Author: Scof, ChainCatcher

Editor: TB, ChainCatcher

After being attacked by 50x leveraged whales exploiting a mechanism vulnerability last time, HyperLiquid got into trouble again.

The method is exactly the same, and the operation is open and transparent, but this time the target is changed to the meme coin $JELLYJELLY, which has far less liquidity than ETH.

Although the platform adjusted its mechanism after the last incident, the results this time show that the protection is still weak. HyperLiquid ultimately paid the price for its negligence and arrogance.

Event Summary

Last night, the decentralized contract platform HyperLiquid encountered a carefully planned on-chain hunting. Around the $JELLYJELLY token, someone used methods such as opening short orders, manipulating the currency price, and inducing system liquidation to jointly hedge the platform's treasury, which attracted widespread attention.

The incident was triggered by a huge short order: the address 0xde9...f5c91 opened a $JELLYJELLY short order worth $4.08 million at a price of $0.0095, investing 3.5 million USDC as a margin, which was actually a "bait" to induce the system to take over.

Subsequently, another address Hc8gN...WRcwq dumped the spot market to create short-term floating profits. Short position holders took the opportunity to withdraw most of their margin, causing the platform to automatically take over the positions and transfer the risk to the vault.

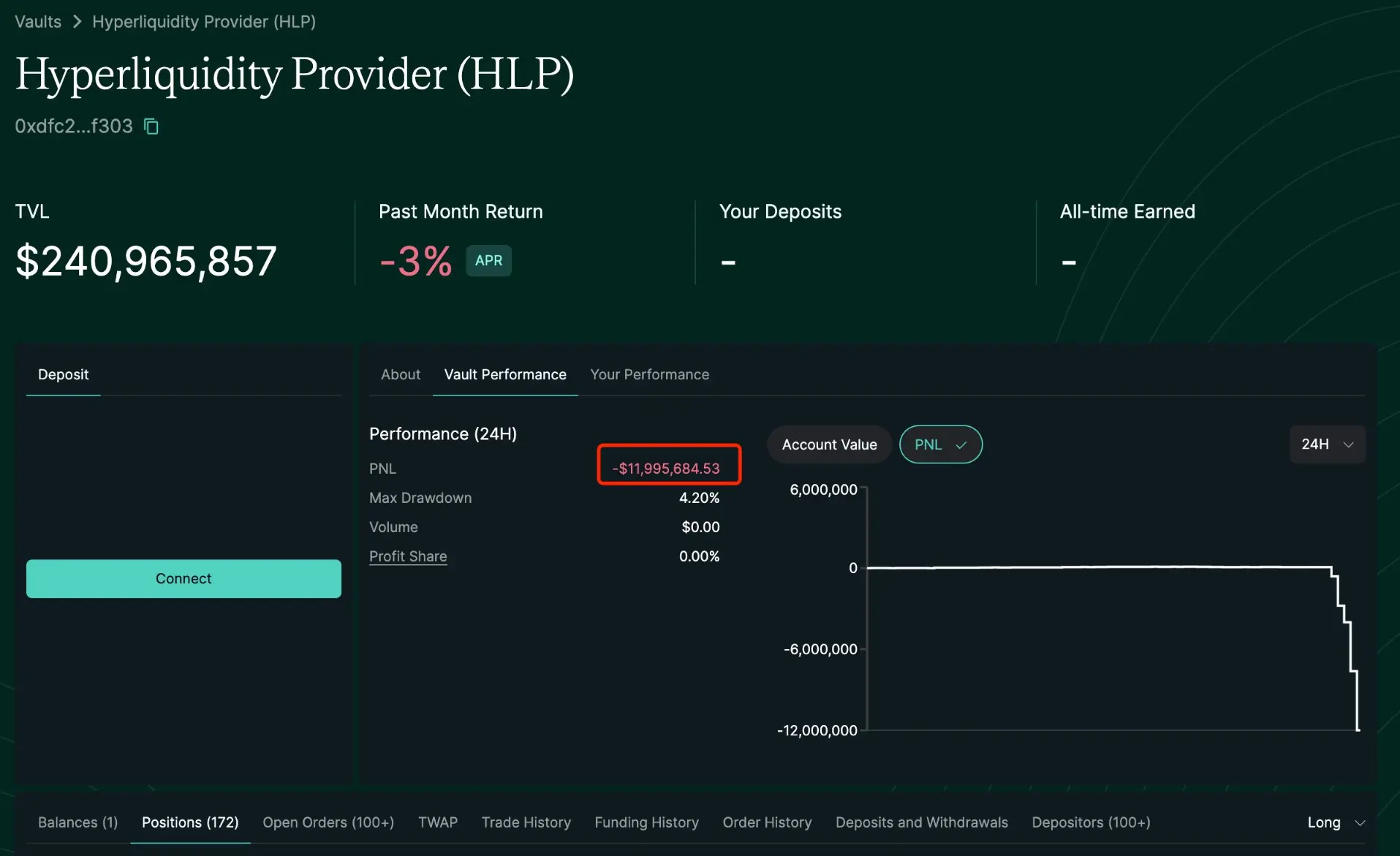

The trader then pulled the price back and bought a large amount of $JELLYJELLY to push up the price of the coin, causing huge losses in the short orders held by the system. At this time, retail investors began to withdraw funds, the pressure on the treasury doubled, and the liquidation price continued to move down. By the peak, the floating loss of the treasury had exceeded 10 million US dollars, and the TVL decreased by about 20 million US dollars. At the same time, according to the analysis of crypto KOL @ai_9684xtpa, if the price of the coin rises to $0.17, the treasury may be forcibly liquidated, facing a maximum loss of 240 million US dollars.

According to monitoring, the pump address once held 120 million $JELLYJELLY (about 5 million US dollars), making it the largest holder on the chain. The funds in this address are suspected to be exhausted, and the price of the coin began to fluctuate violently.

Community Response

Such a thrilling incident quickly sparked widespread discussion on Twitter.

Crypto KOL @thecryptoskanda was the first to speak out, calling for "Binance to list $JELLYJELLY". Soon after, Binance co-founder He Yi retweeted and responded, expressing his approval. A few minutes later, Binance officially announced that it would launch $JELLYJELLY perpetual contracts tomorrow.

At the same time, HyperLiquid officials chose to "pull the plug" and directly delisted $JELLYJELLY, and made a profit of $703,000 by clearing short orders before delisting. Although they said this was a committee vote, the move also caused more controversy.

BitMEX founder Arthur Hayes immediately stated: "HyperLiquid is no longer decentralized," and predicted that HYPE will continue to weaken and eventually return to the starting point.

Andre Cronje, co-founder of Sonic Labs, also criticized HyperLiquid's leverage mechanism in an article on the X platform. He believes that the leverage ratio should not be a fixed function, but should be adjusted dynamically based on available liquidity and actual volatility. For example: small positions can be given 1000 times leverage, while large positions should be limited to 1.2 times. In DeFi, fixed leverage is an extremely dangerous design.

On-chain detective ZachXBT was even more angry and criticized HyperLiquid officials for manipulating prices and turning a blind eye and doing nothing about hackers opening positions on the platform to launder money.

After the incident, according to HyperLiquid's official website, its HLP TVL dropped sharply to $197 million in a short period of time. It is reported that HLP TVL was as high as $240 million before.

For a time, the direction of public opinion completely reversed, and Hyperliquid, which was once hailed by believers as "Binance on the chain", was rapidly losing the trust of the market.

CEX in the guise of DEX?

Although the hunting incident ended with HyperLiquid removing $JELLYJELLY and the platform temporarily stopped bleeding, and the community also achieved a "real-life test" of the mechanism loopholes in a short period of time, the underlying issues are far from being answered.

For example, after the first attack on the mechanism, did the platform truly assess the risk of imbalance between leverage and liquidity? In the face of the liquidation crisis this time, why did it choose to stop losses in a nearly centralized way by delisting trading pairs instead of relying on the preset risk control mechanism?

From another perspective, if the platform claims to adhere to decentralization, then why can it "shut down" at a critical moment with one click? If "survival first" is chosen, then how much of the essential difference between HyperLiquid and CEX is left?

These unanswered questions point to a deeper dilemma: When a decentralized platform faces extreme market shocks, should it let the code speak, or should the backend team make the final decision?

As a user, I believe that on-chain transactions will eventually be the future, but whether HyperLiquid can reach that point is far from an answer. Maybe it is a test product, maybe it will survive and become a new standard. But today, its decentralized narrative is already on the edge of a cliff.