By Gabe Parker, Galaxy

Compiled by: Wuzhu, Golden Finance

summary

Since 2021, the number of Bitcoin-based Layer 2 (L2) projects has increased more than sevenfold, from 10 to 75. More than 36% of all venture capital in Bitcoin L2 was allocated in 2024, and crypto venture capital firms have invested a total of $447 in Bitcoin L2 projects since 2018. Bitcoin L2 will use the funds raised to develop powerful applications and new use cases for BTC, aiming to attract a large amount of liquidity from native BTC holders and the existing wrapped BTC market. The report estimates that by 2030, more than $47 billion in BTC may be connected to Bitcoin L2. Our total addressable market (TAM) analysis of Bitcoin L2 takes into account the current market share of all BTC wrapped versions used in DeFi, as well as native BTC deposited in Bitcoin L2, and BTC locked in staking protocols. As of November 20, 2024, these portions account for 0.8% of all BTC in circulation. By 2030, we estimate that 2.3% of BTC circulating supply will be bridged into Bitcoin L2 to interact with the new Bitcoin DeFi ecosystem, fungible tokens, payment applications, and more.

Preface

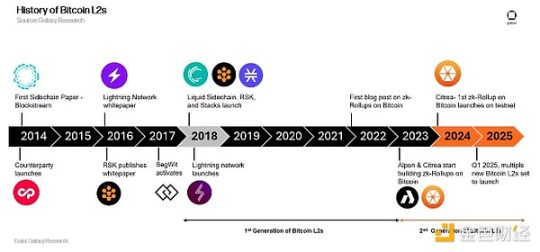

Since Bitcoin’s inception, discussions about Bitcoin’s future have included the concept of layered scaling. Hal Finney described the concept of “Bitcoin banks” in 2010, where “Bitcoin-backed banks…[could issue] their own digital cash currencies.” Tether launched on the Omni Network (one of the earliest Layer 2 networks) in 2014, a move described as “Bitcoin 2.0.” The debate over whether Bitcoin should scale the base layer rather than the high-performance L2 reached its peak during the “block size war,” a war that was largely resolved with the activation of SegWit on Bitcoin in August 2017 and the separate launch of Bitcoin Cash. SegWit enabled the payment-centric Lightning Network, which has been the most prominent L2 for many years. Two notable sidechains were launched in 2018—Blockstream’s Liquid (focused on asset issuance and payment confidentiality) and Rootstock (EVM-compatible sidechain).

The rise of Ordinals has brought tokenization activity back to Bitcoin’s base layer in 2023 and helped reignite interest in building applications on Bitcoin. This renewed interest, coupled with advances in Rollup development within the Ethereum development community, has sparked a new wave of Bitcoin Layer 2, primarily leveraging Rollup technology (optimistic and zero-knowledge). While the Lightning Network has had some success in enabling fast, cheap payments, developers have struggled to develop yield-generating applications for BTC on the blockchain itself. A large part of the difficulty is due to Bitcoin’s inability to support general-purpose smart contract applications. Bitcoin’s base layer is not Turing-complete, and therefore cannot execute the smart contract logic required by most DeFi applications. However, future upgrades may enable features that improve multi-party escrow, allowing for more powerful bridging and Layer 2 architectures. While a Bitcoin upgrade that achieves Turing-complete functionality has not yet been implemented and is unlikely to be implemented, some Bitcoin holders are already using their BTC to operate in DeFi or earn yield by bridging assets to other Turing-complete blockchains, rather than high-performance and trust-minimized Layer 2s — full blockchains like Ethereum. Wrapped Bitcoin (WBTC) on Ethereum accounts for the largest share (62%) of all wrapped versions of BTC. The wrapped versions of BTC used in Ethereum DeFi represent a large number of BTC holders seeking more efficient BTC use cases.

Over $9 billion worth of wrapped BTC (WBTC, tBTC, cbBTC) on Ethereum may indicate user demand for using BTC in DeFi applications. Holders of WBTC, tBTC, and other bridged BTC are more likely to transfer and use BTC on the new Bitcoin L2 than other groups because they are familiar with operating wrapped BTC assets on other chains. Bitcoin L2 may prioritize the development of attractive BTC-denominated yield-generating applications to attract existing wrapped BTC users on Ethereum to move funds to the new Bitcoin L2. Wrapped BTC holders may also use Bitcoin L2 because they have shown a tendency to value utility over decentralization. All Bitcoin L2s launched will be more centralized systems than Bitcoin L1, although some will have decentralized features comparable to the existing Ethereum L2.

Being able to use BTC in DeFi applications without exiting the Bitcoin ecosystem is a key selling point for Bitcoin L2. It will likely reduce friction in the user experience of bridging BTC and provide a safer alternative to using BTC in DeFi over existing solutions. A major benefit of Bitcoin DeFi on Bitcoin L2 is that BTC is both the native gas asset and the focal point of DeFi development. Historically, native assets have demonstrated greater utility on their native blockchains compared to external networks. For example, ETH’s large lending demand in Ethereum DeFi applications stems from its integral role as Ethereum’s native gas token and its widespread adoption as the primary unit of account for NFT and fungible token transactions. The evolution of the DeFi ecosystem on platforms like Ethereum and Solana illustrates an important principle: strong DeFi economies are built around blockchains’ native assets.

This report defines the key characteristics of Bitcoin L2 and provides a high-level overview of different types of Bitcoin scaling solutions. The report also provides a breakdown of the $447 million in cryptocurrency venture capital investment in Bitcoin L2 since 2018 and provides a TAM analysis of emerging Bitcoin L2s. Finally, the report shares key insights into the future prospects of Bitcoin modularity.

What is Bitcoin Layer 2?

Bitcoin L2 provides higher transaction throughput than Bitcoin L1 by enabling larger and faster blocks. Bitcoin L2 acts as its own execution environment and can therefore circumvent technical limitations present on Bitcoin L1, such as the lack of Turing completeness. By acting as an independent execution environment, Bitcoin L2 can use its own consensus mechanism, security framework, and virtual machine. For example, most Bitcoin L2s in production are EVM-equivalent or compatible, enabling them to integrate applications from other EVM blockchains. (For more information on EVM equivalence and compatibility, read Christine Kim's report on Ethereum ZK-Rollups).

Another key determinant of Bitcoin L2s is their bridging mechanism, i.e. how users transfer BTC from the base layer to L2. Bitcoin L2s use a wide range of bridging frameworks, including multi-signature and multi-party custody (MPC) wallet schemes and third-party bridges. Some Bitcoin L2s use multi-signature/MPC wallet schemes with BitVM, an off-chain Turing-complete virtual machine compatible with Bitcoin. At a high level, BitVM bridges involve a 1-of-n trust assumption, where only 1 honest bridge operator needs to be online for a user to exit the bridge. MPC and multi-signature bridges typically require more than 50% of signers to be honest in order for a user to exit the bridge.

The main difference between the Bitcoin L2 bridge and the Ethereum L2 bridge is that the latter involves smart contract accounts, while the former uses Bitcoin public key addresses. However, in both cases, smart contract accounts and Bitcoin public key addresses on Ethereum are usually controlled by a set of private keys. Another key difference is that Bitcoin L2 bridges for sidechains and Rollups do not have unilateral exits, meaning that users cannot exit the L2 without trusting the intermediary. Ethereum Rollups may include a feature called forced withdrawals, which enables anyone to submit their transaction directly to L1 to withdraw funds from the Rollup in the event that the sorter is offline or unable to include the user's transaction. State channels are the only Bitcoin L2 with trustless unilateral exits. Lightning Network bridges are built to allow users to seamlessly withdraw funds back to L1 as long as they have the latest balance status.

Bitcoin Rollup and Sidechains

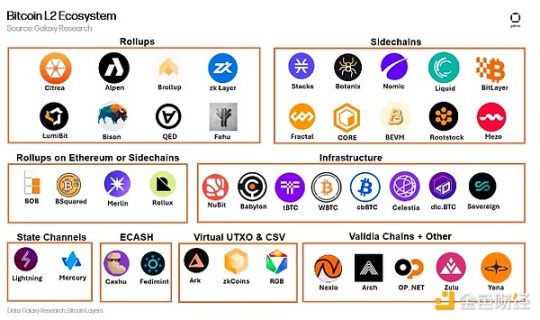

There are two categories of Bitcoin L2 solutions that can support general application development: Rollups and Sidechains. State channels are another L2 solution developed on Bitcoin, the most famous of which is the Lightning Network, but this technology is mainly used to enable faster and cheaper peer-to-peer transactions on Bitcoin and currently does not support Turing-complete smart contracts.

Sidechains: Sidechains are effectively independent blockchains that run in parallel with the base layer through an embedded connection with their own node operators and security mechanisms. Sidechains extend the base layer by creating independent compatible blockchains with larger blocks and faster block times. As a result, more transactions can be processed in a shorter period of time. Since sidechains use their own consensus model, they do not rely on the data availability layer, but instead act as closed and independent execution environments. Since sidechains use their own consensus model, some critics argue that they are not technically "layer 2" solutions, but rather act as separate extended layer 1. However, sidechains can be designed in a variety of ways, and it is important to distinguish between those that are consistent with the base layer and those that are not. Sidechains can publish hashes of block headers or other data to L1 as a way to "checkpoint" their own state to L1.

Rollup: Rollup is a blockchain that offloads transactions from the base layer and executes them on a secondary layer. As a result, Rollup provides users with 10x to 100x cheaper and faster transactions. By using a transaction data compression algorithm that batches multiple transactions together, Rollup can achieve higher transaction throughput than sidechains.

Rollup also uses a parent blockchain for data availability. The parent blockchain stores the state root, transaction data, or state differences of the Rollup. The data stored on the parent blockchain enables any full node to reconstruct the latest state of the Rollup. Rollup can be designed to support a single application or provide general functionality and host multiple applications.

Rollups update state roots in two ways. Validity Rollups (also known as zk-Rollups) create succinct cryptographic proofs that L1 verifies immediately upon receiving the update, proving that the update is consistent with the correct execution of those transactions. Optimistic Rollups push optimistically correct state root updates to L1 and provide a defined time window for validators to challenge the state root update.

The classification of the market map above follows these key characteristics:

- Bitcoin Rollup: An execution layer that publishes proofs and state difference data or transaction data into Bitcoin blocks.

- Rollups not on Bitcoin: An execution layer that publishes proofs and state difference data or transaction data on Ethereum or an alternative DA layer.

- Sidechain: An independent execution layer compatible with the Bitcoin base layer that does not require DA from the parent chain.

- Infrastructure: Data availability protocols and any wrapped BTC providers.

- State Channel: An off-chain execution environment with no global state, where only the initial and final states of account balances are committed.

- ECASH: A custodial state channel solution based on David Chaumian’s Ecash proposal.

- Virtual UTXO and CSV: A new iteration of state channels and execution layers using client validation.

- Valid chain: The execution layer is compatible with BTC and uses off-chain or alternative DA.

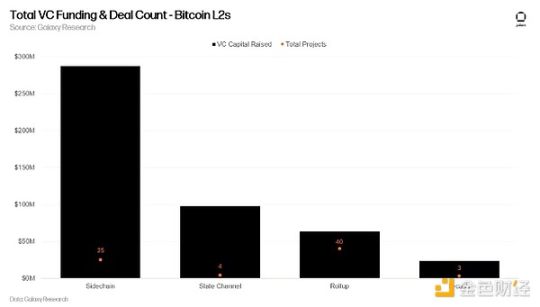

The market map does not include all projects in each category and is only for reference of different types of project construction in the Bitcoin L2 ecosystem. As of November 20, 2024, Bitcoin's L2 market consists of 40 Rollups and 25 Sidechains. This report does not cover state channels, CSV, Drivechain or ECash protocols, which represent a total of 10 projects.

Bitcoin L2 Venture Capital

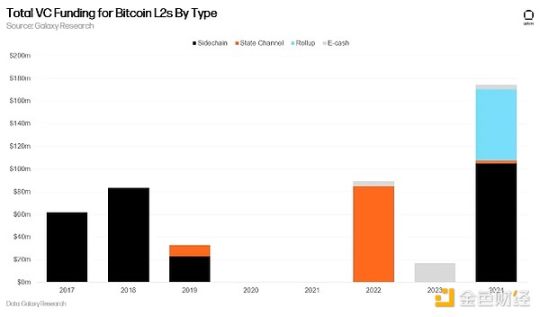

As of September 2024, Bitcoin L2 has raised $174M in funding from crypto VCs. Of this, sidechains received the largest allocation at $105M, followed by Rollups at $63M. Notably, 39% of all venture capital investment in Bitcoin L2 occurred historically in 2024 alone. A significant shift occurred in Q2 2024, with Bitcoin L2 capturing 44% of all crypto VC capital invested in L2 solutions across the industry, a staggering 159% quarter-over-quarter increase. The surge in crypto VC investment in Bitcoin L2 in 2024 highlights how traditional crypto VCs (excluding Bitcoin-focused funds) had little exposure to the Bitcoin ecosystem prior to the early stages of fundraising and development in 2024. As of November 2024, Bitcoin L2 has raised 2 Series A rounds across 30 disclosed deals.

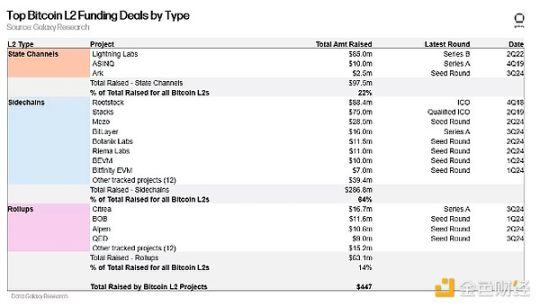

Bitcoin Layer 2 has attracted a lot of investment since 2018, with sidechains leading the way. Of the total $447 million invested in Bitcoin L2, sidechains accounted for the largest share, accounting for 64%. State Channels followed closely behind, accounting for 22%, and Rollups accounted for 14%. It is worth noting that ECASH-based protocols such as Cashu and Fedimint are not included in the above table and have received a total of $27.2 million in venture capital. The electronic cash project does not meet our definition of Bitcoin L2, but it is worth considering as a potential infrastructure in the Bitcoin L2 field.

Potential Market for Bitcoin L2

We consider the directly available market for Bitcoin L2 to be wrapped versions of BTC in DeFi contracts, native BTC bridged to L2, and the total supply of BTC staking protocols. The demographic of the “active” BTC supply is the focus of our TAM analysis. We believe this group of holders is most likely to link BTC to the new L2 to seek yield opportunities.

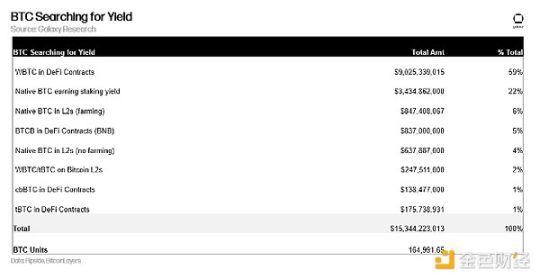

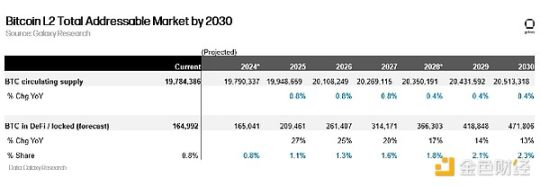

As of November 20, approximately 0.8% of BTC in circulation (164,992 BTC) is actively used. For the wrapped BTC market, $10 billion is locked in DeFi smart contracts and $247 million is locked on Bitcoin L2. For native Bitcoin, $3.4 billion is locked in staking protocols (Babylon, Bouncebit) and $1.5 billion is locked in Bitcoin L2.

If we assume that the share of circulating BTC supply using DeFi, L2, and Staking increases by 0.25% per year over 6 years, we estimate that by the end of 2030, “active BTC supply” could grow to 471,806 BTC (approximately a 3x increase).

In comparison, 2.3% of Ethereum’s circulating supply (ETH, WETH, stETH, wstETH) is locked in DeFi smart contracts (excluding staking protocols). At current prices as of November 20, 2024, the model projects Bitcoin L2’s TAM to reach $44 billion by 2030.

If Bitcoin reaches $100,000 in 2030, the TAM of Bitcoin L2 could reach $47 billion, assuming that 2.3% of the total Bitcoin supply is locked in Bitcoin L2 by 2030.

Note that this analysis provides a rough estimate of how much BTC supply could flow into Bitcoin L2 to earn yield; it does not take into account the potential growth of the Bitcoin L2 ecosystem, which includes other crypto assets that will be issued on top of these L2s, such as Runes, Ordinals, stablecoins, etc. Our TAM estimates rely on two key assumptions. First, we assume that the percentage of BTC supply locked in Bitcoin L2 could grow by 0.25% per year between now and 2030; second, we assume that the BTC price could reach $100,000 by 2030. Our view is that these are conservative estimates of Bitcoin L2 user demand and Bitcoin price over the next six years.

Also note that our forecasts depend on the progress of the DeFi and staking ecosystem on Bitcoin L2 while establishing legitimacy over the next 6 years. Crucially, if the yields on new Bitcoin L2 DeFi are not attractive enough, the BTC supply wrapped on Ethereum may remain in the Ethereum ecosystem. The following section will focus on the minimum yield level required for DeFi applications on Bitcoin L2 to compete with DeFi applications that accept BTC wrapped versions on Ethereum.

Taking Market Share from BTC DeFi on Ethereum

Although new versions of BTC wrappers are used in DeFi, this section focuses only on WBTC as this token accounts for 62% of the wrapped BTC market.

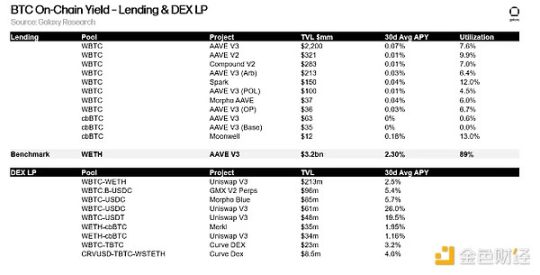

In order to capture significant market share from WBTC, lending protocols on Bitcoin L2 must 1) provide higher supply yields by increasing BTC utilization (users borrowing BTC), and 2) provide ample stablecoin liquidity for lending. About 72% of all WBTC locked in DeFi contracts are deposited in lending protocols. The large proportion of WBTC in lending protocols suggests that this group of BTC holders is only interested in lending applications. In addition, for every $100 of WBTC deposited on Ethereum's two major lending protocols Aave and MakerDAO, about $50 of stablecoins are borrowed.

By looking at the average utilization of these deposit pools, it is clear to see the large amount of stablecoin borrowing against WBTC on AAVE and Maker. On AAVE, the average utilization rate of WBTC is 7.7%, which means that 92.3% of deposited WBTC is used as collateral for stablecoin borrowing. As of November 2024, the average annual interest rate on WBTC deposits on AAVE is only 0.04%. For reference, the utilization rate of WETH on AAVE is 89%, and WETH deposits generate an annualized return of 2.3%.

ETH/WETH has a much higher utilization rate than WBTC. Use cases for WETH include DeFi, perp trading, staking, and NFTs. Lending applications on Bitcoin L2 aim to increase the utility of BTC by building a dedicated ecosystem for this asset, thereby providing higher yields. Some examples include Ordinal and alternative token protocols built on Bitcoin L2.

The table below highlights the yields for depositing wrapped BTC into lending protocols and DEX pools on Ethereum.

While depositing WBTC in a DEX pool offers higher yields compared to a lending pool, the risk of impermanent loss and yield volatility makes DEX pools an unreliable source of yield. As a result, 72% of WBTC’s DeFi contracts are allocated to lending protocols. In the case where BTC borrowing on Bitcoin L2 exceeds WBTC borrowing activity on Ethereum, lending protocols on Bitcoin L2 will offer higher yields due to increased utilization of the underlying asset.

Summarize

DeFi applications on Bitcoin L2 need to offer higher yields than Bitcoin DeFi on Ethereum to take market share from the wrapped BTC market. Bitcoin L2 can only succeed if it can take market share away from DeFi applications that accept tokenized versions of BTC like WBTC, tBTC, and cbBTC. A vibrant DeFi ecosystem on Bitcoin L2 is the most important development for long-term L2 adoption. This is evident when looking at the top applications by TVL on Ethereum L2 (Arbitrum, Optimism, and Base), which include lending, DEX, and derivatives platforms.

The trust assumptions of the new Bitcoin L2 bridge design are no weaker than those of the WBTC, cBTC, and tBTC bridge designs. WBTC holders need to trust BitGo's federation, a centralized entity, while BTC holders on Bitcoin L2 need to trust a relatively more decentralized set of bridge operators. Although there is no unilateral exit on any Bitcoin Rollup or sidechain, once this feature is developed, the bridge on the new Bitcoin L2 will be less trustworthy than WBTC, cBTC, and tBTC.

In 2024, Bitcoin L2 received $174 million in venture capital, providing these projects with a platform to execute market strategies. Bitcoin L2, which has raised a large amount of funds, will establish an ecosystem fund and use the funds to install existing EVM applications. Continued investment in the Bitcoin L2 ecosystem will play a vital role in the growth of the industry in the next 6 years. Once Bitcoin L2 is put into production on the mainnet, cryptocurrency venture capital firms may turn to investing in early native applications.

The emergence of Ordinals and BRC-20 in 2023 signals to cryptocurrency VCs that there may be another way to invest in Bitcoin besides digital gold. As Bitcoin L2 matures and its user base expands, cryptocurrency VCs will continue to deploy capital into the Bitcoin ecosystem.

Of the 75 Bitcoin L2s today, only 3-5 players are likely to end up with the lion’s share of the market. There won’t be enough users, liquidity, and attention to allocate to 75 Bitcoin L2s. We highlighted this view of Bitcoin Rollups using Bitcoin for DA in a previous report. The L2s with the most liquidity and yield-generating applications may be the only ones that survive in the next 6 years. Therefore, business development partnerships in infrastructure, liquidity bootstrapping, and market making will be critical to determining which Bitcoin L2s will lead the others.