Discussion on Ethereum engine refactoring;

Ethena chooses the Arbitrum camp to launch its chain;

Unichain, MakerDAO and other old DeFi are all moving;

Thoughts on DeFi in the past week.

1/ Let’s talk about ETH first. Vitalik Buterin proposed to use RISC-V to replace EVM as the long-term execution layer.

Try to explain it in as simple a way as possible:

(1) It can be roughly understood as changing the engine, the goal is to improve efficiency

(2) Coping with the massive computing consumption that may be faced in the future

(3) Breaking through the insurmountable performance ceiling under the EVM framework

(4) This change only occurs in the underlying execution engine

(5) Will not change Ethereum’s account model, contract calling method, etc.

(6) Users and developers do not need to change the way they interact with smart contracts when using Ethereum

In summary, Vitalik believes that in the long run, the bottleneck of Ethereum's execution layer will eventually face the problem that the execution layer itself is difficult to verify or requires special hardware to run (huge computing resource consumption), and the expansion will be limited. Using RISC-V is a solution to this problem. As for why RISC-V is better, a superficial understanding is that RISC-V represents a general and efficient computing model, and its hardware and software ecosystem is more mature. It is still in the discussion stage. If this change is really implemented, it will not be small, and the cycle is estimated to be a few years later.

2/ Ethena launches the chain

I was quite surprised that Converge chose the Arbitrum camp, because there are many good players such as Unichain and Base on OP Superchain, and Arbitrum is obviously at a disadvantage in the camp. Although Arbitrum Orbit and OP Superchain are both based on L2 expansion solutions, there are still some differences in design:

(1) Orbit allows developers to create dedicated Rollup or AnyTrust chains: they can be directly anchored to Ethereum as L2 or to Arbitrum as L3.

(2) The vision of OP Superchain is a network consisting of multiple parallel L2s. These L2s (called OP Chains) are all built on the shared OP Stack standard code base.

In a loose sense, Orbit is vertical expansion, while Superchain is horizontal expansion. The two have different views on modularity and flexibility. Orbit advocates openness. For example, the DA of the Orbit chain can choose to publish data directly on Ethereum (Rollup method), and the Data Availability Committee (DAC) maintains the data (AnyTrust method), or it can be integrated into external data availability networks such as Celestia. Superchain focuses on providing an EVM execution environment equivalent to Ethereum. It emphasizes consistency with Ethereum and multi-chain standardization, and modular changes need to be made with caution.

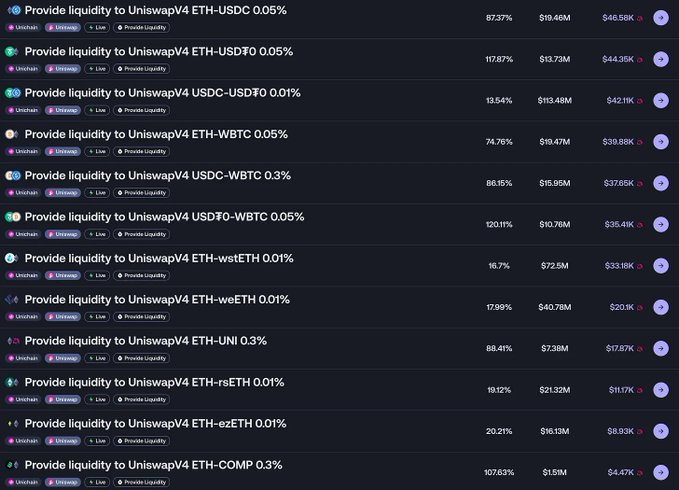

3/ Unichain Liquidity Mining

The income is considerable, but you need to control the range yourself. Mining in the entire range has little presence (the APR on Merkl is inaccurate, and you need to calculate it yourself based on the amount of funds and the range). Compared with the previous version of liquidity mining, the threshold and difficulty are higher. Newcomers are not very enthusiastic about this, and people who play memes don’t know how to play. The current target audience is still old miners. In fact, for old miners, the income is also very attractive without newcomers snatching it. They curse with their mouths but their bodies are very honest. They all play their own games. It is a bit difficult to make DeFi popular by relying on this.

4/ Ripple’s stablecoin RLUSD has entered the mainstream DeFi protocol

(1) Aave has added RLUSD to V3

(2) Curve Pool has deployed 53M liquidity

Stablecoins are really hot this year, and it seems that there is a place for this track in every cycle. You can always find an angle. When there is non-compliance, algorithmic stablecoins perform well, and when the compliance environment is good, the big brothers also come out.

5/Optimism launches SuperStacks event to prepare for the upcoming Superchain interoperability feature

(1) April 16 to June 30, 2025

(2) Encourage users to participate in DeFi on Superchain and earn XP

(3) Protocols can also add their own incentives

(4) OP officials said there would be no airdrop, it was just a social experiment

If you are interested in Superchain, you can participate. For example, you can also get XP by mining on Unichain. I don’t recommend mining deliberately. I have always been paying attention to the interoperability of Superchain and waiting to see what changes it will bring after it is officially launched.

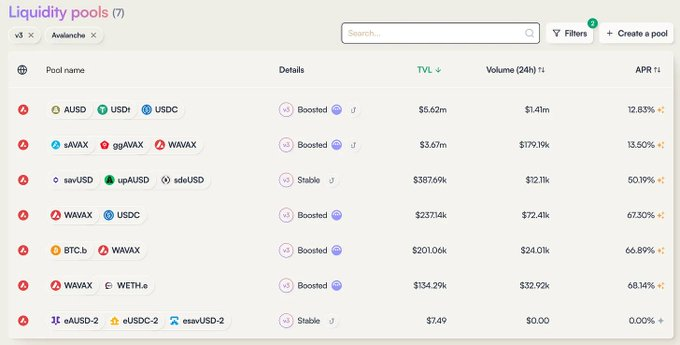

6/BalancerV3 is launched on Avalanche, accompanied by $AVAX incentives

The rewards are OK, but the capacity is average. BAL was previously delisted by Binance, but the protocol is still actively working, including cooperation with the ecosystem and updating and iterating. This old DeFi has not become a leader like Uniswap and Aave, and it does not have the coin issuance bonus of the new DeFi, so it is very difficult to survive. We can only hope for a big explosion on the chain.

7/ Circle launches CPN network, targeting the global payment market

A compliant, seamless and programmable framework that brings together financial institutions to coordinate global payments through fiat currencies, USDC and other payment stablecoins. The network is designed to overcome the infrastructure barriers that stablecoins face in mainstream payments, such as unclear compliance requirements, technical complexity, and issues with secure storage of digital cash.

The first thing to solve is the cross-border payment problem, replacing the traditional slow and expensive payment environment. I think I knew Ripple before, but I am not very familiar with it. At the same time, it provides programmability, which is a good thing and promotes the popularization of blockchain. If every country has a stable currency on the chain, the situation will be different. In fact, it is also promoting more countries to issue compliant stable currencies.

8/ "Bridge" war

(1) GMX selects LayerZero as the information transmission bridge for multi-chain expansion plan

(2) a16z crypto purchased 55M worth of LayerZero tokens, locked for three years

(3) Wormhole releases future planning roadmap

Some thoughts:

This track has a very rigid demand, but it is also very crowded. From the perspective of making money, most of it relies on transaction fees, which will become more and more competitive. This is a good thing for users because the fees will be relatively cheap. From the perspective of protocol integration, what needs to be considered is stability and security.

These giants all have super high valuations, and it is difficult to design an economic model. From this perspective, this kind of business is more suitable to be done on a separate chain, or to imitate this mechanism and incorporate it into the token model of the PoS chain.

9/ Spark (MakerDAO) deployed 50M funds to Maple

It is worth noting that this is the first time Spark has deployed funds in the non-U.S. Treasury bond sector, but there is a limit of US$100 million.

Who is Maple?

Maple focuses on connecting on-chain and off-chain to provide unsecured lending. Its main products include the main platform Maple Finance and the derivative platform Syrup:

(1) Maple’s clients are both qualified investors and institutions

(2) Syrup’s clients use SyrupUSDC to expand on-chain user deposits

There is a key role in Maple:

Pool Delegates: Pool Delegates are usually reputable institutions or trading firms that manage the loan pool. They are the core managers in the Maple ecosystem and their responsibilities include:

- Conduct credit assessment on borrowers and decide whether to approve loans

- Set loan terms (such as interest rate, term, etc.)

- Monitor loan execution and repayment

- Responsible for recovering assets if the borrower defaults

It is obvious that the key to the operation of the protocol basically depends on Pool Delegates.

Maple is an old project. It was not popular in the last cycle, mainly because its business model is to absorb deposits on the chain and then lend to off-chain customers without collateral in a centralized way. This concept was not easy to accept in the past. However, it has been gradually accepted in this cycle due to changes in the compliance environment and user thinking. However, I personally feel that USDS's choice of Maple to deploy funds is still a relatively risky move.