By Hedy Bi

Planning/ Lola Wang

Produced by OKG Research

On March 24, Bo Hines, executive director of US President Trump's Digital Asset Advisory Committee, made a highly controversial suggestion - using the proceeds from gold reserves to buy Bitcoin and increase the country's Bitcoin reserves in a "budget neutral" way. Just a few days ago, the International Monetary Fund (IMF) officially included Bitcoin in the global economic statistics system. With Bitcoin being included in the Balance of Payments and International Investment Position Manual (BPM7), central banks and statistical agencies of various countries need to record Bitcoin transactions and positions in the balance of payments and investment position reports. This move is not only a formal recognition of Bitcoin's influence in the international financial system, but also means that it is gradually evolving from a speculative asset to a more institutionalized financial instrument. From an international level, Bitcoin can become a country's foreign exchange reserve option from March 20.

However, back to the US proposal, the most intriguing part is that the US proposes to exchange gold, which is regarded as the "ultimate safe-haven asset" by the market, for Bitcoin. This proposal itself raises a fundamental question: Is gold really still an undisputed safe-haven asset? If the answer is yes, then from the era of gold coins in ancient Greece and Rome to the present, which has been dozens of centuries, why has no company adopted a radical model similar to Strategy (formerly MicroStrategy) in the Bitcoin market to increase its gold holdings for a long time? As policymakers around the world re-examine the position of this emerging asset in the financial system, the United States has taken the lead in expressing its attitude. Can Bitcoin become the first shot in the financial paradigm shift?

OKG Research will launch a special topic "Trump Economics" in 2025, and will continue to track the impact of Trump 2.0 on the crypto industry and the global market. This article will start with the comparison between Bitcoin and gold to analyze the deep meaning of this intriguing proposal from the United States.

What the United States sells is not real gold?

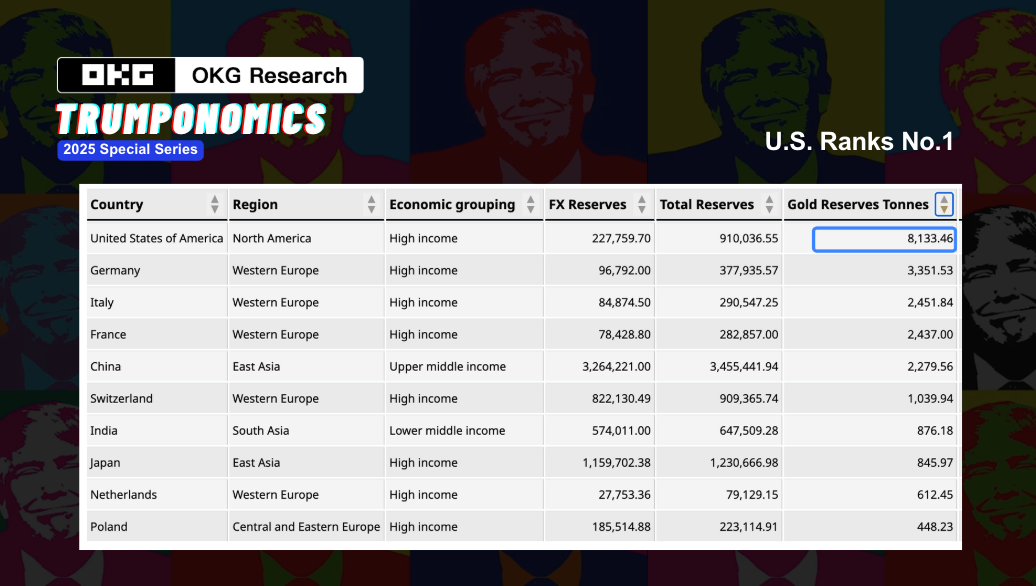

The United States has been ranked first in the world for 70 years with its official gold reserves of 8,133.5 tons. But a noteworthy fact is that this gold has not been circulated in the market for a long time, but stored in the Kentucky Gold Reserve, Denver, New York Federal Reserve and other places. Since the "Nixon Shock" in 1971 ended the Bretton Woods system, the US gold reserves are no longer used to support the US dollar, but as a strategic reserve asset, and are generally not sold directly.

Therefore, if the United States wants to use its "surplus gold reserves" to purchase Bitcoin, the most likely way is to use gold-related financial instruments rather than selling physical gold.

Historically, the U.S. Treasury has been able to create dollar liquidity out of thin air by adjusting the book value of gold without increasing actual gold reserves. This method is essentially an asset "revaluation" operation, and in fact, it can also be seen as an alternative debt monetization.

Currently, the U.S. Treasury has fixed the book value of gold on its balance sheet at $42.22 per ounce, which is much lower than the current market price of gold, which is $2,200 per ounce. If Congress approves an increase in the book price of gold, the book value of the Treasury's gold reserves will increase significantly. Based on this new price, the Treasury can apply for more gold certificates from the Federal Reserve, and the Federal Reserve will provide the Treasury with corresponding new dollars.

This means that the United States can implement a "stealth dollar devaluation" by adjusting the book value of gold without consulting other countries, while creating large-scale fiscal revenue. These additional US dollar funds can be used to purchase Bitcoin, further increasing the US Bitcoin reserves. The fiscal revenue generated by the gold revaluation not only provides financial support for Bitcoin purchases, but may also drive increased demand for Bitcoin in a broader financial context. Stephen Ira Miran, an economic adviser to the Trump 2.0 administration, cited the "Triffin Dilemma" and pointed out that the dollar's status as a global reserve currency has exposed the United States to a long-term trade deficit, and the revaluation of gold will help break this vicious cycle and avoid a surge in interest rates. Bitcoin will benefit from this adjustment without releasing too much liquidity.

However, this approach can ostensibly encourage other institutions and investors to follow suit, thereby attracting more liquidity into the Bitcoin market. However, it cannot be ignored that if the market determines that the loss of the dollar's credibility is a long-term trend, the global asset pricing system may change, and Bitcoin's price discovery mechanism may become more uncertain.

The gold market has never been free

If the U.S. Treasury Department revalues gold and uses the surplus "book value" to exchange for U.S. dollars to purchase Bitcoin, the Bitcoin market may usher in a short-term frenzy, but at the same time face the risks of tightening regulation and liquidity control, just as gold entered the "free pricing" era due to the collapse of the Bretton Woods system - price fluctuations with coexistence of opportunities and uncertainties.

But the gold market has never been truly free.

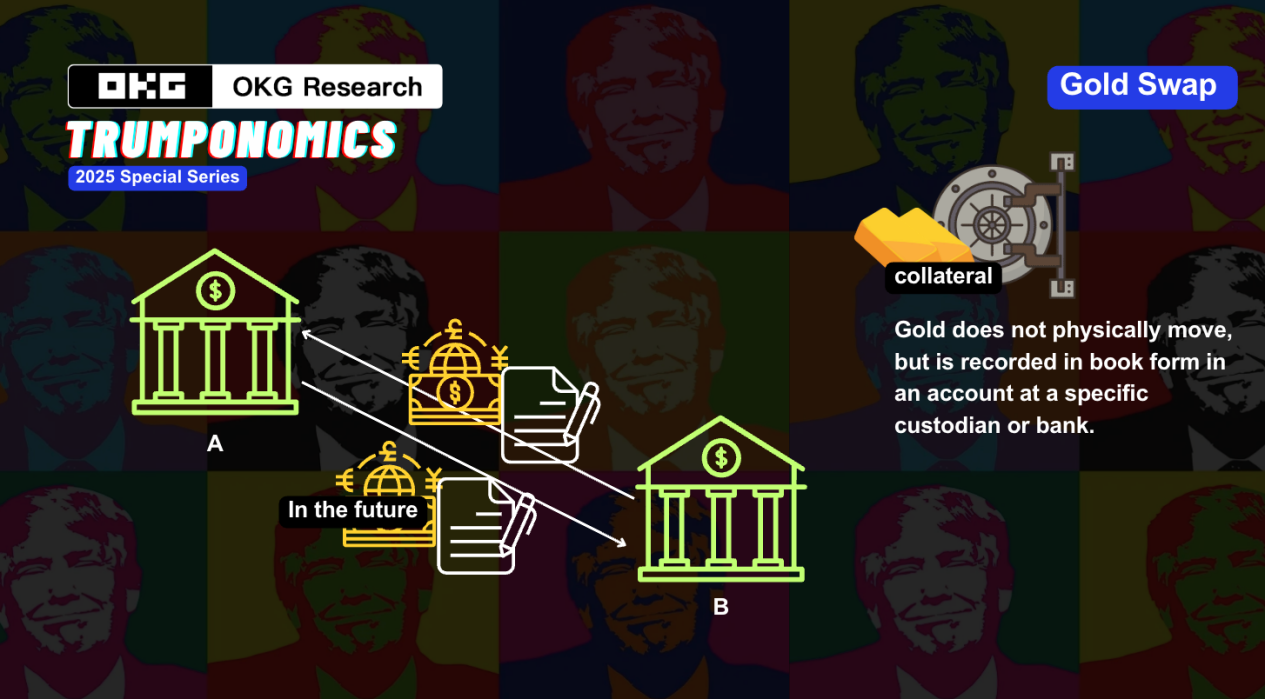

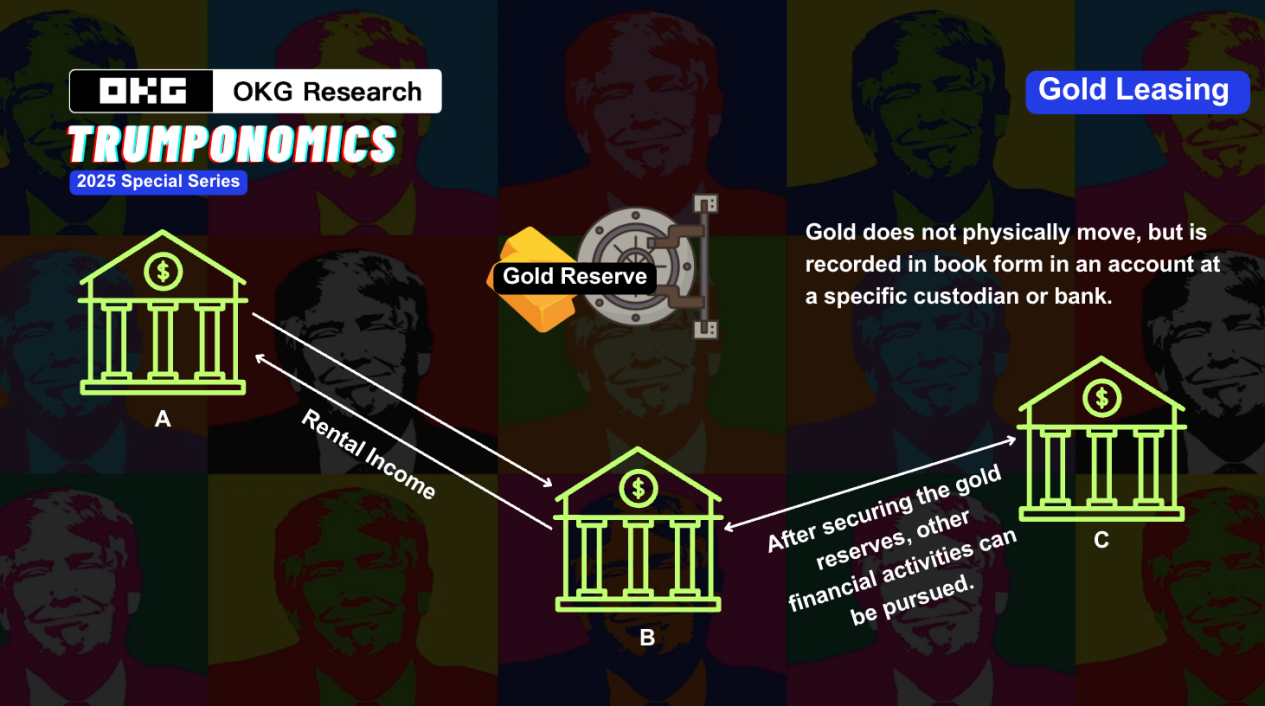

Historically, in addition to being a safe-haven asset, gold also plays the role of a "shadow lever" in the monetary system. There are many examples of using gold for geopolitical games. One of the most famous cases is the "Gold Gate Incident" in the 1970s. During that period, the international credibility of the US dollar was hit by the Vietnam War and other internal and external factors. In order to stabilize the global market's confidence in the US dollar, the United States protected the US dollar by raising the relative price of gold. In addition, in the 1980s, the Reagan administration indirectly intervened in market prices through the "Gold Swap" operation; in the 2000s, the Federal Reserve released liquidity through the gold leasing market to maintain the strong position of the US dollar.

In addition, the credit of gold is not unbreakable. The data of 8,133.5 tons has never been independently audited for decades. Whether the gold in Fort Knox (Knox Vault, located in Kentucky) is intact has always been a hotly debated "black box" issue in the market. More importantly, although the US government does not sell gold directly, it may manipulate its value through financial derivatives such as the "book adjustment" mentioned above to implement shadow monetary policy operations.

The deeper question is, if gold is revalued to release dollar liquidity and Bitcoin becomes a dollar hedge, how will the market redefine credit? Will Bitcoin really become "digital gold" or will it be absorbed and re-controlled by the dollar system like gold?

Will Bitcoin become part of the US shadow monetary policy play?

If Bitcoin may be heading towards a fate similar to gold being absorbed and controlled by the US dollar system, as the United States' interest in holding Bitcoin increases, the market may enter a stage where "Bitcoin becomes a shadow asset" - the official recognizes the value of Bitcoin, but limits its direct impact on the existing system through policies and financial instruments.

Suppose the US government includes Bitcoin in its strategic assets and starts hoarding Bitcoin. As a decentralized asset, unlike traditional gold, the government cannot directly control the supply or price of Bitcoin. However, the government can indirectly influence the price and market sentiment of Bitcoin by conducting market operations through shadow institutions (such as financial instruments such as Bitcoin ETFs or Bitcoin Trust Funds).

These shadow institutions can take advantage of the liquidity and volatility of the Bitcoin market to put a large number of Bitcoins into a "hoarding" state, hoping to release these Bitcoins at a specific time, thereby affecting market supply and demand and price trends. This operation is similar to the "gold swap" and "gold leasing" in the gold market, which does not involve actual Bitcoin transactions, but achieves its purpose through financial instruments and market strategies.

Not to mention the "bubble" in gold derivatives or the real existence of gold: in 2011, some analysts estimated that the ratio of paper gold to physical gold on COMEX could be as high as 100:1. Or the 7-year-long gold repatriation in Germany in 2013, which led to speculation that the Federal Reserve might not have enough physical gold, or that some of the gold had been leased or pledged.

But will Bitcoin repeat the same mistake? Judging from the current development trend of blockchain technology, the answer may be no.

- Gold’s “Black Box” vs. Bitcoin’s Transparency

Bitcoin is not a "black box" operation, and all transactions can be traced on the chain. The decentralized nature of Bitcoin makes it superior to gold in terms of transparency and auditability. As a native asset on the blockchain, all Bitcoin transactions are publicly auditable, and anyone can track the circulation of Bitcoin through on-chain data tools (such as OKX Explorer).

In addition, the Bitcoin network is composed of decentralized independent nodes, each of which holds a complete transaction ledger and jointly verifies transactions. A single institution or country cannot tamper with or manipulate Bitcoin transaction data. Bitcoin does not need to rely on third-party institutions for audits. According to the on-chain data of OKX Explorer, the total holdings of whale wallets (1000+ BTC) remain at 30% to 35%, or 6 million to 7 million BTC. This alone is higher than the current centralized exchange hot wallet Bitcoin storage and institutional custody and ETF ratios. The capital flow of Bitcoin wallets mainly stored on the chain is completely public and globally queryable.

Real-time efficiency is much higher than the gold reserve reports updated on a quarterly or annual basis by most countries, and there will be no more situations like the United States lost seven gold audit reports in Fort Knox. Due to the lag in reserve reports, the market's response to these changes is often delayed.

- Financial run risk VS. Bitcoin's risk resistance

One of the problems of the traditional financial system is the centralized management model of banks and financial institutions, which brings systemic risks. For example, during the 2008 financial crisis, the collapse of Lehman Brothers triggered a chain reaction, and the bankruptcy of Silicon Valley Bank (SVB) in 2023 once again made the market aware of the fragility of the banking system. When there is a liquidity panic in the market, banks may face a large-scale run, and the traditional financial system relies on government emergency bailouts and the Federal Reserve's monetary policy intervention to maintain stability.

Even for Bitcoin stored in centralized exchanges, there are technical ways to prove the actual storage situation of centralized exchanges. OKX officially launched its PoR program (Proof of Reserves, PoR) on November 23, 2022, and used it as a core tool for transparency and user protection. Excess PoR (i.e. PoR greater than 100%) means that the assets held by the exchange or custodian not only cover all user deposits, but also reserve a certain percentage of funds. This excess portion can act as a safety buffer to ensure that even in the event of extreme market fluctuations or unexpected losses of some assets, the institution still has sufficient reserves to meet the withdrawal needs of all users. There will be no "partial reserve" model similar to the traditional banking system. In contrast, the bank reserve rate in the traditional financial system is usually far below 100%. Once a crisis of trust breaks out, banks will face serious liquidity problems.

The US strategy of revaluing gold and creating "new" dollars in this way, and then using these funds to buy Bitcoin, is not only a shadow currency operation, but also exposes the fragility of the global financial system. Whether Bitcoin can truly become an independent and free "digital gold" in this process, rather than just an appendage of the US financial system, we have not yet known. But from a technical perspective, both the real-time queryable transactions on the chain and the PoR of centralized institutions provide a new solution for the traditional financial system. The proposal to exchange gold for Bitcoin has opened up a profound dialogue about the future financial system.