Nearly 10,000 participants poured into the Hong Kong Convention and Exhibition Center. This was the first time that Consensus, the world's top Web3 industry summit, landed in Asia. Hong Kong was chosen not only because it is a test field for financial innovation, but also a hub for the flow of value between the East and the West. From "tokenized green bonds" to "Hong Kong dollar stablecoin regulatory sandbox", from "RWA ecology" to "decentralized AI", Hong Kong is using policy innovation as an engine to push the narrative of Web3 from technical experiments to deep integration with the real world.

OKG Research has been tracking the development of Web3 in Hong Kong since 2022, focusing on ecological and technological innovation practices. It has produced more than 30 in-depth articles on hot topics such as VASP, stablecoins, and RWA tokenization, and has established column cooperation with Hong Kong mainstream media such as Sing Tao Group and Ta Kung Wen Wei Media Group to continuously output industry insights. Taking the Consensus Conference as an opportunity, we once again focus on the core topics of Hong Kong Web3 and launch the " HK Web3 Frontline " special topic, analyzing the past, present and future of Hong Kong Web3 from a differentiated perspective.

1. Regulation first: orderly exploration of Web3 compliance boundaries

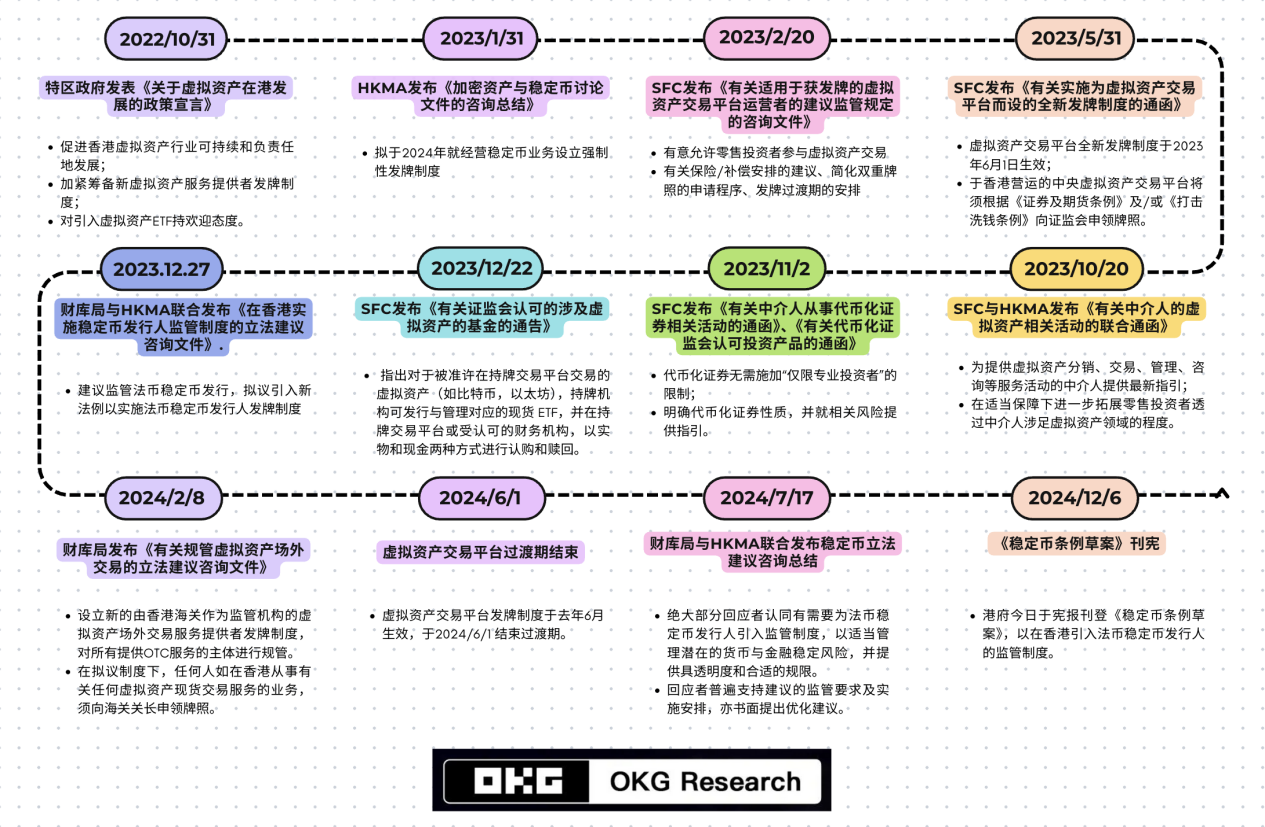

If the Hong Kong Web3 ecosystem is compared to a building, a reliable and adaptable regulatory framework is the foundation. Since the release of the policy declaration at the end of 2022, Hong Kong has continuously reviewed and improved its regulatory system to promote the autonomous evolution of the virtual asset ecosystem within the boundaries of security and compliance. By formulating a comprehensive regulatory framework covering virtual asset exchanges, stablecoin issuers, custodians and over-the-counter trading activities, Hong Kong has paved the way for value interoperability and long-term innovation in the financial market.

These measures not only enhance the credibility of Hong Kong's virtual asset market, but also continue to attract capital and corporate inflows. By the end of 2024, Hong Kong Cyberport alone has gathered nearly 300 Web3 companies, with a cumulative financing scale of over HK$400 million.

However, the global Web3 landscape has changed dramatically in the past two years. With Trump's return to the White House, the US crypto regulation situation has clearly improved. The high-pressure penalty regulatory model that has lasted for many years is disappearing, and regions such as Singapore and Dubai continue to send crypto-friendly signals. When "the rise of the East and the decline of the West" is no longer mentioned, and when the global Web3 competition becomes more and more fierce, how should Hong Kong seize this wave of innovation? OKG Research has proposed that the development of Web3 and virtual assets in Hong Kong should not only be theoretical, but also pragmatic: the Hong Kong government is concerned about technological innovation and application innovation that can have a substantial impact on the economy and society. Liang Fengyi, CEO of the Hong Kong Securities and Futures Commission, also expressed a similar view in her speech at the Consensus conference, " The second trend in shaping the future financial landscape is to integrate Web3 innovation into the real economy. "

At the same time, although the crypto asset market accounts for less than 1% of the global financial system, its rapid expansion and increasing correlation with mainstream financial assets have led to risks that cannot be ignored. Hong Kong and the United States have seemingly taken different paths at many points in time, but in fact they have reached the same goal: both are maintaining innovative activities while guarding against potential financial risks brought by this new category of assets.

2. Hong Kong dollar stablecoin: Hong Kong’s “financial” ambition

Stablecoins were a hot topic at the Consensus conference and a key area of focus for Hong Kong in the past two years. Standard Chartered Hong Kong, Ansett Group and Hong Kong Telecom were recently reported to be setting up a joint venture, hoping to apply for a license from the Hong Kong Monetary Authority under the new regulatory system to issue stablecoins pegged to the Hong Kong dollar. Circle, the issuer of USDC, also announced earlier that it would cooperate with the three major note-issuing banks in Hong Kong to launch HKDCoin, which is pegged 1:1 to the Hong Kong dollar.

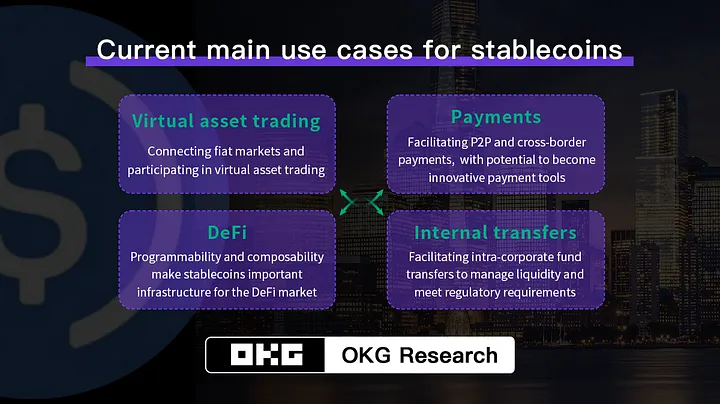

Although it is uncertain how much of the pie the Hong Kong dollar stablecoin will eventually get in the current environment where the US dollar stablecoin occupies an absolute market share, for Hong Kong, developing the Hong Kong dollar stablecoin is an inevitable choice to seize the initiative in the development of Web3 and seize the future financial opportunities . The connection channel with legal currency is the most worthy of development and the most likely to precipitate value in the current crypto ecosystem, and stablecoins are an indispensable infrastructure for building channels; at the same time, the focus of the next stage of Hong Kong Web3 development is to break the barriers between the virtual world and the real world, and stablecoins are the core link between traditional finance and the crypto world, and may become a widely accepted payment tool.

But how should the Hong Kong dollar stablecoin be issued? How should Hong Kong regulate it? Which institutions will be the first to "take the plunge"? " Seven Questions on the Hong Kong Dollar Stablecoin: Issuance Logic, Regulatory Rules and Potential Impacts " provides answers and believes that stablecoins backed by non-US dollar assets cannot compete with US dollar stablecoins in the short term. However, through mechanism innovation (such as interest-bearing stablecoins) and application innovation (such as RWA), the Hong Kong dollar stablecoin is expected to avoid direct competition with the US dollar stablecoin, thereby attracting more diverse institutions and users to participate.

Of course, we also need to distinguish between the Hong Kong dollar stablecoin and the digital Hong Kong dollar. Although there may be potential competition between the digital Hong Kong dollar and the Hong Kong dollar stablecoin in the short term, it is expected that resources will be shared and advantages will be complementary in the future: the utilization rate, scalability and friendliness of the Hong Kong dollar stablecoin in the virtual asset market will far exceed that of the digital Hong Kong dollar, while the digital Hong Kong dollar will be in a leading position in terms of value support and reliability.

3. RWA Tokenization: From Concept to 100 Billion Market

RWA is undoubtedly the hottest concept at this Consensus. “ RWA tokenization is not a trend, but a necessity. ” John Cahill, head of digital assets at Morgan Stanley, said at the “Institutional Investment Summit”, revealing the general strategic shift of traditional financial giants today.

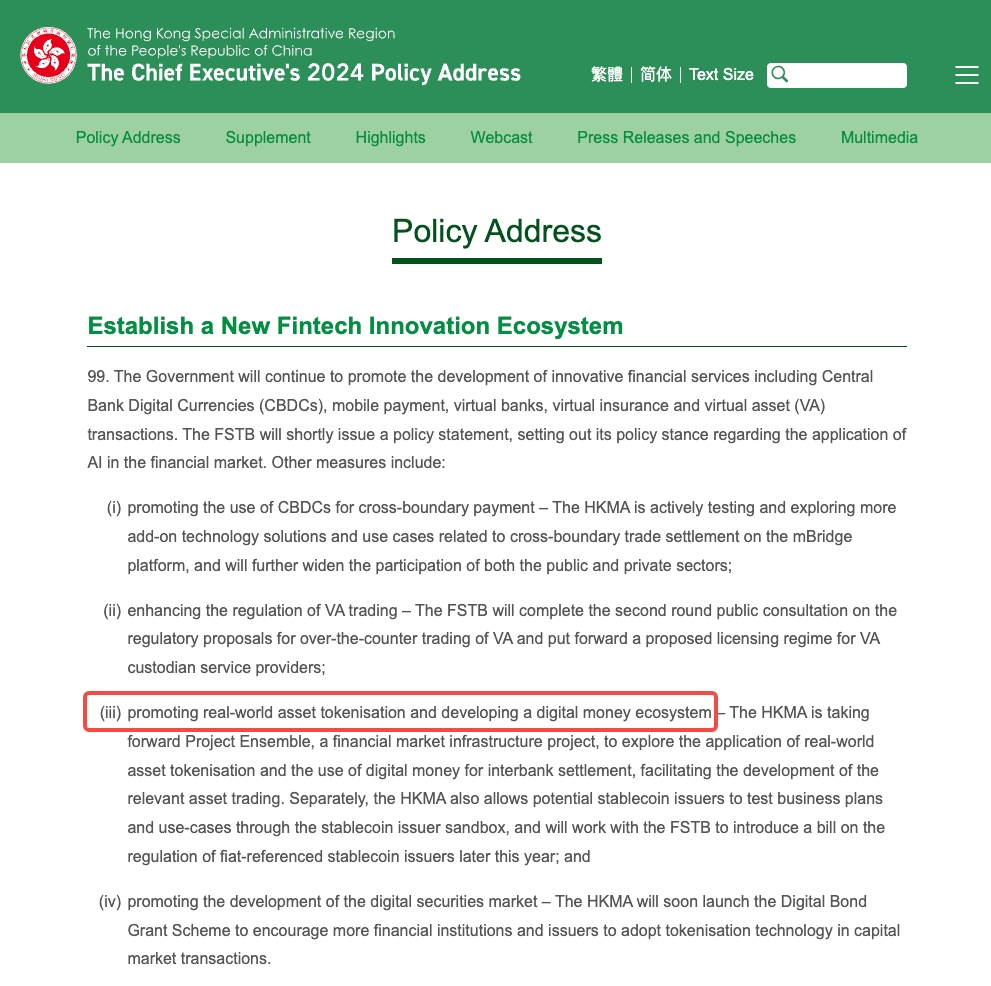

OKG Research proposed in 2023 that RWA is an important area worthy of long-term attention and investment in Hong Kong. How to tokenize the huge traditional assets is the biggest development opportunity for Hong Kong's virtual asset industry. Today, Hong Kong is actively embracing the wave of RWA tokenization. The 2024 Policy Address proposes to promote the tokenization of RWA and the construction of the digital currency ecosystem, and the Hong Kong Monetary Authority has launched the "Digital Bond Funding Program" to encourage the capital market to adopt tokenization technology. When attending the Consensus Conference, Xu Zhengyu, Secretary for Financial Services and the Treasury of the Hong Kong Special Administrative Region Government, also stated that Hong Kong is considering promoting gold tokenization.

However, the initiative of the tokenization narrative at this stage does not lie in Web3, but depends more on Web2 institutions, to see whether they have enough motivation to change the status quo and put the assets in their hands on the chain and tokenize them. This is not easy for traditional institutions: any new technology that attempts to migrate traditional assets/businesses to new areas is usually difficult to succeed quickly, because the incremental value it creates may not be large enough, but the cost is often high. The same is true for RWA. However, as Wall Street in the United States accelerates its layout of the tokenization market, Hong Kong urgently needs more institutions with resources and assets to actively participate in tokenization innovation in order to take more initiative in the transformation and avoid being quickly pulled away in the competition with the United States. How to stimulate market vitality is still an important proposition.

In addition, OKG Research also suggested in " How much time does Hong Kong have for RWA tokenization? " that Hong Kong should focus on standardized financial assets that are most suitable for tokenization in the short term, and give full play to Hong Kong's geographical and institutional advantages as an international financial, trade and shipping center, focusing on tokenized applications in trade and cross-border related scenarios, and rapidly expanding the scale of Hong Kong's RWA tokenization market.

IV. ETF and OTC: The “open and covert confrontation” of funding channels

Another key measure for the development of Web3 in Hong Kong in 2024 is the launch of virtual asset spot ETFs. From the clear acceptance of relevant applications at the end of 2023 to the official listing of six virtual asset spot ETFs approved by the Hong Kong Securities and Futures Commission on the Hong Kong Stock Exchange at the end of April, it took only a hundred days, which is enough to reflect the "speed" and "efficiency" of Hong Kong regulatory authorities. The launch of virtual asset spot ETFs has opened up another funding channel for investors to deploy crypto assets. As of the end of 2024, the total asset management scale of Hong Kong Bitcoin Spot ETF has exceeded HK$3 billion, accounting for 0.66% of the total volume of Hong Kong's ETF market.

Compared with the United States, the main advantages of Hong Kong's virtual asset spot ETFs are that they support physical subscriptions and are the first to launch Ethereum spot ETFs, but these have not brought sustained growth. Although the share of ETFs subscribed in physical form accounts for more than 50% of the initial issuance scale, Bitcoin holders are reluctant to release their liquidity easily due to macro expectations, while Ethereum spot ETFs affect investors' enthusiasm because they do not support staking. Although the current yield on Ethereum staking is only about 3%, both from a narrative and economic perspective, the additional income brought by staking is likely to be an important factor in attracting investors, especially traditional financial investors, and is also the main feature that distinguishes Bitcoin from Ethereum.

In addition to the ETF channel, Hong Kong has gradually formed a three-tier funding network of "licensed exchanges-compliant OTC-banks" . OKG Research stated in " How can the Hong Kong crypto market improve liquidity? " that the focus of liquidity at this stage is over-the-counter. Although trading platforms are still the most important infrastructure in the crypto market, observing the recent trends will find that crypto liquidity is gradually converging to the OTC (over-the-counter) market. At present, the Hong Kong OTC market handles nearly 10 billion US dollars in transactions each year. At the same time, thanks to the crypto money changers, a physical product with regional characteristics, it not only attracts young investors from all over the world, but also has an appeal to participants in the middle and older age groups. In recent years, the Hong Kong OTC market has also attracted the attention of many users and institutions in the fields of international trade and cross-border payments, becoming another important channel for Hong Kong to gather global funds.

The Hong Kong government is considering bringing OTC into the regulatory scope. Although it may have an impact on trading activity in the short term, it can help Hong Kong attract more compliant funds in the long run, and also help Hong Kong add another channel for the free flow of funds in addition to the licensed VATP. Perhaps in the near future, a safe and compliant OTC market will not only help the Hong Kong market improve liquidity, but also become an important channel for the crypto market and the Web3 ecosystem to connect to the real liquidity market.