Author: @lazyvillager1, Crypto Kol

Compiled by: zhouzhou, BlockBeats

Editor's note: COIN and BTC have risen significantly since Trump's victory, but the author prefers ETH and is optimistic about the development of the Base L2 ecosystem. Base is expected to stand out from the competition and attract MEME, consumer dApps, and more on-chain activities. ETH is still the core of digital assets, and Base, as the on-chain leverage of Coinbase, benefits from Coinbase's resources and support, has scarcity and innovation, can attract users in the long run, and does not rely on traditional token incentives. The activeness of the Base ecosystem and the continued growth of TVL prove its great potential in ETH-L2.

The following is the original content (for easier reading and understanding, the original content has been reorganized):

Basic judgment on future development

Since Trump's victory on November 5, COIN and BTC have led the way, up 70% and 16% respectively. I personally still prefer ETH, and based on the theme of MEME coins I wrote in October, I believe that multiple favorable factors are converging for the Base L2 ecosystem:

1. “Win” the competition with other L2s and even the ETH mainnet to become the preferred ecosystem to accommodate MEME, consumer dApps and attract attention

2. Compete with SOL’s “full-featured” integrated casino model as the top EVM-compatible ecosystem

My core point is simple. ETH remains the key center of the digital asset ecosystem. All derivative projects to date rely on two core principles to drive network effects:

a. The “underlying” currency must have strong performance relative to its competitors;

b. The underlying currency must be scarce

So in this race for attention, most of the time you’re actually picking a coin (even if it’s just a simplified way) to show its superiority. In the next few weeks (this trend has already started), the CT community will discuss why a coin might win (such as SOL’s opponents, or MEME coins) or why an application supporting a coin might win (such as utility tokens, DeFi governance, etc.).

I would argue that a more risk-adjusted option from today is to bet on an ecosystem without a coin. In my opinion, Base is organized in a way that creates the strongest potential for continued adoption, with the double-edged sword that it may rely on the resurgence of ETH.

However, given that I believe ETH’s potential is currently underestimated - if/when the relative value between BTC, ETH, and SOL increases in the coming weeks, a “reservoir” will inevitably be needed to accommodate this newly generated and circulating wealth.

I think Base is poised to win this position.

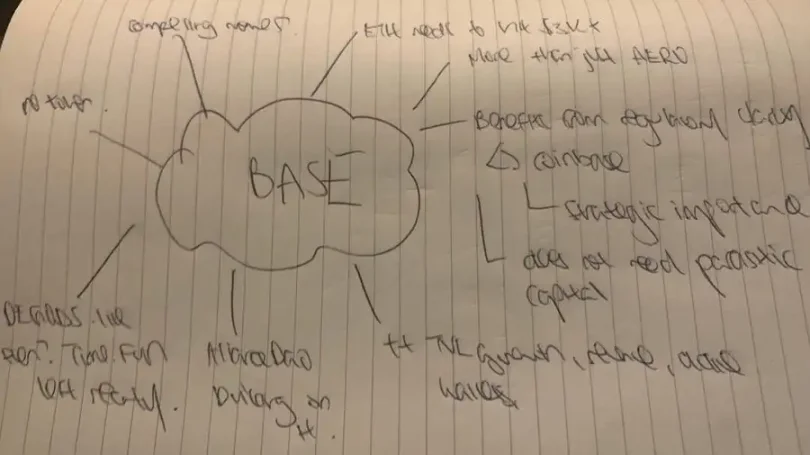

- The connectivity of the "faucets" on Base has been greatly improved this year, but it has not received enough attention.

- Base has significant strategic value to COIN and has a real balance sheet to back it up.

- Base has been tested many times this year and performed quite well.

I have adjusted my layout accordingly and will discuss in detail in subsequent posts my logic and the risks and mitigations involved in redirecting on-chain traffic to Base, which I believe is the most vibrant "playground".

memecoin and the environment in which it is usually successful

The key point is that low-cap memecoins generally provide uncorrelated returns, while on-chain activity often heats up around major uncertainties.

Reflecting on the strength of major assets and their impact on on-chain activity

Based on the above, I believe that on-chain activity will show very strong performance in the next few weeks.

The performance of major assets supports this trend - buying is mainly driven by spot, with open interest (OI) for ETH and BTC mostly reset to pre-election levels, and the rise in funding rates is mainly due to the lack of new short establishment (and the levels broken in recent days - the amount of short liquidation has reached $1 billion, the highest this year), rather than the use of excessive leverage.

Therefore, based on the idea that the current price range is supported, I think on-chain activity will become a place for OTC funds, new funds and recycled funds to gather. The funds created in the past week are in contrast to the funds in the 3-4 weeks before the election. The latter saw a large increase in funding and open interest, but other than BTC, other assets had difficulty in attracting what I call "mercenary funds".

The flow of funds in the past week has not only appeared widely in assets other than BTC (all selected assets have generally risen globally), but even DOGE - this is a very important indicator that reflects the characteristics of these "buyers": willing to use leverage, willing to speculate and trade 24 hours a day. These buyers are not restricted to US trading hours, which is similar to the rise of BTC in October.

We are less than a week into this price environment - the dislocation in the market is significant: capital needs time to assess whether these flows are irrational or substantial. During this period, projects that are able to move significantly at the margin should have the most significant re-rating effects.

Base is already “winning” — even though it has no tokens

Base is probably one of the most misunderstood ecosystems out there, and due to the way it is built, Base lacks the typical crypto-native investors/KOLs to curate and spread the message. However, by all metrics, Base is “winning.” The ratio of attention Base attracts to its user/wallet/TVL growth is probably the most disproportionate of all projects out there.

Please see the figure below, which is elfa ai's capture of Base's attention. In terms of collective mentions, there were about 18 mentions on CT in the past 7 days, which is 10 times lower than ARB and roughly equivalent to the number of mentions on STARKNET, BLAST, and OP.

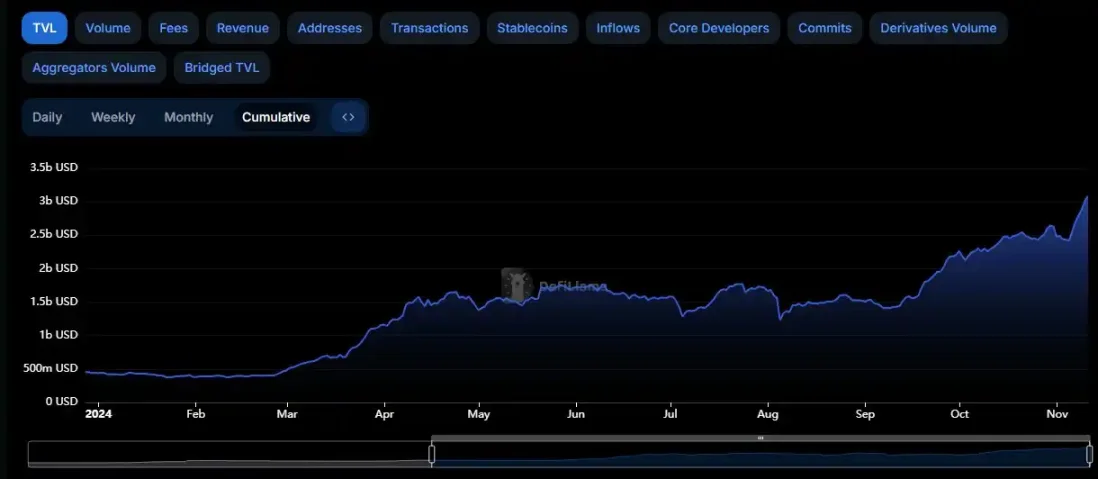

It is the only ETH-L2 to have seen a consistent increase in TVL throughout the year, despite not having user incentives like other L2s (like BLAST GOLD). At $3 billion in TVL, its TVL even exceeds that of ARB (which hosts the very popular HyperliquidX, which has ~$1 billion in TVL).

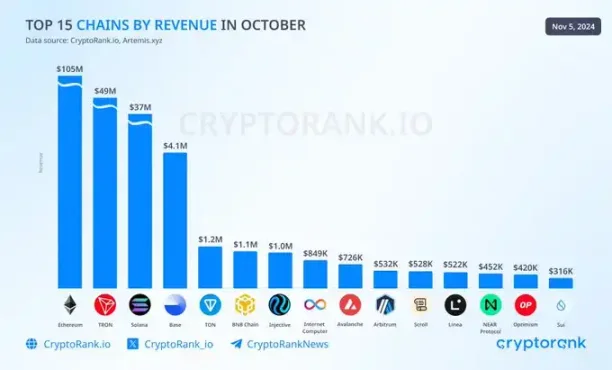

Base also had the highest revenue in the growing ecosystem in October (a month where TRON declined and Base and ETH grew). Base also currently has the most unique active wallets and transactions (actual data should be treated with caution, but this is the only picture we can paint).

Base is reminiscent of last year’s fourth quarter SOL – an environment that attracted builders when attention was low.

Base subverts and breaks the traditional L1/L2 operation mode

The traditional operation mode is usually as follows:

1. Have an idea for an ecosystem, ideally with unique variants (faster, more reliable, more decentralized, easier to build, less trust, etc.)

2. Raising funds by giving away tokens at almost zero valuation (usually to companies with the best connections and resources)

3. Connect with dApp developers while building - Each blockchain will typically look for a local "bank", so there will likely be some type of lending protocol as well as a trading protocol. Developers are paid via token rewards for on-chain development.

4. Attract users through point/token incentive programs, where users deposit/pledge stable capital to receive yield rewards.

5. Users/added TVL provide the founding team with a foundation to raise capital from a new round of investors and conduct a second round of financing at a higher valuation - and indicates an inflow of users/capital.

6. After the blockchain is launched, users will first receive rewards through non-locked tokens; while investors and team members will have to wait through locked tokens. (But the proportion is much larger)

7. Lending protocols typically establish partnerships with market makers and investors to deposit and maintain capital on-chain by promising returns.

8. Over time, the hope is to get organic capital flowing in and staying there through certain metrics (e.g., connectivity, ease of use, ecosystem richness, etc.) — thereby reducing or eliminating the need for dilutive capital.

9. The founding team pays early supporters and employees with tokens - at this point the tokens effectively become free expenses (used to pay suppliers). Ideally, the ecosystem supports the sustainability of the chain by serializing revenue.

This model is ripe for disruption, with HyperliquidX being the most prominent example of a startup that doesn’t rely on traditional means and ignores most of the above measures.

This year, this capital raising method has clearly failed in many aspects, with the following pain points:

Mining incentives are often very unclear, and once capital is locked up, it becomes hostage, allowing teams to change terms retroactively without regard for the consequences.

Investors/team members can stake locked tokens - this allows staking rewards to be sold at the TGE (token generation event) even if the original locked tokens are illiquid, severely diluting retail investors.

New capital is expensive (and the opportunity cost is extremely high in crypto), so without significant dilution or supply manipulation, users are very utilitarian and will generally leave once rewards are distributed.

Why is Base more likely to be more successful?

Base is more than just an L2, it is Coinbase’s on-chain leverage — an opportunity Coinbase gained through the reduced regulatory scrutiny (i.e., improved policy environment) brought about by Trump’s victory.

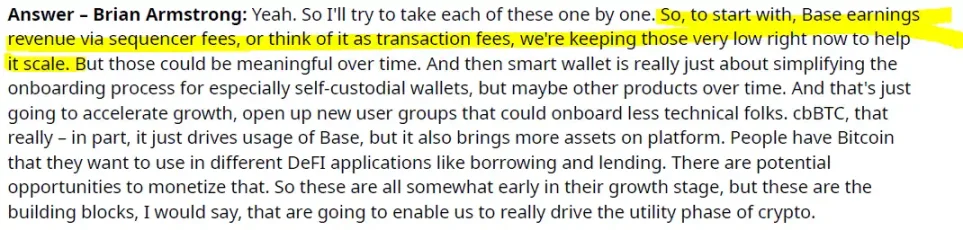

In other words, Base is not going to win through the traditional “fat tail” approach I mentioned above, so what does that mean? Here is an excerpt from Coinbase’s Q3 conference call showing how the team thinks about Base:

Base is (partially):

1. Synergy test platform with CIRCLE, and development of smart wallets. Coinbase can collect data in real time and comprehensively build a truly independent "Garden of Eden" ecosystem (i.e.: i. Attract users, ii. Seamless onboarding, iii. Setting up smart wallets by using pass keys instead of traditional secret phrase records, iv. Providing a "playground" for speculation)

2. As Coinbase transitions to a recurring service business (such as through Coinbase One subscriptions, etc.) rather than relying on volatile transaction fees, the team's vision is to attract the most retail users in the long term rather than charging as much fees as possible in the short term.

The latter is the epitome of the extractive value capture model that every blockchain follows - due to the creation of tokens and their inherent nature. By separating the ecosystem from the token, Base is able to take a longer-term perspective to "win." In other words, the only way Base will make money in the future (because COIN already exists as equity) is by getting applications and users to pay "rent."

The most important point is:

The biggest difference between Base and other blockchain projects is that it is backed by a business with a real balance sheet. Any other ecosystem, at least at some point, is supported by counterparties with financial incentives who seek returns. And these counterparties themselves do not have unlimited capital.

Once the payoff is achieved, the support (whether financial or community) will go away. So other ecosystems have a life cycle, or a time limit, where new support money eventually stops coming in and the product is left to fend for itself. You will see some ecosystems start to struggle (e.g. shut down platforms) in the next 12 to 16 months.

This may not be the case with Base <> Coinbase. If Base ceases to receive support, it means that an important part of Coinbase has failed (and thus the overall strategic vision has failed). Since Coinbase itself generates traffic and revenue through the "where the price is" approach, we can speculate that Base may receive a kind of "evergreen" funding support.

Base proves its resilience

Base started out as the base platform for Friend Tech (basically a shell with limited functionality at the time). Since then, it has gone through several important phases:

1. Application migration, such as timedotfun. Please see jessepollak's response: link. This is a very positive attitude and supportive spirit, understanding that each chain has its own unique value.

2. The only project that successfully incubated another L2 - degentokenBase. The attention DEGEN received on a weekend earlier this year quickly pushed its valuation to $600 million, comparable to the self-building and rise of apecoin this month.

3. The only chain that can accommodate AI-related applications like SOLANA - VIRTUAL, went from 0 to 500 million US dollars during the AI and memecoin craze in October this year.

In my opinion, no other ecosystem could sustain this level of attention and drive this level of capital inflow. So the question is: if other ecosystems can do this, why don’t they do it? So Base has clearly demonstrated the ability to support new and interesting projects/applications that go far beyond simple yield loops or lending applications.

Here are some other examples:

- warpcast

- BlueSocialApp

- OnchainKit

- liberoverse

- Sofamon xyz

- BetBase xyz

- dreamcoinswow

- ethxy

This isn’t an exhaustive list, nor an endorsement of any of the names mentioned here, but simply a snapshot of the incredibly diverse creative projects that have been built on Base since its last iteration, especially during the Friend Tech era when most of these apps hadn’t officially launched yet.

Buy at a point that is considered a value bottom

Profiting on Base is essentially betting on the success of the entire ecosystem, even as a proxy for Coinbase. No single token can concentrate demand, so true network effects can be achieved as a whole.

Most of the tokens on Base are currently trading at cycle lows - and I won’t be providing any token names or recommendations, but you can see some chart examples, which I randomly selected.

Therefore, I believe Base is the most attractive place to put capital because you are essentially betting on two things — and this has nothing to do with leverage or savvy token selection:

1. ETH stabilizes and finds a floor that provides on-chain demand (which I’ve discussed before),

2. ETH winners want to recycle their profits somewhere.

Given the lack of organic options on the MainNet (MN) (which have been moved to L2) and the lackluster demand in the NFT market this year, I’m betting that the attention and money will be focused on Base.

In summary - as long as ETH remains hot, Base should also remain hot.