Stablecoin Playbook: Flipping Billions to Trillions

By Rui Shang, SevenX Ventures

Compiled by: Mensh, ChainCatcher

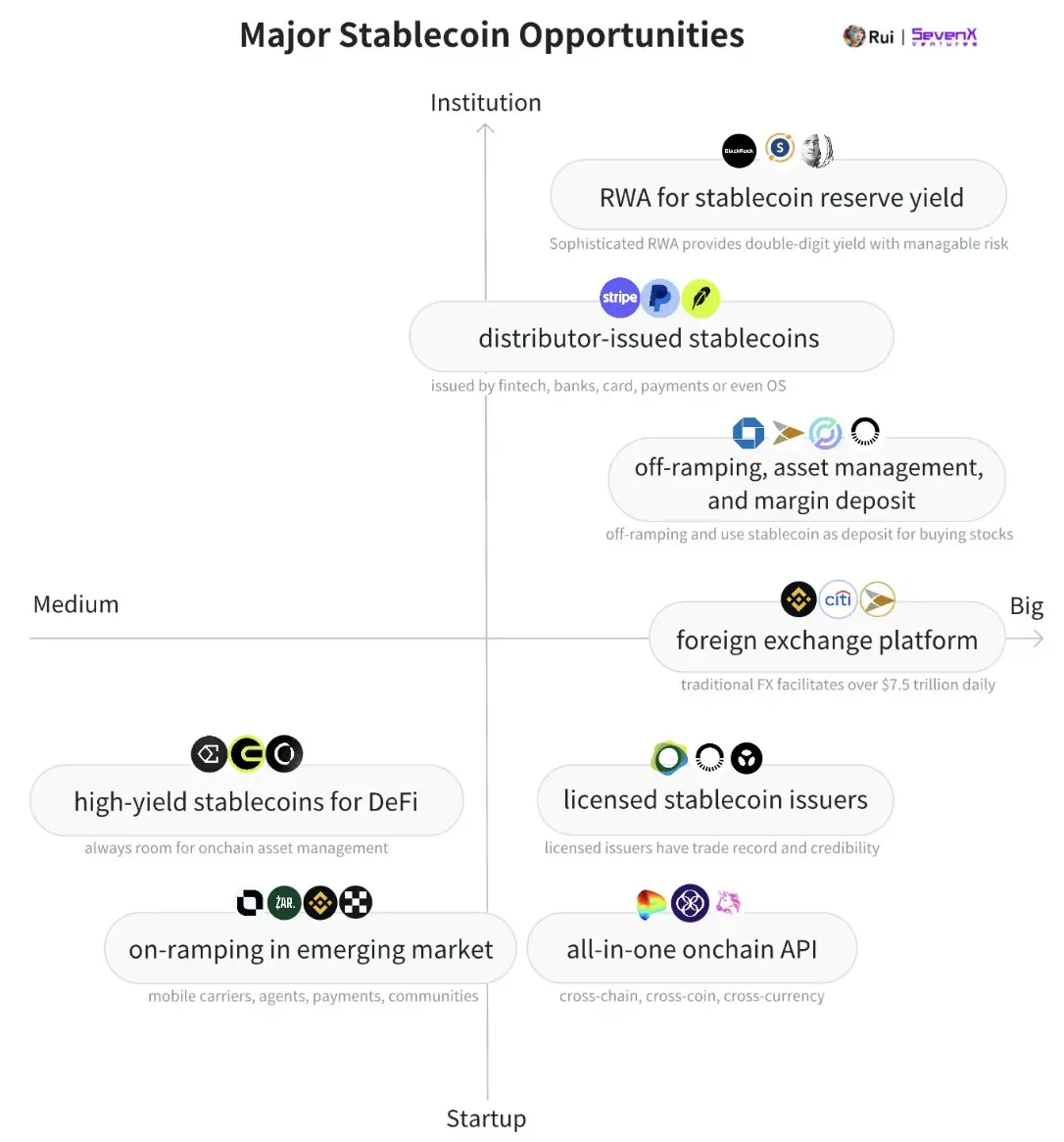

Overview: 8 major stablecoin opportunities

The younger generation is a digital native, and stablecoins are their natural currency. As AI and IoT drive billions of automated microtransactions, global finance needs flexible monetary solutions. Stablecoins, as "currency APIs," are transferred as seamlessly as Internet data and reached a transaction volume of $4.5 trillion in 2024, a figure that is expected to grow as more institutions realize that stablecoins are an unparalleled business model - Tether made $5.2 billion in profits in the first half of 2024 by investing its US dollar reserves.

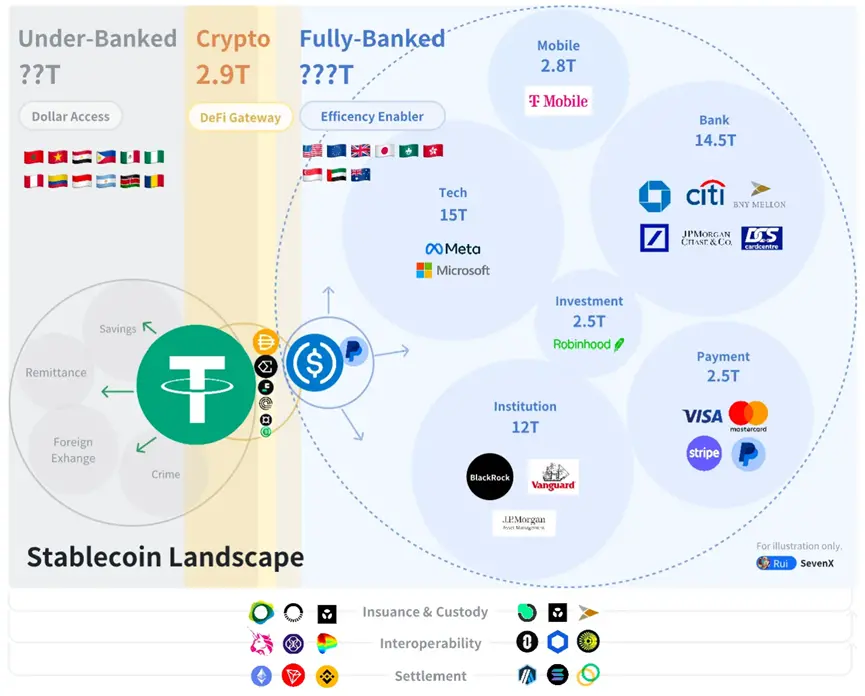

In the stablecoin race, it is not the complicated cryptographic mechanisms that matter, but distribution and real adoption. Their adoption is mainly reflected in three key areas: crypto-native, fully banked, and unbanked worlds.

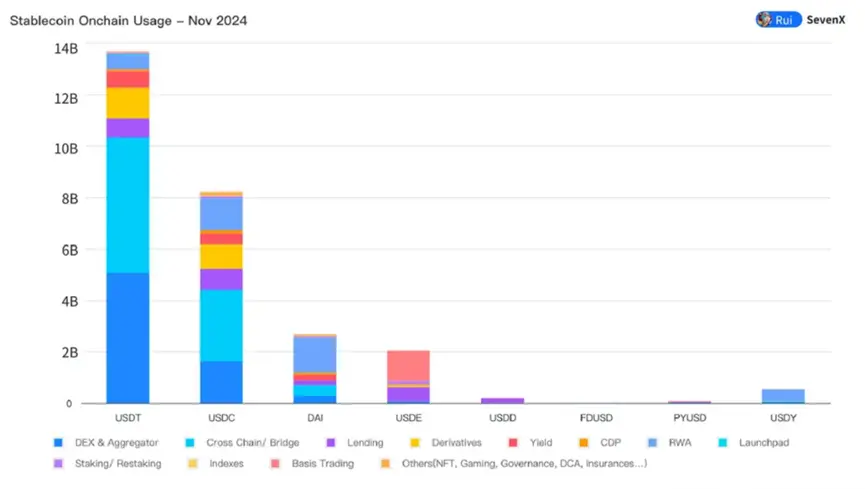

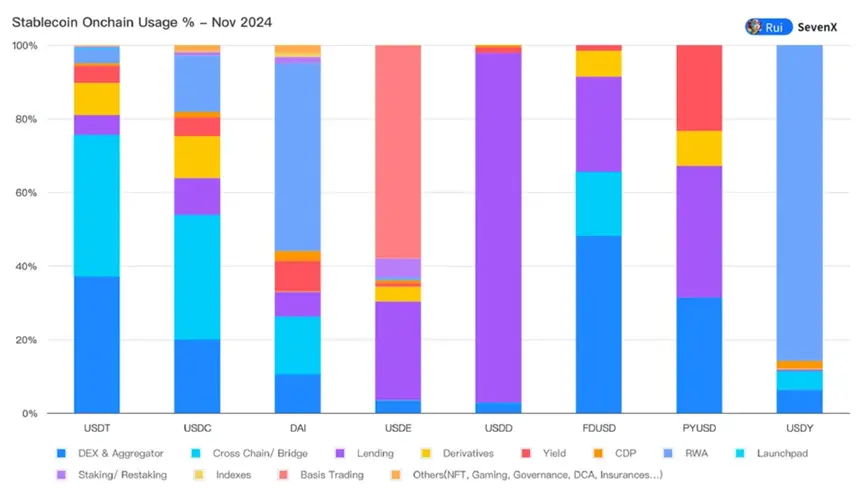

In the $29 trillion crypto-native world, stablecoins are the gateway to DeFi and are essential for trading, lending, derivatives, liquidity farming, and RWA. Crypto-native stablecoins compete through liquidity incentives and DeFi integration.

In a fully banked world of over $400 trillion, stablecoins increase financial efficiency and are primarily used for B2B, P2P, and B2C payments. Stablecoins focus on regulation, licensing, and leveraging banks, card networks, payments, and merchants for distribution.

In an unbanked world, stablecoins provide access to USD, promoting financial inclusion. Stablecoins are used for savings, payments, foreign exchange, and yield generation. Grassroots market outreach is critical.

Natives of the Crypto World

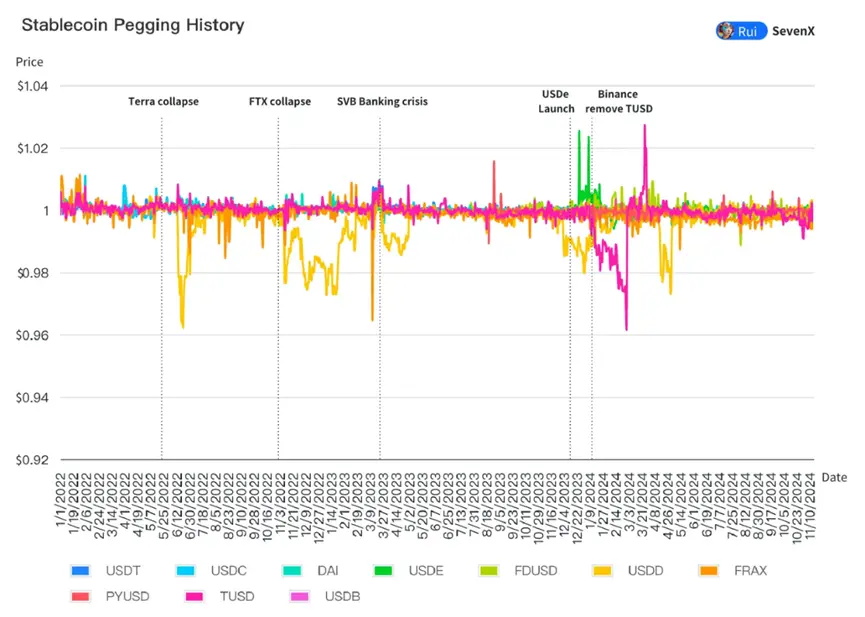

In the second quarter of 2024, stablecoins accounted for 8.2% of the total crypto market capitalization. Maintaining exchange rate stability remains challenging, unique incentives are key to expanding on-chain distribution, and the core problem lies in the limited on-chain applications.

The battle to anchor the dollar

- Fiat-backed stablecoins rely on banking relationships:

93.33% are fiat-backed stablecoins. They have greater stability and capital efficiency, and banks have the final say by controlling redemptions. Regulated issuers like Paxos became the USD issuer for PayPal due to their successful redemption of billions of BUSD.

- CDP stablecoins improve collateral and liquidation to increase exchange rate stability:

3.89% are Collateralized Debt Position (CDP) stablecoins. They use cryptocurrencies as collateral but face issues with scaling and volatility. CDPs have improved their risk resistance by accepting a wider range of liquidity and stable collateral by 2024, with Aave's GHO accepting any asset in Aave v3 and Curve's crvUSD recently adding USDM (real assets). Some liquidations are improving, especially soft liquidations for crvUSD, which provides a buffer against further bad debt through its custom automated market maker (AMM). However, the ve-token incentive model has problems because when CRV's valuation drops after large-scale liquidations, crvUSD's market cap also shrinks.

- Synthetic USD remains stable using hedging:

Ethena USDe alone has captured 1.67% of the stablecoin market share in a year, with a market cap of $3 billion. It is a delta-neutral synthetic dollar that fights volatility by opening short positions in derivatives. Funding rates are expected to perform well in the upcoming bull market, even after seasonal fluctuations. However, its long-term viability is questionable as it relies heavily on centralized exchanges (CEX). With the increase of similar products, the influence of small funds on Ethereum may weaken. These synthetic dollars may be vulnerable to black swan events and can only maintain low funding rates during bear markets.

- Algorithmic stablecoins fell to 0.56%.

Liquidity onboarding challenges

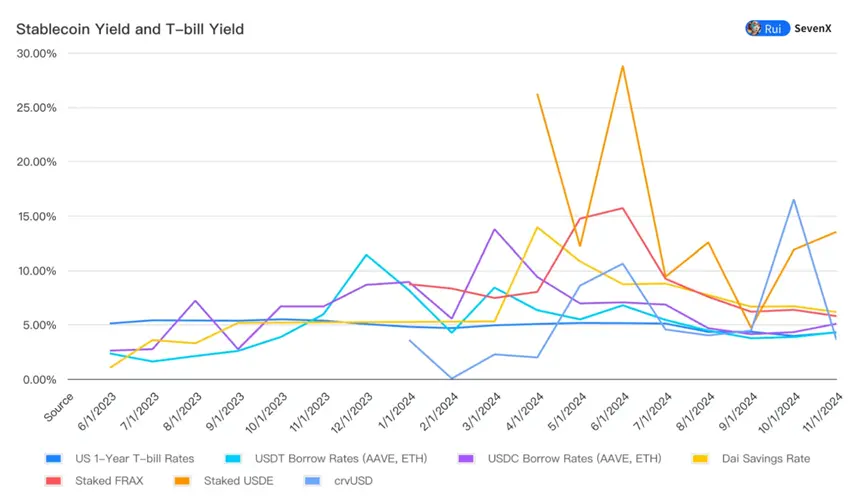

Crypto stablecoins use yields to attract liquidity. Fundamentally, their liquidity cost consists of the risk-free rate plus a risk premium. To remain competitive, stablecoins must offer yields at least as good as the Treasury bill (T-bill) rate — we’ve seen stablecoin borrowing costs fall as T-bill rates hit 5.5%. sFrax and DAI are leading the way in T-bill exposure. By 2024, multiple RWA projects have increased the composability of on-chain Treasuries: CrvUSD uses Mountain’s USDM as collateral, while Ondo’s USDY and Ethena’s USDtb are backed by Blackstone’s BUIDL.

Based on Treasury rates, stablecoins employ a variety of strategies to increase risk premiums, including fixed budget incentives (such as issuance on decentralized exchanges, which can lead to constraints and death spirals); user fees (tied to lending and perpetual contract trading volume); volatility arbitrage (falling when volatility subsides); and reserve utilization, such as staking or re-staking (less attractive).

In 2024, innovative liquidity strategies are emerging:

- Maximizing intra-block yields: While many yields currently derive from self-consuming DeFi inflation as an incentive, more innovative strategies are emerging. By using reserves as a bank, projects like CAP aim to direct MEV and arbitrage profits directly to stablecoin holders, providing a sustainable and more lucrative source of potential yield.

- Compounding with Treasury Bill Returns: Leveraging the new compounding capabilities of RWA projects, initiatives like Usual Money (USD0) offer “theoretically” unlimited returns through their governance tokens, benchmarked to Treasury bill returns — attracting $350 million in liquidity providers and entering Binance’s launch pool. Agora (AUSD) is also an offshore stablecoin with Treasury bill returns.

- Balanced high returns against volatility: Newer stablecoins adopt a diversified basket approach to avoid single returns and volatility risks and provide balanced high returns. For example, Fortunafi's Reservoir allocates treasury bills, Hilbert, Morpho, PSM, and dynamically adjusts each part to include other high-yield assets when necessary.

- Is TVL a flash in the pan? Stablecoin yields often face scalability challenges. While fixed budget yields can provide initial growth, as TVL grows, yields are diluted, causing the yield effect to weaken over time. Without sustainable yields or real utility in trading pairs and derivatives after incentives, its TVL is unlikely to remain stable.

The DeFi Gateway Dilemma

On-chain visibility allows us to examine the true nature of stablecoins: are stablecoins a true representation of money as a medium of exchange, or are they simply financial products that generate returns?

- Only the best yielding stablecoins are used as trading pairs on CEX:

Nearly 80% of trading still happens on centralized exchanges, with top CEXs supporting their "preferred" stablecoins (e.g., FDUSD on Binance, USDC on Coinbase). Other CEXs rely on overflow liquidity from USDT and USDC. In addition, stablecoins are working to become margin deposits on CEXs.

- Few stablecoins are used as trading pairs on DEX:

Currently, only USDT, USDC, and a small amount of DAI are used as trading pairs. Other stablecoins, such as Ethena, whose 57% of USDe is staked in its own protocol, are purely held as financial products to earn returns, far from being a medium of exchange.

- Makerdao + Curve + Morpho + Pendle, combined allocation:

Markets like Jupiter, GMX, and DYDX prefer USDC for deposits because the minting-redemption process of USDT is more skeptical. Lending platforms like Morpho and AAVE prefer USDC because of its better liquidity on Ethereum. On the other hand, PYUSD is mainly used for lending on Solana's Kamino, especially when the Solana Foundation provides incentives. Ethena's USDe is mainly used for Pendle for yield activities.

- RWA is underrated:

Most RWA platforms, such as Blackstone, use USDC as a minting asset for compliance reasons, and Blackstone is also a shareholder of Circle. DAI has been successful in its RWA product.

- Expand the market or explore new areas:

Although stablecoins can attract major liquidity providers through incentives, they face a bottleneck - DeFi usage is declining. Stablecoins are now in a dilemma: they must wait for the expansion of crypto-native activities or seek new utility beyond this field.

An outlier in a fully banked world

Key players taking action

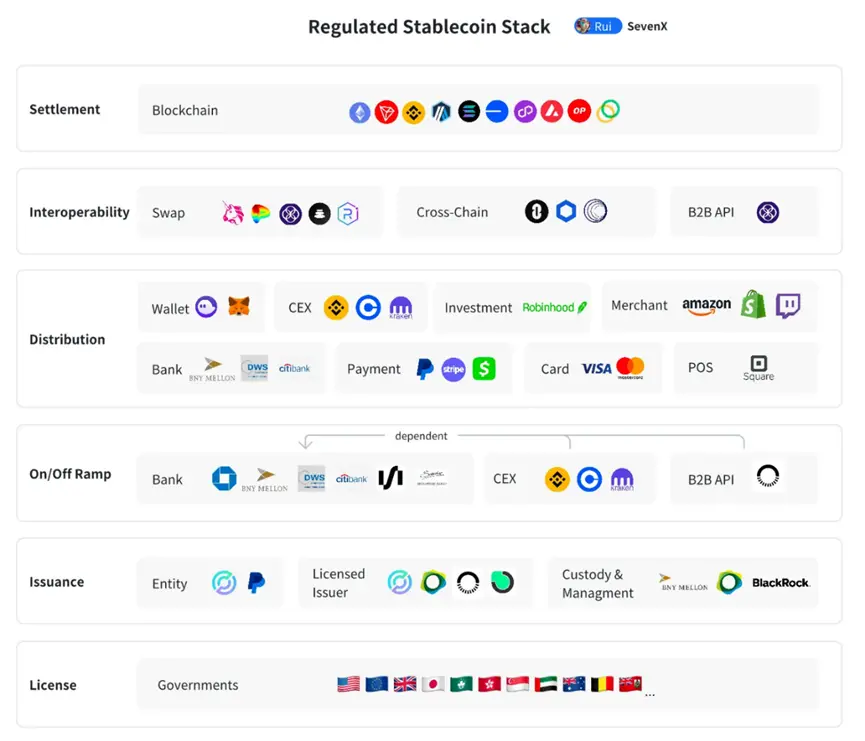

- Global regulation is becoming clearer:

99% of stablecoins are backed by the US dollar, and the federal government has ultimate influence. The US regulatory framework is expected to be clarified after the crypto-friendly Trump presidency, and his promises of lower interest rates and a ban on CBDCs could be a boon to stablecoins. The US Treasury report noted the impact of stablecoins on demand for short-term Treasury bonds, with Tether holding $90 billion in US debt. Preventing crypto crime and maintaining the dominance of the US dollar are also motivations. By 2024, multiple countries have established regulatory frameworks under common principles, including approval of stablecoin issuance, reserve liquidity and stability requirements, restrictions on the use of foreign-currency stablecoins, and generally prohibitions on the generation of interest. Key examples include: MiCA (EU), PTSR (UAE), Sandbox (Hong Kong), MAS (Singapore), PSA (Japan). Notably, Bermuda became the first country to accept stablecoin tax payments and license the issuance of interest-bearing stablecoins.

- Licensed issuers gain trust:

The issuance of stablecoins requires technical capabilities, inter-regional compliance, and strong management. Key players include Paxos (PYUSD, BUSD), Brale (USC), and Bridge (B2B API). Reserve management is handled by trusted institutions such as BNY Mellon, which safely generates returns by investing in its Blackstone-managed funds. BUIDL now allows a wider range of on-chain projects to earn returns.

- Banks are the gatekeepers of cash withdrawals:

While deposits (fiat to stablecoins) have become easier, withdrawals (stablecoin to fiat) remain challenging as banks have difficulty verifying the source of funds. Banks prefer to use licensed exchanges like Coinbase and Kraken, which conduct KYC/KYB and have similar AML frameworks. While high-profile banks like Standard Chartered are starting to accept withdrawals, small and medium-sized banks like Singapore's DBS Bank are moving fast. B2B services like Bridge aggregate withdrawal channels and manage billions of dollars in trading volume for high-profile clients including SpaceX and the US government.

- Publishers have the final say:

Circle, the leader in compliant stablecoins, relies on Coinbase and is seeking global licenses and partnerships. However, this strategy could be affected as institutions issue their own stablecoins, as its business model is unparalleled - Tether, a company with 100 employees, made $5.2 billion from investing its reserves in the first half of 2024. Banks like JPMorgan Chase have launched JPM Coin for institutional transactions. Payment app Stripe's acquisition of Bridge shows interest in owning a stablecoin stack, not just integrating USDC. PayPal also issued PYUSD to capture reserve returns. Card networks such as Visa and Mastercard are tentatively accepting stablecoins.

Stablecoins improve efficiency in a banked world

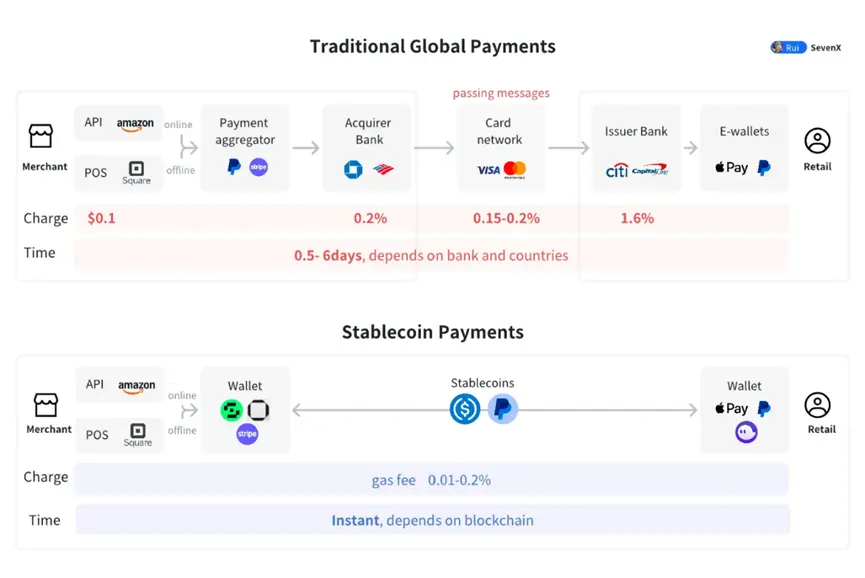

Backed by a foundation of trusted issuers, healthy banking relationships, and distributors, stablecoins have the potential to improve efficiencies across large financial systems, particularly in the payments space.

Traditional systems face efficiency and cost limitations. In-app or intra-bank transfers offer instant settlement, but only within their ecosystem. Interbank payments cost around 2.6% (70% to the issuing bank, 20% to the receiving bank, and 10% to the card network), and settlement takes more than a day. Cross-border transactions cost even more, around 6.25%, and settlement can take up to five days.

Stablecoin payments provide instant peer-to-peer settlement by eliminating intermediaries. This speeds up the flow of funds and reduces capital costs, while providing programmable features such as conditional automatic payments.

- B2B ($120-150 trillion in annual transactions): Banks are in the best position to promote stablecoins. JPMorgan developed JPM Coin on its Quorum chain, and as of October 2023, JPM Coin is used for about $1 billion in transactions per day.

- P2P (Annual transaction volume of $1.8-2 trillion): E-wallets and mobile payment applications are in the best position. PayPal has launched PYUSD, which currently has a market value of $604 million on Ethereum and Solana. PayPal allows end users to register and send PYUSD for free.

- B2C business (annual transaction volume of US$5.5-6 trillion): Stablecoins need to cooperate with POS, bank APIs and card networks. Visa became the first payment network to use USDC to settle transactions in 2021.

Innovators in an underbanked world

Shadow Dollar Economy

Emerging markets are in desperate need of stablecoins due to severe currency devaluation and economic instability. In Turkey, stablecoin purchases account for 3.7% of its GDP. People and businesses are willing to pay a premium over fiat dollars for stablecoins, reaching 30.5% in Argentina and 22.1% in Nigeria. Stablecoins provide access to dollars and financial inclusion.

Tether dominates this space, with a solid 10-year track record. Even in the face of complex banking relationships and redemption crises — Tether admitted in April 2019 that USDT was only 70% backed by reserves — its peg has remained stable. This is because Tether has built a strong shadow dollar economy: in emerging markets, people rarely exchange USDT for fiat, they treat it as dollars, a phenomenon that is particularly evident in regions such as Africa and Latin America to pay employees, invoices, etc. Tether has achieved this without incentives, simply by virtue of its long-term existence and continued utility, which has enhanced its credibility and acceptance. This should be the ultimate goal of every stablecoin.

Get USD

- Remittances: Inequality in remittances slows economic growth. In sub-Saharan Africa, economically active individuals pay an average of 8.5% of total remittances to low- and middle-income countries and developed countries. The situation is even more severe for businesses, where barriers such as high fees, long processing times, bureaucracy and exchange rate risks directly affect the growth and competitiveness of businesses in the region.

- USD Access: Currency volatility cost 17 emerging market countries $1.2 trillion in GDP between 1992 and 2022 — a staggering 9.4% of their combined GDP. Access to USD is critical to local financial development. While many crypto projects are working on onboarding, ZAR is focusing on grassroots “DePIN” approaches. These approaches use local agents to facilitate cash-to-stablecoin transactions in Africa, Latin America, and Pakistan.

- Foreign Exchange: Today, the foreign exchange market has a daily trading volume of over $7.5 trillion. In the global south, individuals often rely on the black market to convert local fiat currencies to US dollars, mainly because the black market exchange rate is more favorable than official channels. Binance P2P is starting to be adopted, but lacks flexibility due to its order book approach. Many projects such as ViFi are building on-chain automated market maker foreign exchange solutions.

- Humanitarian Aid Distribution: Ukrainian war refugees can receive humanitarian aid in the form of USDC, which they can store in digital wallets or cash out locally. In Venezuela, frontline medical workers use USDC to pay for medical supplies during the COVID-19 outbreak as the political and economic crisis deepens.

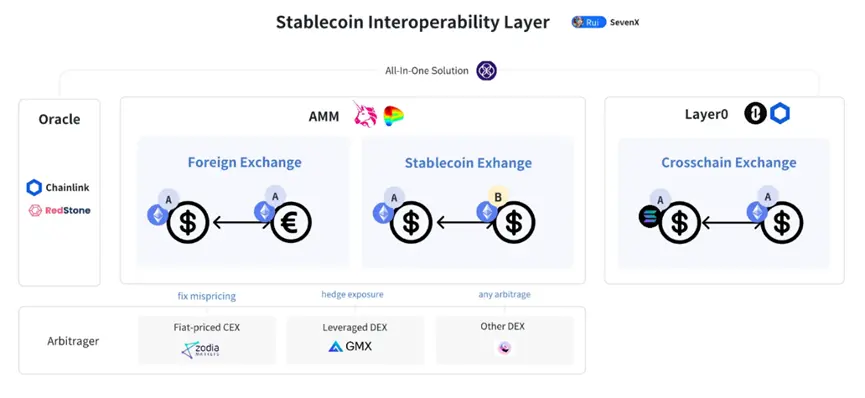

Conclusion: Interweaving

Interoperability

- Different currencies swap:

The traditional FX system is highly inefficient and faces multiple challenges: counterparty settlement risk (CLS is enhanced but cumbersome), the cost of a multi-bank system (six banks are involved when a yen purchase from an Australian bank reaches a dollar office in London), global settlement time zone differences (the Canadian dollar and Japanese yen banking systems overlap for less than 5 hours per day), and limited access to the FX market (retail users pay 100 times more than large institutions). On-chain FX offers significant advantages:

Cost, efficiency, and transparency: Oracles like Redstone and Chainlink provide real-time price quotes. Decentralized exchanges (DEX) provide cost efficiency and transparency, and Uniswap CLMM reduces transaction costs to 0.15-0.25% - about 90% lower than traditional FX. The move from T+2 bank settlement to instant settlement enables arbitrageurs to use a variety of strategies to correct mispricing.

Flexibility and accessibility: On-chain FX enables corporate treasurers and asset managers to access a wide range of products without the need for multiple currency-specific bank accounts. Retail users can use crypto wallets with built-in DEX APIs to access the best FX prices.

Separation of currency from jurisdiction: Transactions no longer require a domestic bank, decoupling them from the underlying jurisdiction. This approach leverages the efficiencies of digitalization while maintaining monetary sovereignty, although there are still drawbacks.

However, challenges remain, including scarcity of non-USD-denominated digital assets, oracle security, support for long-tail currencies, regulation, and unified interfaces with both on- and off-chains. Despite these obstacles, on-chain FX still presents attractive opportunities. For example, Citi is developing a blockchain FX solution under the guidance of the Monetary Authority of Singapore.

- Swap between different stablecoins:

Imagine a world where most companies are issuing their own stablecoins. Stablecoin exchanges present a challenge: using PayPal’s PYUSD to pay JPMorgan’s merchants. While on-chain and off-chain solutions can solve this problem, they lose the efficiency that cryptocurrencies promise. On-chain automated market makers (AMMs) offer the best real-time, low-cost stablecoin-to-stablecoin trading. For example, Uniswap offers multiple such pools with fees as low as 0.01%. However, once billions of funds enter the chain, the security of the smart contracts must be trusted, and there must be deep enough liquidity and instant performance to support real-life activities.

- Interchange between different chains:

The major blockchains have diverse strengths and weaknesses, leading to stablecoins being deployed on multiple chains. This multi-chain approach introduces cross-chain challenges, and bridging presents huge security risks. In my opinion, the best solution is for stablecoins to launch their own layer 0, such as USDC's CCTP, PYUSD's layer 0 integration, and the move we witnessed with USDT recalling bridge-locked tokens, which may lead to similar layer 0 solutions.

In the meantime, several unanswered questions remain:

Would compliant stablecoins hinder “open finance” because they could potentially monitor, freeze, and withdraw funds?

Will compliant stablecoins still avoid offering returns that could be classified as securities, preventing on-chain decentralized finance (DeFi) from benefiting from its massive expansion?

Given Ethereum’s slow speed and its L2’s reliance on a single collator, Solana’s imperfect track record, and the lack of long-term performance records of other popular chains, can any open blockchain really handle huge amounts of money?

Will the separation of currency and jurisdiction introduce more confusion or opportunity?

The financial revolution led by stablecoins is both exciting and unpredictable before us - a new chapter in which freedom and regulation dance in a delicate balance.