By Hedy Bi, OKG Research

The United States, which has returned to the survival of the fittest, will fire the first shot in the trade war tomorrow morning (April 2, Eastern Time), and it is clear that it will put "America First" above multilateralism. The global economy is hanging on the front line. The market has already partially cashed in. Gold has risen by 18% since the beginning of the year, setting new highs. However, there are still opportunities under the crisis. We seem to be able to smell a hint of opportunity from the Trump family's latest crypto business layout. Although the mining cost remains high and the profit margin is slim, from the recent stablecoin to the entry of mining machines, the crypto industry seems to be accelerating both "Made in the USA" and "Made in Trump". In the words of Donald Trump Jr., "there is no limit to the future."

This article is the seventh article in OKG Research's 2025 special plan "Trump Economics". It seeks vitality from the crisis and deeply analyzes the impact of tariffs on the entire industrial chain of the crypto industry.

Tariffs, known as "customs and market taxes" since ancient times, are imposed on transit goods to manage the Silk Road trade. Tariffs, as a macroeconomic tool, directly affect the market price and circulation efficiency of commodities. In other words, for the crypto industry, it is not only necessary to pay attention to the prices of commodities and technologies directly related to the chain, but also to its more far-reaching impact on the overall efficiency of the industry, the liquidity of the supply chain, and the reshaping of the market structure.

Tariffs will directly increase Bitcoin mining costs by 17%

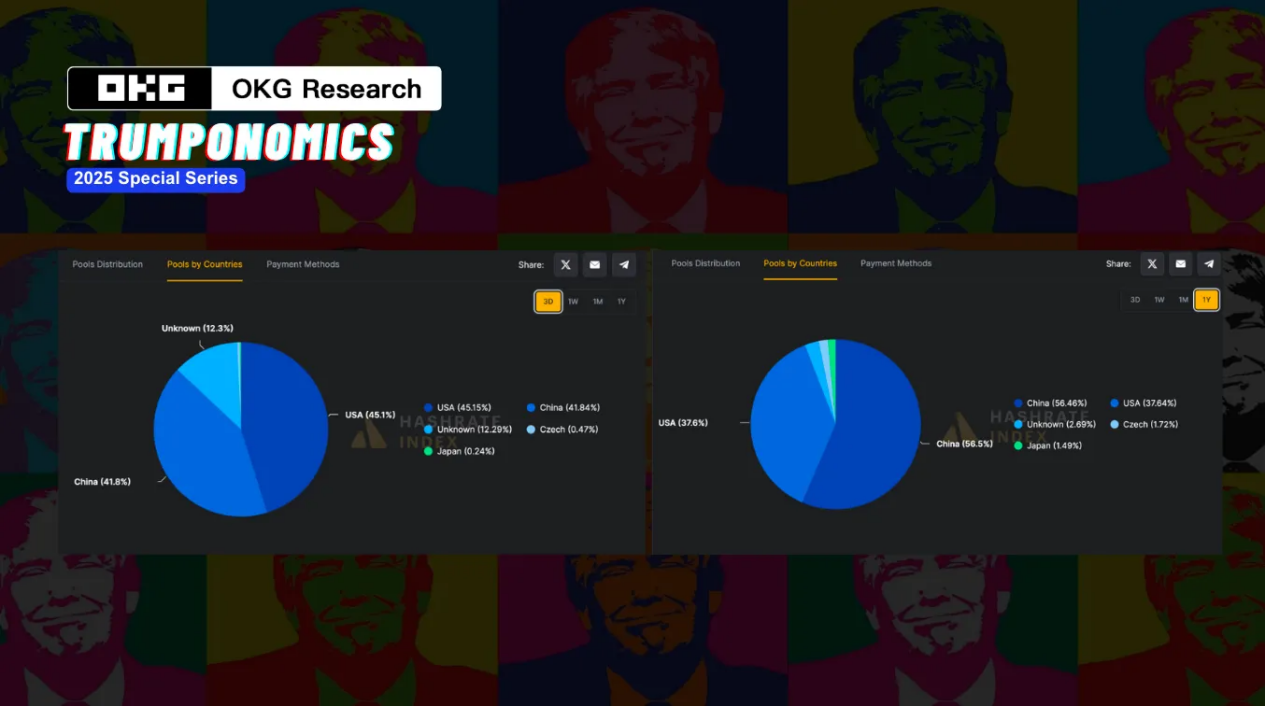

In the cryptocurrency industry, Bitcoin has always been the most representative digital asset, dominating the market landscape. According to CoinMarketCap data (April 2, 2025), the market value of Bitcoin accounts for 59% of the entire crypto market, far exceeding other digital assets. Bitcoin relies on the Proof of Work (PoW) consensus mechanism, which makes the price and supply chain of mining machines a key factor in the market trend. However, although the computing power share of US mining pools has increased from 37.64% to 45.15%, the mining machine supply chain is still dominated by Chinese manufacturers, especially Bitmain, MicroBT and Canaan Technology, which account for more than 70% of the global mining machine market share. Therefore, the Trump administration's goal of "bringing Bitcoin mining back to the United States" faces huge challenges.

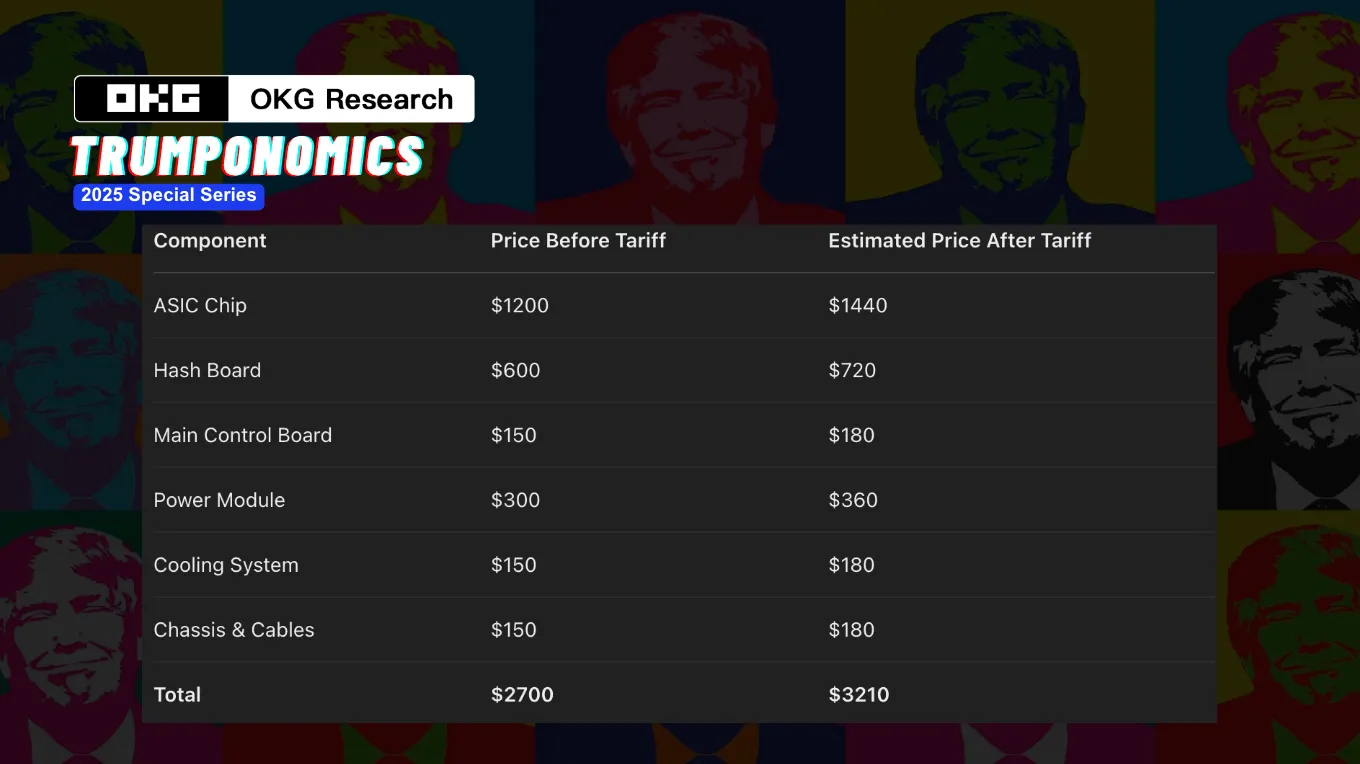

The tariffs imposed by the United States on Chinese electronic products have exacerbated this mismatch between supply and demand. It is expected that if a 20% tariff is imposed on Chinese electronics, the cost of mining machines will increase by about 17%, which will directly affect the return on investment (ROI) of mining farms. This change is particularly critical for new mining farm operators, who may need to re-evaluate their profit models. In addition, although MicroBT and Bitmain have announced the establishment of manufacturing centers in the United States and Malaysia to promote the de-Chinaization of mining machine production, this shift has also brought about delivery delays. Customers may have to wait 1 to 3 months to receive the equipment, which poses a considerable challenge to mining farm operations that rely on timely delivery.

The global semiconductor shortage and the US's technology export restrictions on China have forced mining machine manufacturers to establish production bases in multiple countries to reduce risks. This change has led to an unstable supply of mining machines, and supply bottlenecks may occur in the short term, which will in turn affect the expansion and operational capabilities of mining farms. With the increase in mining machine prices and the increase in delivery delays, the mining industry may gradually move towards centralization. Large mining companies will occupy more market share with their financial advantages, while small mining farms may face greater survival pressure, and the extension of the investment payback period will prompt them to exit the market.

Overall, tariff policies and supply chain fluctuations are profoundly affecting the Bitcoin mining industry. Rising costs, delivery delays, and unstable supply chains have prolonged the payback period for mining farms and accelerated the concentration of the industry. Large mining companies are likely to dominate the market, while small mining farms will face more severe challenges to survive. In addition to Bitcoin, other blockchain projects that rely on imported electronic hardware from non-US regions (such as AI) will also face similar cost pressures.

Off-chain blocking and on-chain opening

The US tariff policy not only directly affects the cost of goods, but also has a more far-reaching impact on the reshaping of the global financial order. In recent years, the rapid rise of US dollar stablecoins has become part of the US financial strategy - building barriers off-chain and accelerating openness on-chain.

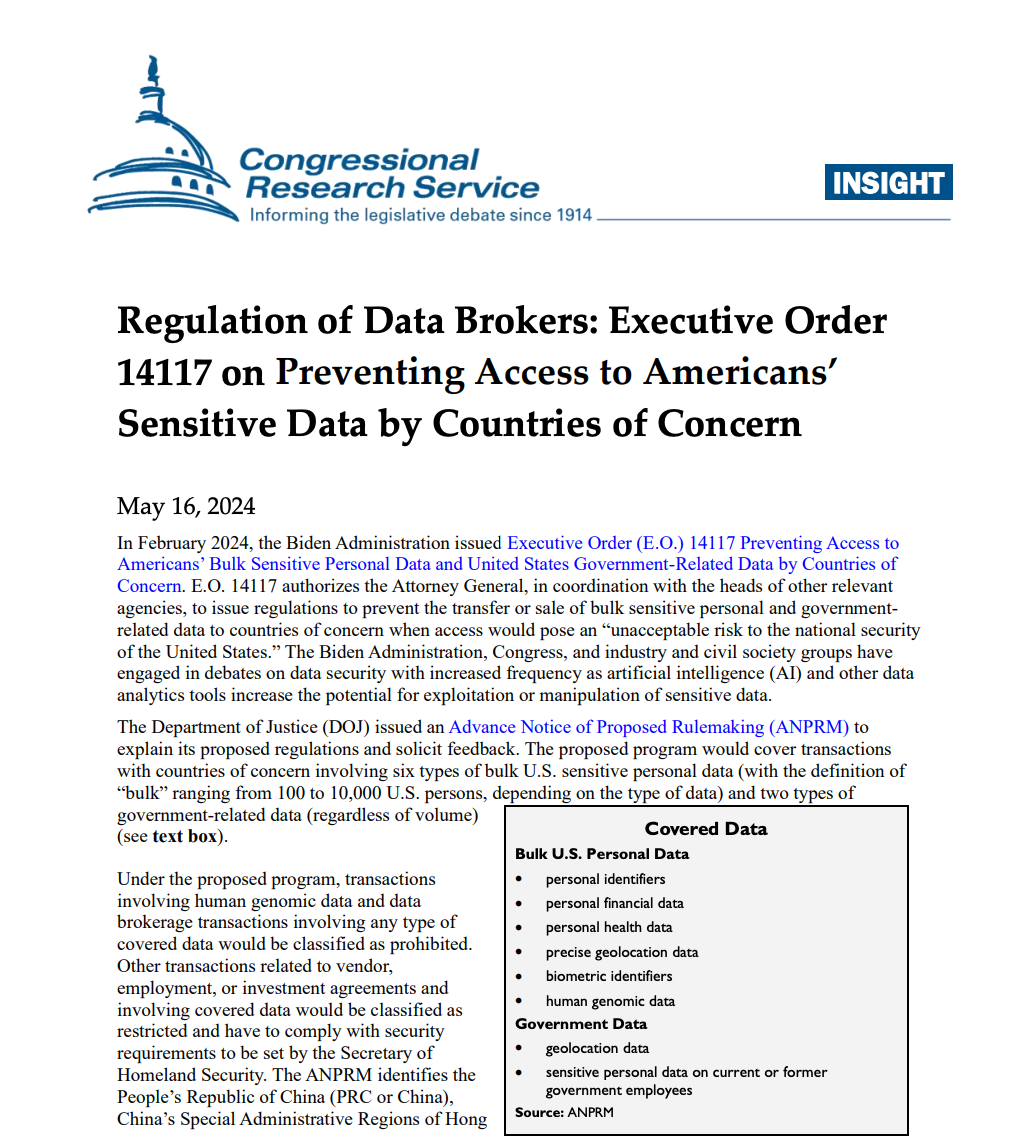

For a long time, the settlement system of global trade has relied on the banking network, and clearing systems such as SWIFT and CHIPS dominate international capital flows. However, as geopolitical conflicts intensify, the United States has not only imposed tariffs, but also deeply reshaped global trade through measures such as data decoupling and financial supervision. The most typical example is Executive Order No. 14117 (hereinafter referred to as "Executive Order 14117") signed by US President Biden in 24 years, which aims to restrict "countries of concern" from obtaining US data. "Executive Order 14117" will officially take effect on April 8, and companies such as Paypal will also need to adjust their companies in mainland China. The policy is ostensibly aimed at the cloud computing and chip industries, but in fact it also cuts off the supply chain data sharing of multinational companies, which has a chain reaction on trade financing and payment settlement.

In this context, the US dollar stablecoin has become a new channel for global capital flows. This means that when the traditional banking network is subject to regulatory restrictions, the stablecoin network can still provide US dollar liquidity to the global market. For example, financial companies in Argentina, exporters in Southeast Asia, and even some Middle Eastern traders have begun to bypass the banking system and use USDC or USDT directly for supply chain payments. The low cost and instant settlement characteristics of stablecoins make them an ideal tool for cross-border trade. Traditional bank transfers may take 2-5 days and are expensive (the average SWIFT transfer fee is $20-40). Taking USDC as an example, the transfer fee through stablecoins is usually less than 1 cent and can be completed in seconds.

More symbolically, in countries with strict capital controls such as Argentina and Nigeria, the demand for stablecoins is becoming more urgent. In 2024, Argentina will have to pay a 30% premium when purchasing stablecoins, and Nigeria will pay 22%. Behind these premiums, it is precisely because of the closure of traditional financial channels and the depreciation of the national currency that stablecoins have become a key tool for residents and businesses to bypass the banking network and protect their wealth.

Post-tariff landscape: Liquidity expansion outside the Fed

After the tariffs, the market demand for US dollar stablecoins will increase. To be more precise, a "shadow dollar market" that bypasses the Federal Reserve's supervision is rapidly expanding around the world.

In addition to the "de-banking" of their circulation paths, in terms of issuance, the issuance of US dollar stablecoins such as USDT and USDC relies on US Treasury bonds as collateral. This model is still indirectly affected by the Fed's policies on the surface - after all, the yield of US Treasury bonds determines the cost of stablecoin issuance. But the liquidity creation mechanism of stablecoins is not directly controlled by the Fed. When the market demand for the US dollar is high, stablecoin issuers can quickly increase issuance without the approval of the Fed. This means that even if the Fed hopes to tighten liquidity through tightening policies, the stablecoin market can still "release water in disguise" and continue to expand the supply of US dollars worldwide.

In the past, the Federal Reserve could adjust the supply rate of US dollars through the banking system, but now, these "on-chain dollars" are completely outside the banking network, and the Federal Reserve's traditional regulatory measures are almost ineffective in the stablecoin market.

The liquidity of stablecoins is mainly concentrated within the crypto market. DeFi platforms, centralized exchanges (CEX), and on-chain payment systems form an "internal circulation" of stablecoins. A large amount of capital has not flowed back to the financial system regulated by the Federal Reserve, but has remained in this emerging on-chain dollar economy. What's more, the dollar deposit interest rates offered by many DeFi platforms are much higher than those of traditional banks, which further weakens the Fed's interest rate transmission mechanism. Even if the Fed adjusts the benchmark interest rate, the flow of funds in the stablecoin market still operates according to its own logic, becoming a relatively independent dollar financial system.

The demand from the stablecoin market has also pushed up the market demand for U.S. Treasuries and depressed the yield of U.S. Treasuries. It is worth noting that with the introduction of RWA, the liquidity of stablecoins has also begun to enter a wider asset pool, further exacerbating this trend. This means that the interaction between the stablecoin market and the U.S. Treasury market will become more complex and may even affect the pricing logic of funds in the global capital market in the future.

The announcement of tariffs, known as "Liberation Day", will bring more or less restrictions in terms of cost and circulation, but the United States is quietly reshaping the global financial architecture by strengthening off-chain blockades and expanding on-chain dollar liquidity. From the decoupling of supply chain data, to the restrictions on bank clearing, to the rapid rise of stablecoins, we seem to be witnessing a financial revolution.

Remember the original intention of Bitcoin written in the white paper? A completely peer-to-peer electronic currency should allow online payments to be sent directly from one party to another without going through a financial institution. Perhaps, we are already standing on the threshold of this vision.