Original author: Elliot Hershberg

Compiled by: LlamaC

Main Text👇

Ten years ago, Scientologist (not scientist) Bob Dugan sold the US biotech startup he founded to AbbVie for $21 billion (yes, not millions). His company, Pharmacyclics, had developed a promising cancer drug, and the payoff was huge. In fact, Dugan’s gain of more than $3.5 billion was reportedly one of the largest returns on a public buyout in history.

Aside from the eccentricity of founder Dugan — and the involvement of several other big names that made the whole thing historic — it was a relatively ordinary deal. A large pharmaceutical company was under great pressure to find new sources of revenue as the patent exclusivity period of one of its blockbuster products was about to end. A breakthrough drug from an American startup just happened to fill that gap.

A large part of the biotech industry is built on this dynamic. Small startups have become the main source of innovation, conducting the majority of early clinical trials each year. Large pharmaceutical companies acquire these startups at a generous premium to continuously replenish their product pipelines.

But things are changing. Ten years later, Dugan is back. This time, he brought a new drug that beat Merck's $30 billion-a-year cancer immunotherapy drug Keytruda in clinical trials. The key is that Dugan did not discover this drug in an American laboratory, but obtained a license from a Chinese company.

Unlike Pharmacyclics, this story did not end with a multi-billion dollar acquisition. Instead, Merck turned to the same source and bought its own version of the same drug from another Chinese company for $500 million.

This is significant. As we’ve seen recently in artificial intelligence, China has become a formidable competitive threat in biotech, demonstrating its ability to rapidly develop new drugs that rival — or even surpass — what’s coming out of U.S. labs. In other words, “pharma is having its ‘deepseek moment.’ ”

Here’s another example. With the explosive success of GLP-1 drugs, pharmaceutical companies are racing to acquire their own next-generation products to compete with Novo Nordisk and Eli Lilly for market share. Merck has once again set its sights on China, acquiring an oral GLP-1 drug for an upfront payment of $112 million. The deal also includes subsequent milestone payments based on commercial success, totaling $1.9 billion.

For context, US biopharmaceutical company Viking Therapeutics has an oral GLP-1/GIP agonist in its pipeline and is currently valued at $3.8 billion. Rather than fully acquiring Viking, why not acquire a molecule from China at a low price and see if it works?

At a time when the biotech market is sluggish, increased external competition is making things even more difficult. While the M&A market has slowed, now founders and investors are losing sleep over deals scuttled at the last minute by secretive Chinese competitors they’ve never heard of.

The whole situation has generated a lot of analysis. My favorites so far have been David Li, a Chinese-American biotech startup founder, and his follow-up analysis in the Timmerman Report, Bloomberg, and Alex Telford’s thoughtful take on the question, “Will all our drugs come from China?”

Here, I want to take a step back and think about how we got to this point.

In 1987, Merck was featured on the cover of Fortune magazine for "betting on the magic molecule" and was named "America's Most Respected Company."

In the decades before that, Merck scientists were responsible for developing breakthrough molecules for high blood pressure, some of the most successful vaccines in history (one of the most prolific vaccinologists of all time, Maurice Hilleman, was a Merck scientist), the first statins, and entirely new classes of antibiotics.

For two of its hottest products on the market today, Merck isn’t relying on the U.S. biotech startup ecosystem (which was still in its infancy in 1987) but instead is sourcing molecules from the Chinese ecosystem—which until recently was not a significant source of innovation.

Clearly, the global drug discovery industry has undergone a significant evolution. At this juncture, I think it is worth reflecting on the long journey of drug discovery technology commercialization and the implications of this historical pattern for the industry’s future.

The long journey of commercializing drug development technology

Let's think about biologics for a moment.

Throughout history, the vast majority of drugs have been discovered by chance as plant chemicals that have a positive effect on human physiology. Over time, tools have been developed to more systematically screen chemical space for useful small molecules. Another small group is proteins such as insulin that can be isolated from animals and used to treat diseases.

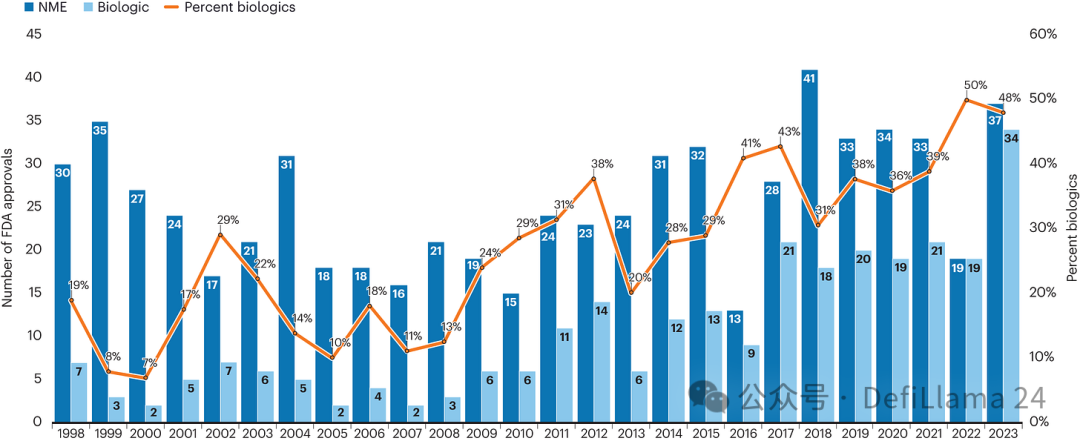

Genentech was founded in 1976 on the revolutionary breakthrough of recombinant DNA technology, a revolution that sowed the seeds of radical change. The tools of genetic engineering enabled entirely new ways to produce bioderived molecules to alleviate disease. Fifty years later, the number of biologics approved each year has almost equaled that of small molecule drugs.

Growth of Biologics Over Time

Growth of Biologics Over Time

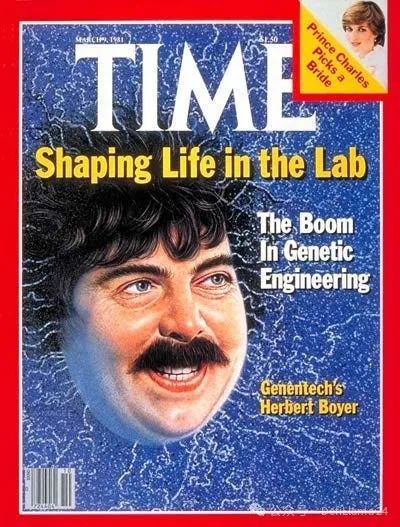

But initially, few people believed this new class of medicines was possible. And just as few people around the world had the necessary skills to try it. It’s easy to overlook the fact that Genentech began as a fringe project, with scientists working day and night in uniform, wearing T-shirts, jeans, and running shoes.

As Peter Thiel has said, the company holds an important shared secret that the outside world has not yet understood.

Success changed all that. When Genentech achieved its first product breakthrough, the market responded with wild optimism. Nothing—not even Princess Diana—was more exciting than the idea of transforming life.

When Genentech went public in 1980, the initial share price was $35. Within one hour of trading, the share price soared to $88, almost tripling. The scene at the time was simply frenzy.

By 1983, US companies had invested $500 million in emerging biotechnology companies. Two years later, the US Department of Commerce estimated that some 200 biotechnology companies had attracted nearly $2 billion in investments.

Looking back, it was clearly a hype bubble. Recombinant DNA technology was still in its infancy. Major breakthroughs like recombinant insulin did not follow quickly. Regulatory issues were still unresolved. Manufacturing biologics at scale was also a challenge.

The initial boom was followed by a period of disillusionment and contraction. In 1985, a Massachusetts journalist wrote:

If all this seems too far-fetched for scientists with little or no commercial track record, you're right. To that point alone, two trends have taken hold in the post-boom biotech industry.

First, in a few of the better-capitalized companies, the scientist/founder/CEOs are hiring, or being forced to hire, traditional “numbers experts” as company presidents or COOs. These are experienced business executives from large companies, not academics. Cambridge-based BioTechnica International just hired a 20-year DuPont veteran. At Collaborative Research in nearby Lexington, the new president once led a Johnson & Johnson subsidiary. So is the new president of Damon Biotech in Needham Heights.

Second, industry momentum seems to have shifted in favor of large companies. In particular, those companies that provided much of the seed funding for biotech startups through equity purchases and R&D contracts. In a sense, the good response to new biotech IPOs has simply delayed bad news for many companies. Now, when these young companies are in desperate need of a new round of capital injection, companies such as DuPont, Grace, Monsanto and Eli Lilly are shifting investment to internal biotech capabilities. As a result, industry experts predict a wave of mergers and acquisitions. EF Hutton analyst Nelson Schneider believes that as many as two-thirds of biotech companies will either merge or be acquired by large pharmaceutical or chemical manufacturers.

In other words, the industry was forced to mature and realize real revenues, and existing organizations woke up and began to build their own biotech capabilities in-house. By the end of the 1980s, most biotech stocks had lost three-quarters of their value.

But at the heart of this bubble lies an important kernel of truth: recombinant DNA technology is indeed a revolutionary tool for making new medicines. Even in a calmer environment, companies that have the resources, technology, talent, and perseverance to survive continue to launch new products.

After synthesizing insulin, Genentech produced seven more biologics throughout the 1980s and 1990s. Amgen was another early biologics pioneer founded in 1980, and they stood out from the competition with a series of breakthrough drugs. Regeneron was founded in 1988, and after an initial boom, they gradually established their own characteristics through in-depth research on the human genome and a powerful monoclonal antibody production technology platform - monoclonal antibodies proved to be one of the most important types of biologics.

Despite many skeptics, biologics continue to expand across medicine, with approvals expected to equal those of small molecules for the first time in 2022. (The chart we saw earlier.)

The commercial success of these pioneers is equally undeniable. Genentech was acquired by Roche for $46.8 billion in 2009 and still operates as a highly influential independent subsidiary. Amgen currently has a market value of $168 billion. Regeneron is now valued at $78 billion, with its stock price up nearly 4,000% from its IPO.

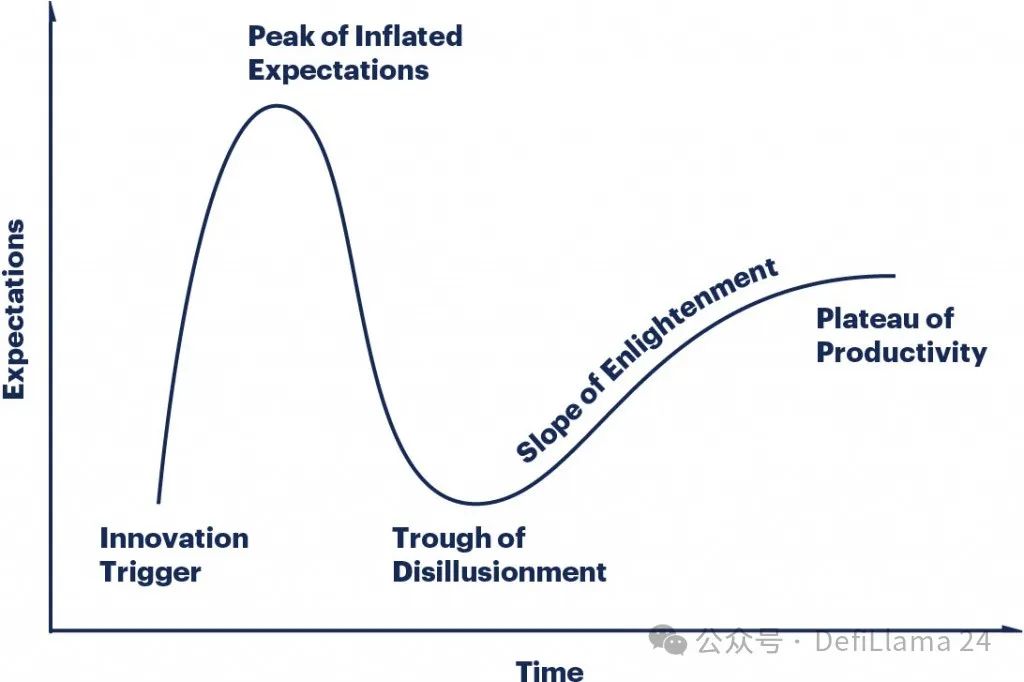

This evolution is almost a textbook example of the Gartner Hype Cycle. An initial "innovation trigger" generates a huge wave of hype and excitement. When the hype fails to materialize immediately, the market cools down. If there is substance to the initial trigger, a more gradual recovery will occur over time.

We do seem to have entered a “plateau of productivity.” The ability to produce biologics is no longer a closely guarded secret among a few companies. Scientists around the world have spent decades perfecting the tools to develop these drugs. A host of companies have sprung up to offer antibody development services.

Take Adimab as an example. Founded in 2007, the company uses a new generation of antibody engineering technology - yeast surface display technology - to quickly produce new molecules for many partners. Currently, they have cooperated with more than a hundred different partners, and "there are more than 75 clinical projects derived from our platform."

Source: Adimab

Given that Adimab is a private company, it is difficult to directly compare its commercial success with that of pioneers such as Amgen or Regeneron. But based on its valuation of $1.1 billion in a secondary transaction a decade ago, it has roughly grown into a business worth about $5 billion to $10 billion.

Today, if companies want to use different technologies or have specific preferences based on cost, speed, location, or even a variety of other factors, they can choose to work with FairJourney Biologics (valued at ~$900 million in 2024), OmniAb (market cap ~$400 million), Ablexis, Specifica, Creative Biolabs, Twist Biosciences, Alloy Therapeutics, or others. This list is only a sample and is far from exhaustive.

It is worth noting that the size of each generation of companies has decreased by about an order of magnitude. The first movers grew to approximately $100 billion+ companies, the leading service providers that emerged later became approximately $10 billion+ companies, and today the new entrants that are finding the market are approximately $1 billion+ companies.

To me, this reads like the textbook definition of commoditization, the process of gradually transforming a good or service into a commodity that is interchangeable with other similar goods and making them competitive on price.

Think about electronics. Initially, only a few companies made the best TVs, and they charged a high premium. Over time, competition eroded that premium. Today, a multitude of companies sell large flat-panel screens with smart features at Costco for hundreds of dollars. That's commoditization.

Likewise, differences between antibody discovery service providers are becoming increasingly indistinguishable, with many companies using similar technologies to produce antibodies against the same drug targets.

So far, we’ve focused only on the history of antibodies. But I want you to join me in making a bold assumption that may annoy some drug developers: no discovery technology is immune to the inevitable trend toward commoditization—just like almost every other technology.

For both large and small molecules, once discovery technologies—whether high-throughput screening, in silico screening, in vitro or in vivo models, or analytical assays—become standardized, companies around the world will compete to offer them as a service.

This is the long journey of modal commoditization.

Over time, revolutionary ideas become the universal building blocks for the next wave of innovation.

The strategic evolution of biotechnology

As discovery techniques have standardized and commoditized, biotech investing has also professionalized. After decades of refinement, the industry has converged on standardized company valuation models, and new strategies have emerged.

One strategy that has gained widespread acceptance is the “fast follower” approach, which is to develop a new drug to be “best in class” at a target targeted by existing drugs rather than to be “first in class” at an entirely new drug target.

An analysis published in 2003 identified two key advantages of “pursuing the best.” First, such drugs clearly have a lower risk profile because their targets have already been validated through drug approval based on human evidence. Investors often discuss the degree of “biological risk” they are taking on for new target hypotheses. Second, the risk differential does not seem to be rewarded commensurately. In fact, looking at drugs launched between 1991 and 2000, most blockbuster drugs were developed for known targets, and fast followers created more value than riskier innovative drugs.

Pursuit of the best

Merck’s acquisition of an oral GLP-1 agonist that we previously studied is a clear example of this strategy. Novo Nordisk and Eli Lilly took huge risks in validating the efficacy of the first GLP-1 drugs. Now, other companies are racing to develop fast-follow products with improved properties, such as being given as a pill instead of an injection.

Many biotech investors have taken this analysis to its logical extreme. As the size of early-stage financing rounds and the funds behind them have swelled, it has become increasingly difficult to justify betting large amounts of capital on completely unproven target hypotheses. In practice, this has led to a serious clustering of proven target areas.

Clustering in the drug development pipeline

To make things more efficient, the 2010s saw the rise of “virtual biotechs” that outsource all R&D to discovery partners like Adimab. The goal is often to quickly develop the best molecule against a known target and then sell it to a large pharmaceutical company for late-stage development and commercialization.

This industry history is critical to understanding the recent surge in Chinese licensing agreements, as many of the top outsourcing partners are Chinese contract research organizations (CROs).

WuXi Biologics, a Chinese giant that provides a full range of biologics discovery and manufacturing services, has become the world's second largest outsourcing partner, accounting for more than 10% of the global market share.

Today, China’s strategic evolution, reflected in its new 2015 policy, is a very logical shift from being a mere service provider to developing its own drugs. In a world where most people use standardized discovery technologies to target the same drug targets, China has two key advantages:

Speed. A new series of reforms will allow clinical trials to be initiated more quickly.

Trends in China’s Innovative Drug Development (Thanks again to Alex Telford for his wonderful blog post that brought this data to my attention!)

Cost. Chinese scientists earn a fraction of what their American counterparts do. An army of highly skilled — often American-trained — researchers can work on more problems.

With these advantages, Chinese startups and biopharmaceutical companies seem to have covered the field of known drug targets. Companies have cheap "call options" on a wide range of targets in the form of preclinical or early-stage assets. When a particular target or product concept is favored by a large pharmaceutical company, these "options" can be exercised by increasing investment to accelerate the progress of existing projects.

This puts enormous pressure on the fast-following strategy. While American scientists sleep at night, machines are still humming in rival labs on the other side of the world.

So far, we have traced the history of the commoditization of drug discovery technologies and the subsequent professionalization of biotech investment. These changes help provide context for the industry’s “DeepSeek moment.”

Now, let’s think about where value might accumulate in the future.

AI may be the last wave of commoditization

Over the past few years, a lot of money has poured into companies with ambitious plans to use artificial intelligence to transform drug discovery. Companies like Xaira Therapeutics, which started with $1 billion in “seed” funding, aim to develop drugs on their own. But many companies, such as EvolutionaryScale, Profluent, Chai Discovery, and Latent Labs, prefer to take a strategy similar to Adimab, offering this new technology as a broadly enabled infrastructure.

When Latent Labs was founded, Tony Kulesa of Pillar wrote:

From this came a clear vision: to democratize the use of advanced AI tools in drug discovery. While every biotech and pharmaceutical company searching for therapeutic molecules understands the role of AI, most do not have the capabilities to develop their own cutting-edge models and tools. Simon’s insight was that by giving partners instant access to the best tools, Latent Labs could accelerate the drug design process across the industry.

The combination of a massive financing and a new business model has sparked mixed reactions, both intrigued and skeptical. “Latent’s launch shows how AI-focused startups can break with tradition in biotech,” wrote Andy Dunn of Endpoints. “While most biotech companies are built around a molecule, a research paper, or a key piece of intellectual property, Latent’s investors are betting on the AI talents of Kohl and another former DeepMind developer, Alex Bridgland of AlphaFold, to figure out a way.”

Let’s consider both the bear case and the bull case for this investment thesis.

In a bear market scenario, these technology directions, whether focused on new data generation, model scaling, architectural improvements, or some combination of the three, will not significantly drive progress compared to commoditized technologies.

In his field notes from the MIT Molecular Machine Learning conference, Simon Barnett of Dimension wrote: “My understanding of [Adimab co-founder] Dr. Wittrup’s talk was that he argued that monoclonal antibody (mAb) discovery is largely a solved problem and that the impact of machine learning (ML) on the field has been overstated.”

If AI technologies end up having only a small quantitative impact on problems like antibody discovery, companies offering these solutions may join the multitude of companies vying to provide such services. Rather than the generational giants of around $50 billion to $100 billion, we may see companies with market caps below $1 billion.

What about the bull case? Squint your eyes with me and imagine that the trajectory of AI progress will lead to a qualitative leap, truly leading us to a world of design rather than discovery. Imagine a model that can predict Platonic antibodies with zero shot - perfect affinity and specificity for any target, extremely optimized in every dimension. Input the target product characteristic (TPP) and you get a drug.

That could be a big deal.

An often-cited comparison is Cadence Design Systems, a $66 billion company that makes most of its revenue by licensing its electronic design automation (EDA) software and intellectual property to the semiconductor industry. In high-value areas, the best design tools can be extremely valuable. So could the “Cadence of pharma” be something bigger?

Is there evidence to support this technological trajectory?

Last March, the Baker Lab at the University of Washington published a preprint paper titled “Atomic Precision De Novo Design of Single-Domain Antibodies.” Building on decades of leading work in computational protein design, they introduced an AI model that can efficiently generate miniature antibodies (called VHHs or nanobodies) for specific targets.

Figure 2 Part of: De novo design of a single domain antibody with atomic precision. The binder is shown in pink and the target protein is in turquoise. The designated epitope (i.e., the region to which the antibody binds) is shown in orange.

The results have sparked huge excitement and interest—including a $1 billion bet to get Xaira off the ground. But the work is a proof of concept, not a magical black box that spits out perfect antibodies. The resulting nanobodies still have too weak an affinity for their targets to be drugs, the scientists note. And nanobodies are strange proteins that don’t exactly resemble human antibodies—again, limiting their utility in many clinical applications.

Less than a year later, the Baker lab “significantly updated” their original preprint, renaming it “Atomically precise de novo antibody design using RFdiffusion.” As you might guess, the title was changed because the scope of the research had expanded beyond VHH design. The updated preprint also showed the design of single-chain variable fragments (scFvs), another antibody format that has two variable domains instead of the single variable domain of VHHs.

Another important update is a response to the affinity issue. The authors wrote: "While initial computational designs showed modest affinities, affinity maturation using OrthoRep produced single-digit nanomolar binders that maintained selectivity for the intended epitope." In other words, AI cannot yet generate perfect binders, but they can be quickly adjusted and optimized using existing experimental techniques.

So that’s about a year in. At the risk of drawing a line between two data points, progress seems to be quite rapid. Looking ahead, what if someone creates a massive affinity training dataset using OrthoRep, and this step moves out of the realm of atoms and is encoded in the world of bits in the form of improved model weights?

What will hinder the continued development from VHHs to scFvs to mature monoclonal antibodies in the next five years?

Again, at a cursory glance, we appear to be on the brink of digitization of biologics development. If the advantages in speed, cost—and perhaps quality—are significant enough, this could lead to consolidation in the discovery market, with new entrants quickly capturing a significant share of outsourced work and displacing incumbents.

Now let’s think carefully about what this world of “foundational models” might look like. What if important underlying patterns of biological structure and function were learned across many tasks? As Simon Kohl of Latent Labs told Endpoints, “This vision is much grander. I think we can expand on this, and over time we’ll find that many other areas beyond the molecular interaction level can be guided by generative models.”

So if this — or any part of what I just outlined — is true, some of these companies could become very large.

But one of the biggest threats may well be… commoditization! After all, the entire “deepseek moment” framing stems from the sudden leap in AI capabilities achieved by Chinese research teams with fewer resources than their American counterparts.

There are already signs of this.

To date, Demis Hassabis, co-winner of the Nobel Prize for protein structure prediction and CEO of DeepMind and Isomorphic Labs, has been betting on algorithmic innovation rather than building proprietary data moats to ensure model defensibility. In a recent interview, he said: "Make your algorithms better, make your models better. You do have enough data - as long as you are innovative enough in the algorithms."

What’s surprising is how quickly serious algorithmic competitors have emerged.

In May 2024, Isomorphic and DeepMind published a paper introducing their latest and most advanced structure prediction model AlphaFold3. In September of the same year, Chai Discovery released and open-sourced a cutting-edge model. About two months later, a research team at MIT launched another open-source version with comparable performance.

It will be interesting to see how value will accrue in this new AI race.

Regardless, all of these advances will open up new opportunities for innovation in drug development and elsewhere.

Discovery platforms could become more valuable

Not all biotech platforms focus on therapeutic modalities. Some companies focus on the other side of the coin: identifying new biological targets for drug development. In Steve Holtzman’s “Typology of Platform Companies,” these are called “Insight Platforms.”

About Biotechnology Platform Strategy

Focusing on disease insights comes with its own set of strategic challenges. Holtzman wrote in his original post:

However, Type 2 A-platform companies face a number of challenges that Type 1 platform companies do not face. These challenges are essentially due to the fact that the output of Type 2 A-platform companies is data/information/insights, rather than the production of new chemical entities (NCEs) and biotherapeutics like Type 1 platform companies.

- The history of data in the biopharmaceutical industry is the history of its commoditization.

- Companies whose "lifeline" is drugs/products have a vested interest in "pre-competitiveizing" data (or at least doing so after a period of exclusivity). They win with their products; they don't want to be tied to the owner of the information.

- The intellectual property (IP) environment is becoming increasingly stringent: gone are the days when you could obtain a patent authorization in the form of logic such as "a method for treating disease X by regulating target A by any means" simply by demonstrating the transcriptional profile of a gene being overexpressed in diseased tissue (or a gene mutation in a disease state) (with the accompanying claims stating that the "means" can be antibodies, antisense nucleic acids, RNA interference, gene therapy, small molecules, etc.).

- Furthermore, over time the demands of the client base have become more broad. Whereas in the 1990s most large pharma clients were willing to accept terms that limited the use of data to small molecule drug discovery and development (because that was the only area they were in), today all pharma/large biotech companies will demand the right to use the data for all therapeutic modalities.

- Finally, a Genus 2, Species A platform company has and built its expertise in the generation, management, and analysis of data. It does not have or cannot afford to invest in significant capabilities for drug discovery/development in one or more therapeutic modalities, or in deep biology/translational capabilities in one or more disease areas.

- End result: Genus 2, Species A platform company abandons its data/information business and builds and becomes a drug discovery and development business.

Let’s break it down.

First, it’s important to recognize that the data-generating technology itself has gone through a long process of commoditization. (It’s technology, people!) Second, the main problem in the past has been asymmetric negotiations with large partners—they once had exclusive access to discovery technologies, which gave them an unfair advantage in actually creating chemicals against new targets.

This dynamic has begun to shift. The growth and maturity of the CRO industry has enabled insights companies to enter partner discussions with their own new chemical entities (NCEs) rather than just patents around target insights.

What if AI accelerates this dynamic? Over time, as modalities become more commoditized, the time and cost to go from target insight to developable chemistry could compress further.

In this world order, the balance could tip. New disease insights against known targets could be more valuable than any incremental starting point in chemical space.

After all, the $100 billion-plus success story of GLP-1 drugs was built on biological insights, not advances in technological models.

Several economic and technological realities are likely to slow progress in this regard.

On an economic level, as David Yang brilliantly points out, part of the reason GLP-1 is a success story for pharma rather than biotech is because of the centrality of M&A to the industry. Most early-stage biotech investors are banking on cash flow from big acquisitions, which means they keep a close eye on the acquisition lists of the pharma giants. And pharma buyers are really reluctant to spend billions of dollars to test new biological hypotheses—especially when the size of the market opportunity is unclear.

How can we change this and unleash a new wave of more innovative medicines? We need to continue to reduce the time and cost of every step from discovery to development to commercialization.

Doing so will make early-stage drug discovery more valuable.

Improving discovery and commercialization capabilities appear to be both technical issues. Accelerating development may require new technologies and regulatory reforms. Learning from China’s experience (this time with a different mindset!) and studying its recent reform initiatives may provide a good starting point for the latter.

On a technical level, it is important to recognize that modeling human biology is a much more difficult AI problem than modeling a specific modality. Consider two questions: Does my antibody bind this target with higher affinity? What effect does activation of the GLP-1 receptor have on overall human physiology? The tools to definitively answer the first question are already available in the lab. The answer to the second question will only be fully known after first-in-human trials, as our preclinical models are only crude approximations of human biology.

Modeling human biology more effectively will likely require massive amounts of data generation and continued progress on new AI paradigms.

Over time, addressing these economic and technological challenges could dramatically reshape the biopharmaceutical industry landscape, ushering in a wave of emerging commercial biotech companies advancing bold new therapies.

But in the long run, all these rapidly accumulating technologies may also lead to a more radical departure from traditional biotech business models.

Moats can be very different

In most industries, there are multiple viable strategies for building a lasting competitive advantage. The classic 7 Powers framework developed by Hamilton Helmer was designed to enumerate the most commonly adopted approaches.

The 7 major forces are:

- Economies of scale – A business where unit costs fall as output increases.

- Network economics – a business model where the value realized by customers increases as the user base expands.

- Reverse positioning – The company adopts a new, superior business model that existing companies are unable to emulate for fear of cannibalization of their existing business.

- Switching Cost – A business model where the customer expects the loss from switching to an alternative is greater than the value gained.

- Brand Effect – Due to the influence of historical information, a company enjoys a higher perceived value when providing objectively identical products or services.

- Trapped Resource – A company has preferential access to a coveted resource that independently enhances value.

- Process power – A company’s organizational structure and combination of activities enable it to achieve lower costs and/or higher quality products that can only be matched by long-term investment.

At the risk of oversimplifying, in biopharma, only two forces really matter. Big pharma benefits from economies of scale because they are able to amortize the costs of development and commercialization across revenues from their existing portfolios. And for biotechs, essentially the only real source of power is monopoly resources in the form of control over new intellectual property (IP).

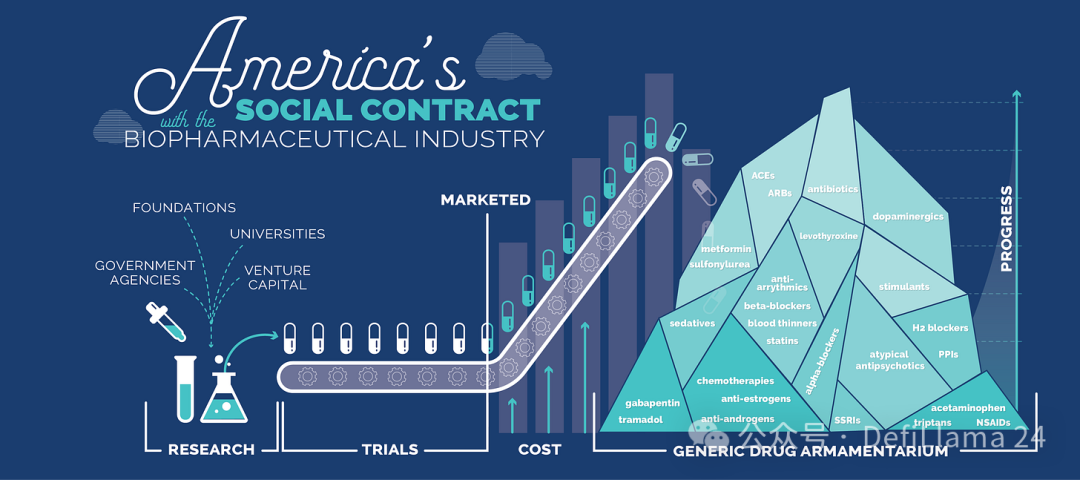

As Peter Drucker once wrote, “Pharmaceuticals is an information industry.” The value of a small-molecule drug is independent of its physical form, which is worth next to nothing. The ability to charge the highest margins of any existing physical product is purely a function of intellectual property. Once intellectual property expires, generic drugmakers can quickly step in and offer drastically reduced prices.

This is what RA Capital’s Peter Kolchinsky defines as the “social contract of biotech.” Scientists and entrepreneurs are rewarded for their innovations with patent exclusivity. But that exclusivity is limited. Once it expires, innovative drugs become cheap commodities that future generations can afford.

Source: The U.S. Social Contract with the Biopharmaceutical Industry

The concern with commoditization is that this may soon become a social contract between China and the biopharmaceutical industry - as long as they can produce products with equivalent intellectual property at a lower cost and faster speed.

But what if there was a different way to build defensive barriers in biotechnology?

There are some early examples pointing to defensive orthogonal forms. It’s hard to predict what the genericization of CAR-T therapy — a new form of medicine that rewires a patient’s own cells to kill cancer — will look like. In his book on the Social Contract in Biotechnology, Kolchinsky actually expressed concerns about this. The companies that sell these drugs may have a moat from process power rather than monopoly resources around intellectual property.

Now let's move forward in time.

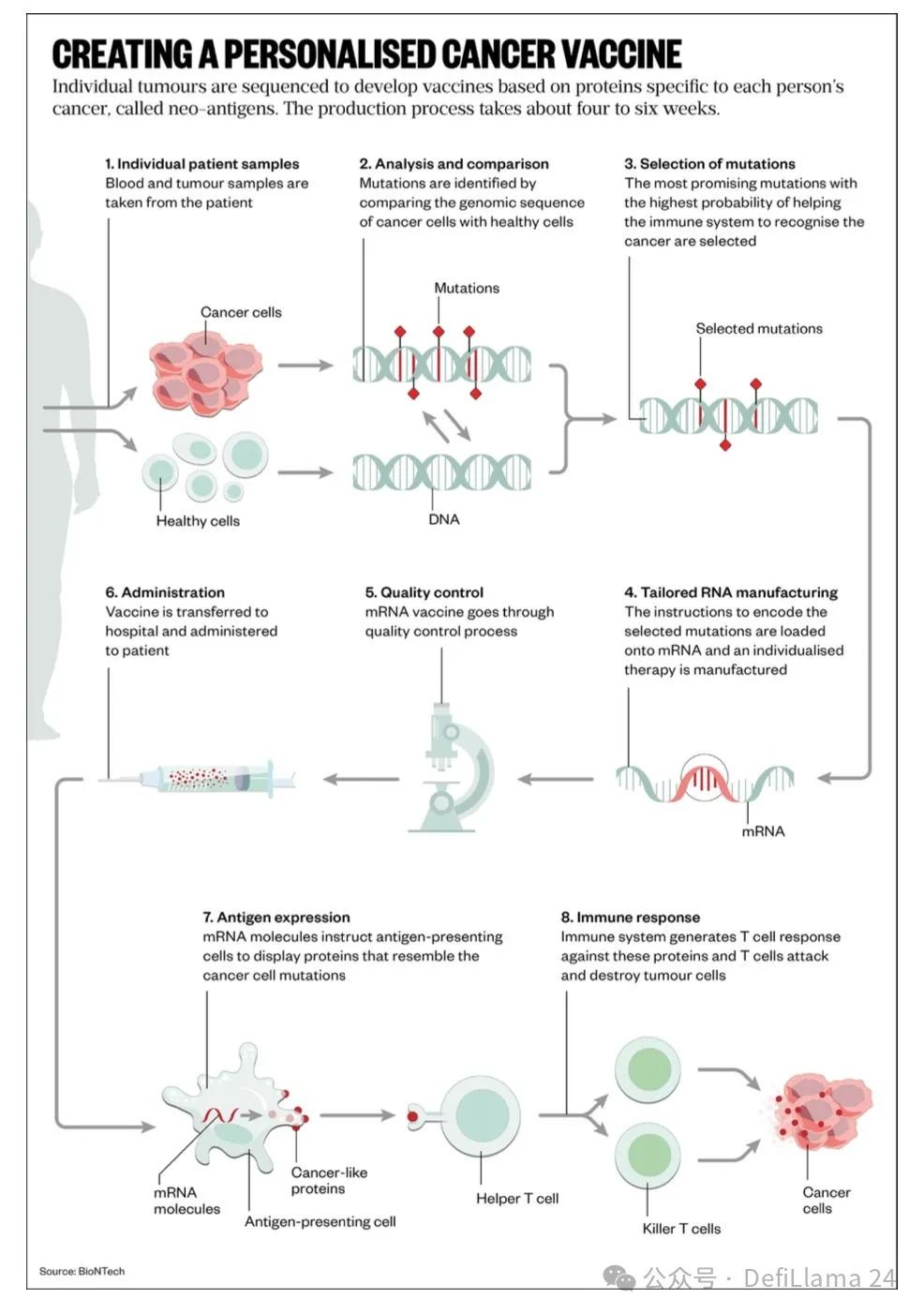

Personalized cancer vaccines are another treatment that takes on this form. The core of these drugs is not made up of a single chemical ingredient. Instead, each dose is made through a complex combination of patient measurements, algorithms, and manufacturing steps.

This has very interesting consequences. This could be the first medicine to have network economics. Since each dose is designed algorithmically, its quality could improve as more data is collected. Patients could benefit from medicines made by companies with the largest data barriers. This approach also clearly benefits from process power. Over time, the winner of this new model could even accumulate significant brand advantages as a market leader.

If more forms of drugs begin to follow this trend, we may see a wave of biotech companies competing directly to establish themselves as a whole new generation of pharmaceutical companies.

At this point, I can’t help but think of what my good friend Packy McCormick has to say about vertical integrators. In his words, these companies have several defining characteristics:

Vertically integrated businesses are those that:

- Integrate multiple cutting-edge and proven technologies.

- Develop significant internal capabilities in its technology stack.

- Modular standardized components while controlling overall system integration.

- Compete directly with existing industry giants.

- Delivering a better, faster, or more economical product (usually all three).

For vertical integrators, integration itself is innovation.

As always, this strategy faces obvious challenges. There is no such thing as a free lunch!

A huge hurdle is likely to be financing and capital formation. This way of creating a company is completely different from the way most biotech investors think about generating returns. It is not at all clear that big pharma will be willing to acquire a company with such a complex product without clear proof of commercial viability.

Winners in this space may need to look elsewhere for funding. One possible option is to tap into the growing pool of "deep tech" venture capital, which is focused on backing breakthroughs in hardware and innovations in the atomic world. Late-stage investments could come from generalist growth equity firms rather than traditional biotech crossover funds.

Trying to build a vertical integrator in biotech is not for the faint of heart.

Combining multiple technologies in new ways is not easy. Financing will be challenging. Scaling up commercialization efforts will also be difficult. Success may take much longer than expected.

Given all these factors, biotech investing may begin to mirror the overall evolution of the private market. Companies may stay private longer. SpaceX, for example, has raised nearly $10 billion in funding in its 23 years as a private company and is now valued at $350 billion. Liquidity for early investors and employees is coming primarily from secondary markets, rather than M&A deals or IPOs.

Despite the difficulties, the potential rewards are huge.

Once-unthinkable measurement tools are now commonplace in biology. The fundamental insights that fueled the last wave of biotechnology have been refined and commoditized. Artificial intelligence is accelerating biology’s transformation into a predictive and quantitative discipline.

Addressing major problems that have been intractable to previous approaches, such as cancer, infectious diseases, and brain health, may require innovative solutions that integrate multiple digital and physical building blocks.

If these global problem-solving companies build moats in new ways, we may see the birth of the first biotech companies with market caps exceeding $1 trillion.

Things are looking pretty bleak in the public biotech market right now. For U.S. biotech companies, the continued rise in Chinese acquisition activity further threatens their prospects for success. As Adam Feuerstein writes, “Sentiment is so bad and pessimism is so lingering that people are starting to seriously question whether the industry can ever turn around.”

At the same time, early-stage markets are full of potential. The pace of technological innovation is also rapid. Entrepreneurs who have learned valuable lessons and mastered powerful tools are pursuing new ideas.

Maybe the right question isn’t whether the market will rebound. Because it will. Markets are cyclical. Instead, the question is whether biotech is on the verge of a shift to a whole new phase. If so, now is the best time to start a business.

in other words……

Biotech is dead. Long live biotech!