Title: DeFi's Growing Focus on Token Value Accrual

Author: @ManoppoMarco, primitivecrypto investor

Compiled by: zhouzhou, BlockBeats

Editor's note: DeFi protocols are accelerating the accumulation of value for token holders. Protocols such as Aave, Ethena, Hyperliquid and Jupiter are implementing buyback programs, fee switches and new incentive structures. Ethena plans to enable a fee switch to share revenue with stakers, and is currently achieving key goals. Other protocols are also enhancing token value through buybacks, fee allocation and optimized governance.

The following is the original content (for easier reading and understanding, the original content has been reorganized):

If you’ve spent 8-9 figures on growth and haven’t seen at least linear growth in revenue, buybacks aren’t necessarily a bad thing. DeFi protocols are facing increasing pressure to distribute part of their revenue to token holders. Major projects such as Aave, Ethena, and Hyperliquid are already exploring how to introduce value accumulation mechanisms for their native tokens.

The key driver behind this trend? The election of Donald Trump, which ushered in a more friendly regulatory environment for DeFi. Here are the latest updates on the token economics of Aave, Athena, Jupiter, and Hyperliquid, including their buyback plans and fee adjustments.

AAVE

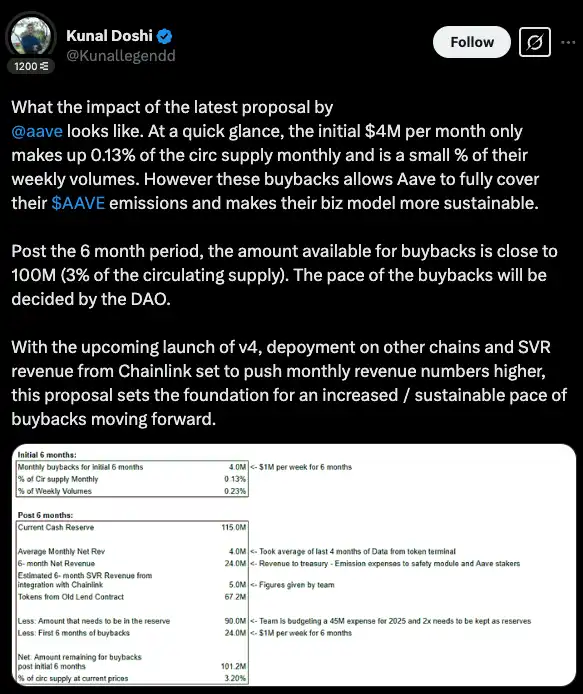

Aave has just launched a major token economics reform that focuses on buybacks, fee distribution, and better incentives for token holders. According to Marc Zeller, founder of the Aave Chan Initiative (ACI), this is one of the most important proposals in Aave’s history.

Buyback & Fee Adjustment

Aave has launched a six-month buyback program, investing $1 million per week (about $4 million per month) to cover the emission of AAVE tokens and improve the sustainability of the protocol. After six months, the buyback pool may reach $100 million (about 3% of the circulating supply), and the specific deployment rhythm will be determined by the DAO.

What’s the goal? Controlling token emission while increasing the strength of Aave’s treasury.

New Fiscal & Governance Initiatives

Aave is setting up the Aave Financial Committee (AFC), which is responsible for treasury fund management and liquidity strategy. In addition, Aave is also completing the transition from LEND tokens and recovering 320,000 AAVE (about $65 million) for future use.

Umbrella: Aave’s new risk management system:

Aave spends $27 million per year on liquidity costs, so it launched the Umbrella system to optimize capital efficiency and reduce risk. The system will be integrated into multiple blockchains, including Ethereum, Avalanche, Arbitrum, Gnosis, and Base.

Anti-GHO: A new reward mechanism for stablecoin holders:

Anti-GHO is a new reward mechanism that will replace the old discount model for GHO holders. Tokens held can be destroyed at a 1:1 ratio to offset GHO debt, or converted to StkGHO, so that the incentive mechanism is directly tied to Aave's revenue. This mechanism is still under development and may be launched as part of the future "Aavenomics Part II" update.

What’s next?

With the release of Aave v4, more on-chain deployments, and additional revenue from Chainlink SVR, this update lays the foundation for larger, more sustainable buybacks in the future.

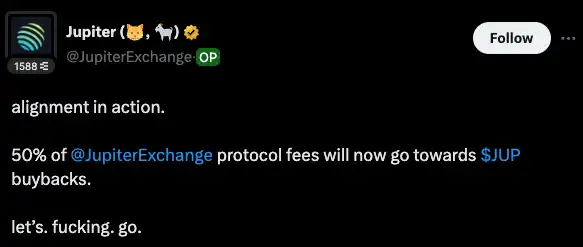

Jupiter

Jupiter has begun to use 50% of its protocol fees to repurchase and lock JUP tokens for three years since February 17, 2025. This move is intended to reduce the circulating supply, enhance long-term stability, and promote user participation in the Solana ecosystem. In February of this year, Jupiter completed its first repurchase, purchasing 48,800 JUPs for $3.33 million. Currently, Jupiter's Litterbox Trust repurchase program has repurchased more than 10 million JUPs (about $6 million).

What’s next?

On an annual basis, Jupiter's $3.33 million buyback is equivalent to an annual buyback volume of more than $35 million. If we use a more aggressive estimate, Jupiter's revenue in 2024 is $102 million, which means the buyback volume could exceed $50 million.

Hyperliquid

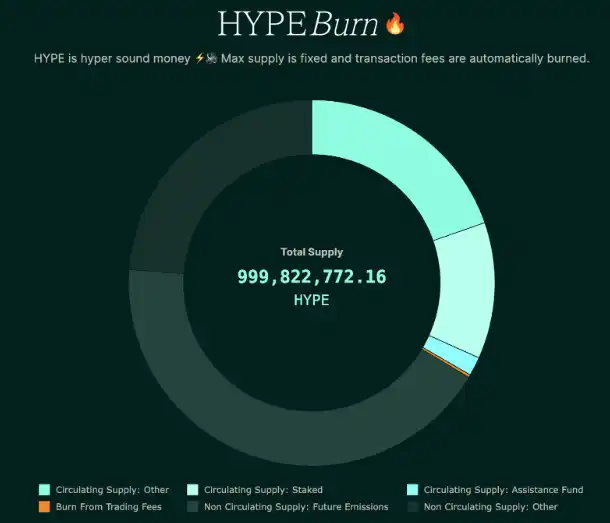

Token Allocation

The total supply of Hyperliquid's native token HYPE is 1 billion, and there is no financing and no investor allocation. The specific allocation is as follows:

31.0%: Airdropped to early users (fully circulated)

38.888%: Reserved for future emissions and community rewards

23.8%: Team allocation, locked for 1 year, most of which will be unlocked in 2027-2028

6.0%: Hyper Foundation

0.3%: Community funding

0.012%: HIP-2

The team and community token ratio is 3:7, with the largest non-team holder being the Assistance Fund (AF), which holds 1.16% of the total supply and 3.74% of the circulating supply.

Revenue Model & Buyback Mechanism

Hyperliquid's main sources of income include transaction fees (spot + derivatives) and HIP-1 auction fees. Since Hyperliquid L1 currently does not charge gas fees, gas-related income is not included for the time being.

Income Distribution

46% of perpetual contract transaction fees are allocated to HLP holders (supply-side rewards)

54% used to repurchase HYPE through Assistance Fund (AF)

In addition, HIP-1 auction fees and spot transaction fees (USDC portion) are currently all used for HYPE token repurchases.

Dual deflation mechanism

· Buyback: AF uses part of the revenue to buy back HYPE tokens, but they will not be destroyed, but held by AF

·destroy:

1. All HYPE-denominated spot transaction fees (such as HYPE-USDC trading pairs) will be directly destroyed

2. After the HyperEVM mainnet is launched, all Gas fees will be paid in HYPE and destroyed.

Buyback Impact & Pledge Mechanism

According to publicly available Hyperliquid transaction fee data, as of March 2025, AF will repurchase 54% of its perpetual contract revenue, and is expected to repurchase about 2.5 million HYPE per month, worth about $35 million. HYPE staking will be launched on December 30, 2024, using a PoS reward mechanism (similar to Ethereum), with an annualized yield of about 2.5%. Currently, 30 million HYPE has been staked (excluding 300 million tokens held by the team/foundation).

Future Outlook

Hyperliquid may introduce a fee sharing model to allocate part of the on-chain transaction fees directly to HYPE holders to create a more sustainable incentive system. However, some people believe that the current model can form a stronger flywheel effect in both market ups and downs.

Hyperliquid's revenue mainly comes from transaction fees and HIP-1 auction fees, and may expand revenue sources such as HyperEVM transactions in the future. Currently, in addition to being used for repurchases and incentives, part of the fees can also be used for:

Distributed to HYPE holders based on holdings or pledged amounts.

Reward long-term stakers and drive deeper community participation.

Deposit into the community treasury, and let the governance decide how to use it.

Possible allocation modes:

Direct fee sharing:

Part of the transaction fees is converted into USDC or HYPE and distributed to coin holders regularly (similar to dividends).

Staking Enhanced Rewards:

Only users who pledge HYPE can receive a share to encourage long-term holding.

· Hybrid Mode:

Combine transaction fee distribution + HYPE repurchase to balance price support and coin holding incentives.

Ethena

Ethena Labs is now among the top five DeFi protocols by TVL, with annual revenue exceeding $300 million. As the protocol grows, Wintermute's proposal for fee distribution has been approved by the Ethena Risk Committee. Currently, 824 million ENA (worth $324 million) is staked, accounting for 5.5% of the total supply, but stakers can only receive point rewards and unclaimed ENA airdrops, and do not enjoy a share of the revenue generated by Ethena.

Ethena fee switch and future plans:

The launch of the fee switch will provide stakers with direct revenue sharing opportunities and enhance the effectiveness of DAO governance through incentive alignment with ENA holders. Ethena's revenue mainly comes from the perpetual contract market funding rate. Currently, 100% of the revenue is distributed to USDe stakers and the reserve fund. In the past three months, the monthly revenue has averaged US$50 million.

Preparation before turning on the fee switch: The Risk Committee set five key indicators to ensure Ethena is in a solid position before sharing revenue.

Current indicator progress:

USDe supply target: 6B – only 9% away from target.

Cumulative revenue: 250M+ – reached 330M USD in January, exceeding the target.

Exchange Integration: Binance/OKX – No timeline yet, but Binance currently holds 4M USDe.

· Reserve Funds ≥ 1% of USDDe supply – $61M in reserves backing 6.1B USDDe.

sUSDe vs sUSDS APY gap ≥ 5% – The gap has narrowed due to the market downturn, but may widen again in the future.

Future Outlook

Ethena is close to reaching its goal, but the fee switch will remain suspended until all metrics are met. During this time, the team will focus on growing USDe supply, securing more exchange integrations, and monitoring market conditions.

Once all conditions are met, ENA stakers can start enjoying revenue sharing.

Summarize

Major DeFi protocols are accelerating their transition to value accumulation for token holders, with Aave, Ethena, Hyperliquid, and Jupiter all implementing buyback programs, fee switches, and new incentive structures to make their tokens more valuable beyond speculation.

This trend reflects the industry’s overall shift toward sustainable token economics, where projects focus more on real income distribution rather than inflationary incentives.

Aave uses its deep reserves to support buybacks and governance improvements, Ethena is committed to providing direct revenue sharing for stakers, Hyperliquid optimizes the buyback and fee distribution model, and Jupiter locks up buyback tokens to stabilize supply.

As the regulatory environment gradually improves and DeFi matures, protocols that successfully align with community incentives will flourish.