Author: Poopman

Compiled by: TechFlow

Another RWA stablecoin backed by treasury bills? Ugh, this is so boring.

Every time I mention @usualmoney to a friend, this is their reaction.

Today, many stablecoins choose to use treasury bills as collateral because they offer relatively good yields and low risk. For example:

- Tether holds $81 billion in Treasury securities.

- MakerDAO/Sky is heavily invested in Treasuries and has made a tidy profit from them (sorry, I can’t remember the exact figure).

- There are more RWA players like Ondo, Hashnote, Blackrock, and Franklin joining the fray. However, to be honest, most treasury stablecoins operate in much the same way.

Institutions that have passed KYC certification can directly mint stablecoins by depositing real treasury bonds into designated funds. Token issuers then work with management funds to issue the corresponding number of stablecoins.

The yields can vary because these Treasury bills have different maturities, but they don't vary much, usually between 4% and 6%.

So, is there any way to get higher yields and make it more interesting?

question?

A simple and effective way to increase returns is to issue more governance tokens to attract more deposits and total locked value (TVL).

However, these tokens often lack real-world utility and tend to be sold off in large quantities upon launch due to high inflation. Many times, they are merely exit vehicles for users and investors, or the tokens themselves are not closely enough tied to the actual revenue generated by the product.

In many cases, revenue flows directly to the product itself, rather than the governance token. For example, sDAI earns DAI, not $MKR.

Those tokens that do have a connection often use the ve3.3 model to kickstart a positive flywheel effect (hat tip @AerodromeFi, @CurveFinance, @pendle_fi) and if the flywheel works, they can grow exponentially in a bull market. However, when the flywheel stops, the dilution effect can spell trouble.

A new approach is to enhance the utility of the token or reposition it as a L2 token, like @EthenaNetwork / @unichain. But this strategy usually only works for big businesses 🤣.

$Usual has chosen a different approach by allocating 100% of the protocol’s revenue to governance tokens, making those tokens “fundamentally backed by actual dollars.”

At the same time, they control inflation and issuance by adding some PVP elements (such as early vs late, staking vs unstaking) to make it more interesting.

However, what may disappoint you is that $usual is not the high-yield product you imagined, it is more like a safe product (SAFU) that is more interesting than its competitors.

To help you understand better, let’s look at the user flow.

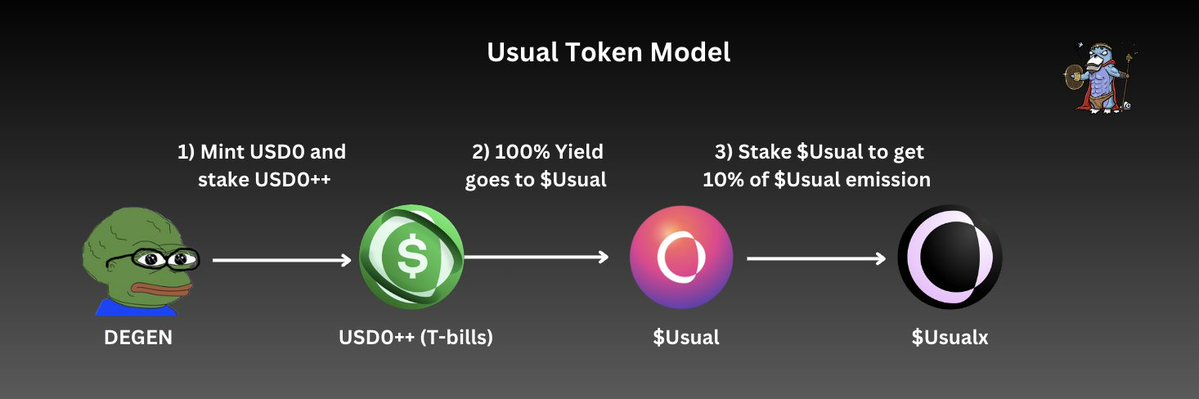

$Usual

$Usual Token Economics and User Flow

Usual money token economics

- First, as a user, I can mint USD0 with stablecoins. If I don’t want to provide liquidity or participate in other yield farming, I can stake USD0 to $USD0++.

- When I stake USD0, my $USD0++ will receive 90% of $Usual rewards, which are $USUAL, not USD0 or USDC. The issuance rate of $Usual depends on the amount of $USD0++ minted and the yield of treasury bills.

- 100% of the treasury yields earned by USD0++ go into the protocol treasury, and the $Usual token is responsible for managing the treasury.

- To get the remaining 10% of $Usual rewards, I can stake $Usual to $Usualx. This 10% is automatically distributed to stakers every time new $Usual is minted. In addition, $Usualx holders have the right to participate in voting and other governance decisions, such as adjusting the issuance rate.

Throughout the user flow, we can see that the governance token ($Usual) actually captures all of the revenue from the RWA product itself, while stablecoin holders and stakers are incentivized through yield-backed rewards.

Since Usual is a RWA product, it is difficult to get a very high annual percentage yield (APY) or annual percentage rate (APR) because the yield is closely related to the actual interest rate and the supply of USD0++.

More details will be introduced in the following paragraphs.

Token Utility at a Glance:

- The tokens represent the entire proceeds of the protocol’s revenue.

- By staking, you can obtain 10% of the total issuance of $Usual and have voting rights to influence the direction of issuance.

- Participate in governance decisions regarding treasury management (e.g. reinvestment, etc.).

- Burn $Usual to unstake LST USD0++ early.

The fun of the distribution mechanism

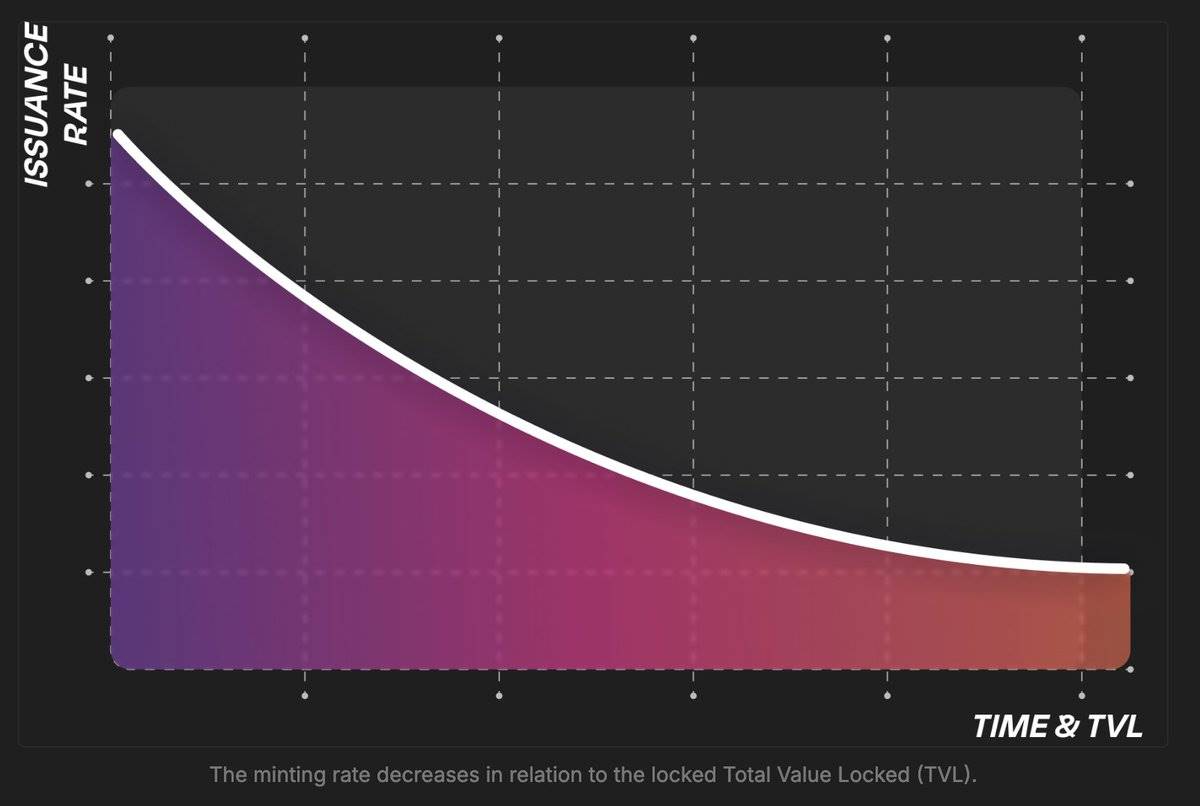

- $Usual issuance is adjusted based on a dynamic supply, which means:

- As TVL grows, the issuance of $Usual decreases.

- When TVL decreases, the issuance of $Usual increases.

question:

So, poopman, are you saying that Usual doesn't encourage deposits when TVL is high?

answer:

No, not at all. When TVL is higher, Usual actually earns more from the increased treasury. Therefore, as the treasury grows, the value of $Usual should be higher.

Conversely, when TVL is lower, $Usual issuance increases because the treasury earns less and they need to pay more compensation. High issuance helps Usual attract more TVL to the platform.

Additionally, to prevent excessive inflation of $Usual:

- The issuance rate will be adjusted according to the interest rate.

- A maximum issuance threshold is set (determined by the DAO).

This is because Usual wants to ensure that the growth rate of the token does not exceed the growth rate of the treasury in order to maintain the value of $Usual and conform to the concept of "project growth = token value growth". Of course, the DAO can make adjustments as needed.

For early and late participants:

In this model, early adopters benefit the most because they receive the most $Usual at a higher price when TVL is high.

For later participants, although they received fewer tokens, they did not suffer any substantial loss except for the opportunity cost, because they were still able to obtain benefits.

Simply put, $Usual is a token that represents the revenue generated by Usual.

$Usual adds some fun by introducing a PVP element, where users can earn 10% of other people’s $Usual issuance through staking, while early participants can get more benefits from latecomers.

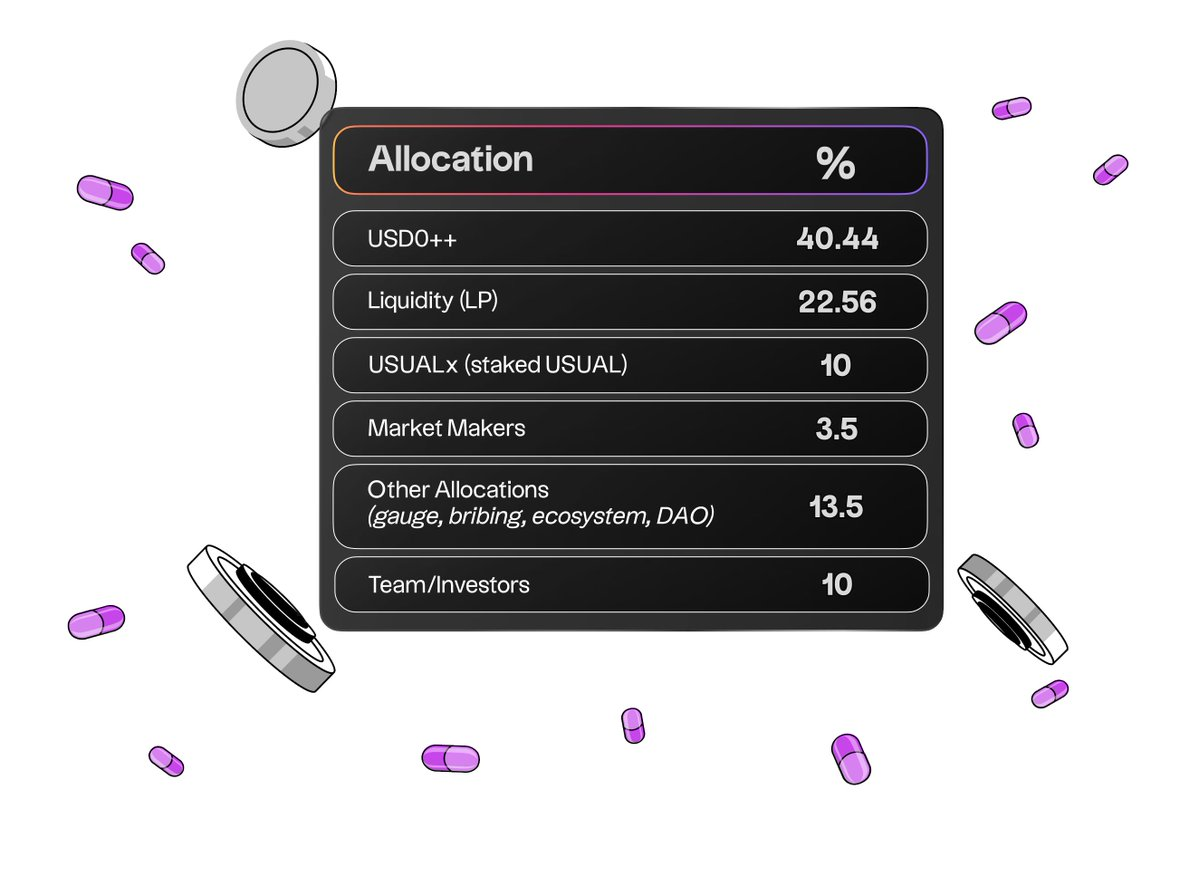

Token Allocation:

$Usual allocations are community-focused:

- 73% of tokens are used for public and liquidity provision

- 13.5% allocated to MM/Team and investors

- 13.5% for DAO/bribing/voting, etc.

Great to see DeFi designed this way putting the community first. Well done to the team.

What are the issues that need attention?

The $Usual token is interesting, has significant and meaningful value, and places a strong emphasis on controlling inflation. However, there are some risks that Usual and its users may want to be aware of.

USD0++ liquidity issues and decoupling risks

There are currently more than $320 million USD0 staked in USD0++, while the USD0 liquidity on Curve is only about $29 million. In other words, less than 10% of the USD0++ available for exit in the market, and an imbalance in the pool may lead to decoupling in the event of a large-scale exit. Although this ratio is not too bad (only 2-3% liquidity in the worst case), it is a risk we must consider when entering the TGE window, as short-term investors may choose to exit.

Earnings competitiveness in a bull market

It may sound naive, but during bull markets, attractive returns usually come from the crypto assets themselves (such as ETH, SOL, etc.), rather than stable real-world assets like treasury bills.

In contrast, I expect stablecoins like sUSDe to earn strong returns in rising markets, attracting more TVL than Usual, as their yields can reach 20-40% or more. In this case, without new products to enhance the yield of USD0, Usual's growth may stagnate.

Nevertheless, I think about 80% of people in the DeFi community understand the risks that USDe holders need to bear. As a "conservative stablecoin", Usual can provide a better and more resilient option for those seeking stability.

The DAO Problem: Low Participation

Low participation has always been a common problem in DAOs. Since Usual is centered around a DAO, it is very important to ensure sufficient and effective participation. Here are some thoughts:

- Delegation may be a solution, but DAO decisions are not always optimal. Crowd wisdom is often used to support the construction of DAOs, but judging by the results of Arbitrum DAO, not everyone has the understanding or vision to build a meaningful future for the project.

- Most participants are self-directed and tend to vote only for matters that are beneficial to themselves. This may lead to problems such as monopoly or uneven distribution of rewards.

Therefore, there are risks in giving too much decision-making power to the DAO, which may ultimately lead to undesirable results.

in conclusion:

- The token economics model is robust and interesting. The governance token does have real value as it is backed by revenue.

- $Usual stakers can get 10% of all minting as rewards, which incentivizes users to stake. This model injects fresh vitality into the RWA stablecoin field, and I think it is the right approach.

- Excellent performance in controlling inflation. Minting amount is strictly limited by the available supply of USD0++ and real-world interest rates, ensuring that inflation does not dilute the value of $Usual.

However, the disadvantage is that you cannot expect extremely high annual returns, which may be a disadvantage compared to other products in a bull market.

- Liquidity issues. Currently on Curve, the liquidity of USD0 and USD0++ is less than 10%. This may pose a risk to liquidity providers during the TGE window, especially during large-scale exits.

However, I believe that most holders are willing to hold on for the long term.