Written by: Hedy Bi, Lola Wang | OKG Research

OKG Research has specially planned and launched a series of special topics on "Trump Economics", which deeply analyzes the future trends and core logic of the crypto market as Trump's 2.0 new policies continue to advance.

This article is the fourth in the "Trump Economics" series of special topics specially planned by OKG Research.

In 2025, Trump's "America First" strategy will stimulate domestic economic growth by promoting trade protectionism, promoting industrial repatriation, reforming taxes, and increasing military spending. The focus is on strengthening the independence of the US manufacturing, technology and energy sectors, while improving export competitiveness. The core goal of this series of policies is to promote the recovery of the US economy, while reducing dependence on foreign production and capital, and enhancing the US's dominant position in the global economy.

As these policies continue to advance, especially the massive fiscal spending and deficit issues caused by the promotion of military spending and large-scale infrastructure construction, coupled with the existing pressure on US debt and potential inflation expectations, investors may begin to try different risk hedging assets. Crypto assets have become a fulcrum for "Trump Economics".

Despite the continuous inflow of institutional funds, actual funds cannot bring dopamine to the market because investor expectations have become the main variable determining the market trend. This article is the fourth article in the special topic Trump Economics in 2025 by OKG Research, which explores the current predicament of the crypto market and the market impact of the massive release of liquidity in 2025.

Crypto Markets Struggling to Find Liquidity

Driven by Trump's economics, the US's self-sufficiency and industrial revitalization policies are facing high inflation and high debt pressure. Although the US macro CPI/PPI data from February 12 to 13 did not cause a large market fluctuation, it was because these data were superficial indirect data rather than direct data. For institutional funds, the market is more about digesting previous expectations. The real market benefits appeared in the wave of liquidity release by the Ministry of Finance in early February. This actual operation injected substantial momentum into the market and promoted the rise of risky assets.

Specifically, the inflow of institutional investors is more like the expected landing and the redistribution of existing funds in the market based on this. In the macro report released by OKG Research last weekend, the author proposed that for the market, "limited liquidity" and the "precise reconfiguration" of the market are currently concentrated on Bitcoin, because of the change in the trading behavior of the main holders behind it. Institutional investors tend to hold for a long time and concentrate, so the flow of ETFs rarely overflows to other assets, which is one of the main reasons why the "altcoin season" that investors are looking forward to has not come yet.

However, although the Fed's meeting minutes on February 19 emphasized the stance of not rushing to cut interest rates, this did not cause a significant impact on the U.S. stock market. Through market observation, the expectation of not cutting interest rates for the time being seems to have been digested, or the market has begun to anticipate trading in advance of "pausing or slowing down the balance sheet reduction."

However, it cannot be denied that no matter how the expectations change, they are based on the macroeconomic situation, and expectations do not mean a "big bet" on the macro economy. So far, what we have observed is that the Fed's monetary policy will still face two major pressures. High inflation and high debt levels will make the Fed's monetary policy more cautious , which means that even in the face of slowing economic growth, the Fed may avoid overly loose monetary policy.

A new round of "liquidity manifestation" in the crypto market may have arrived

Although at present, the United States has not implemented large-scale quantitative easing (QE) in 2025 as it did in 2018 and 2020, that is, injecting treasury bonds and government debt assets into the market to stimulate economic growth. However, in the short term, in order to deal with the U.S. debt ceiling issue, TGA has begun to inject liquidity into the market this week.

Historically, whenever the U.S. government faces debt ceiling issues, the market tends to release short-term liquidity (from TGA), which in turn drives up the prices of various assets, especially risky assets. The U.S. Treasury's "Treasury General Account" (TGA) is an important tool for the government to manage daily cash flow. The balance of this account is adjusted according to the government's revenue and expenditure. When facing debt ceiling restrictions, the Treasury Department usually reduces the supply of Treasury bonds and uses the funds in the TGA account to maintain the normal operation of the government.

In fact, changes in TGA balances directly affect the liquidity of the financial market. Every time there is a large-scale release of liquidity, the increase in risk assets, especially crypto assets, will respond. For example, from mid-2020 to the end of 2021 (this stage was superimposed with monetary policy), Bitcoin rose by about 6 times. During this period, the growth of M2 in the United States also reached 40%+, which was the fastest growth period of M2 in 5 years.

During the first half of 2022 to the first half of 2023, the price of Bitcoin during the TGA liquidity release phase showed a certain lag. During this phase, the price of Bitcoin increased by about 100% from the lowest point to the highest point. However, from the beginning of liquidity release to the end of the phase, the overall increase in the price of Bitcoin was about 10%.

According to the latest Goldman Sachs report, the first round of short-term TGA liquidity injection in 2025 will be approximately $150 billion to $250 billion. It is expected to continue until the summer until a new agreement is reached. This is the first round of foreseeable liquidity release. Other institutions have also conducted analysis and believe that the first round is expected to inject a total of about $600 billion in liquidity.

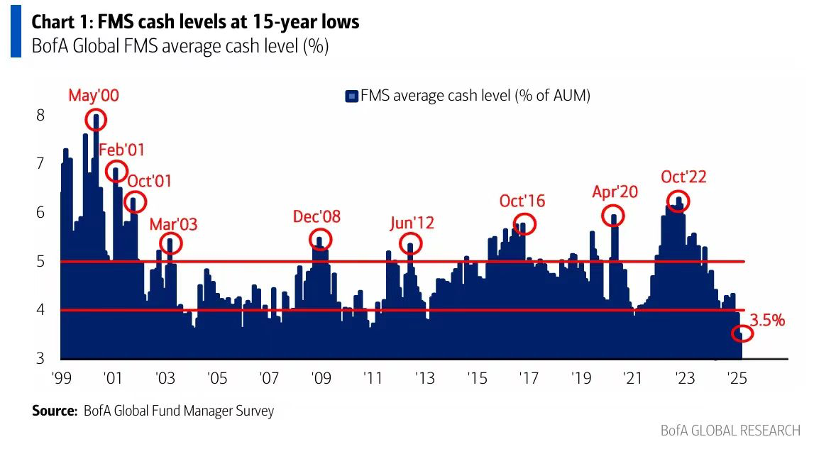

According to the latest macro analysis report from Bank of America (BofA), the cash holdings of global fund managers fell to a low of 3.5% in February 2025, reflecting the increase in investors' risk appetite - they prefer stocks rather than cash and bonds. This increase in risk appetite coincides with the timing of the current TGA liquidity release. In other words, most of this round of short-term liquidity injection is expected to flow into the risky asset market, including crypto assets. The direction of investors' capital flows and their preference for risky assets may further drive the rise of the crypto market.

Not QE, but better than QE?

Under the framework of Trumponomics, the strategy of promoting America First not only relies on trade protectionism and industrial reshoring, but also relies on strong support from fiscal and monetary policies. In order to achieve self-sufficiency and stimulate the domestic economy, the Trump administration prefers to use fiscal tools, such as TGA (Treasury General Account), and when necessary, monetary policy tools to inject liquidity to promote economic growth.

Unlike quantitative easing (QE), a long-term monetary policy tool, TGA's liquidity release is a one-off, short-term operation. By reducing treasury bond issuance and using funds in the TGA account to meet short-term liquidity needs, the government can quickly inject liquidity into the market. Although this injection can drive risk assets up in the short term, due to the strong temporary nature of TGA funds, liquidity may be quickly recovered at a later stage, which may bring about a tightening effect on market liquidity.

In contrast, QE is a means for the Federal Reserve to expand its balance sheet over the long term by purchasing assets (such as Treasury bonds) and continuously inject funds into the market, aiming to stabilize financial markets and stimulate economic growth. The long-term and continuous nature of QE contrasts sharply with the short-term nature of TGA. In order to achieve the goals of industrial revitalization and enhancing competitiveness, the Trump administration needs to use TGA to inject liquidity in the short term, while relying on monetary policy easing measures to support the economy in the long term. However, the short-term liquidity release of TGA may also conflict with the Federal Reserve's monetary tightening direction, which may cause market uncertainty as the government continues to increase debt, thereby affecting the implementation of overall economic policies.

In general, the Trump administration has injected new vitality into the market through the short-term liquidity release of TGA. Although this release is not a long-term monetary easing policy like quantitative easing (QE), it is enough to drive the rise of risky assets such as crypto assets in the short term. For the crypto market, short-term capital inflows are undoubtedly a rare opportunity, but the accompanying liquidity tightening effect and US debt problems still need to be paid attention to. Long-term economic stability still depends on the effective coordination of fiscal and monetary policies under the Trump economics framework. In the next few months, the monetary and fiscal policy tools adopted based on this framework will largely determine the performance of the crypto market.