 30% of Morpho’s TVL comes from Ethena. Ethena is now one of the main drivers of AAVE’s revenue and new stablecoin. Those well-known platforms that are not using Ethena or interacting with its products in some way have essentially been left behind.

There are some interesting similarities between Ethena’s adoption and Lido’s adoption within the protocol. Around 2020 and 2021, the race for the largest lending protocol was much more intense. However, Compound was more focused on minimizing risk, perhaps to a ridiculous extreme. AAVE integrated stETH as early as March 2022. Compound had begun discussing the addition of stETH in 2021, but did not do so until a formal proposal was made in July 2024. This timing is exactly when AAVE began to surpass Compound. While Compound is still relatively large, with a total locked value of $2 billion, it is now just over a tenth the size of AAVE, which it once dominated.

To some extent, this can also be seen in the relative approaches of @MorphoLabs vs @AAVELabs to Ethena. Morpho began integrating Ethena in March 2024, while AAVE did not integrate sUSDe until November. There was an 8 month gap in between, during which Morpho grew significantly and AAVE lost relative control of the lending space. Since AAVE integrated Ethena, TVL has increased by $8 billion and product users have seen significant increases in returns. This has led to an "AAVETHENA" relationship where Ethena's products create higher returns, which incentivizes more deposits, which in turn leads to more lending demand, etc.

Ethena’s “risk-free” rate, or at least its “normal” rate, is about 10%. This is well over double the value of the FFR (risk-free rate), which is currently around 4.25%. The introduction of Ethena to AAVE, and especially sUSDe, functionally raises the equilibrium rate for borrowing, because now AAVE’s “base” rate inherits Ethena’s base rate, and even if it’s not exactly 1:1, it’s close. This has also been seen before, when AAVE introduced stETH, and the borrowing rate for ETH was roughly equivalent to the yield on stETH.

In short, protocols that don’t use Ethena may risk lower yields and lower demand, but the risk of a severe decoupling or collapse in the price of USDe is likely minimal. Some systems, like Morpho, may be better able to adapt and avoid potential collapses due to their independent structure. Therefore, it is understandable that systems based on larger pools of funds, such as AAVE, will take longer to adopt Ethena. Now, while most of this is retrospective, I want to make some more forward-looking points. Recently, Ethena has been struggling to integrate DEXs. Most DEXs lack short demand, that is, users who want to short contracts. Generally speaking, the only type of users who can do this consistently at scale are delta-neutral traders, of which Ethena is the largest. I believe that perpetual contract platforms that can successfully integrate Ethena while maintaining a good product can break away from competition in a very similar way to how Morpho broke away from its smaller competitors by working closely with Ethena.