Author: Thejaswini MA

Compiled by: Block unicorn

Preface

January 2024 feels like a different time. It’s only been eighteen months, but in retrospect it seems so far away. For crypto, it’s like The Bridge on the River Kwai.

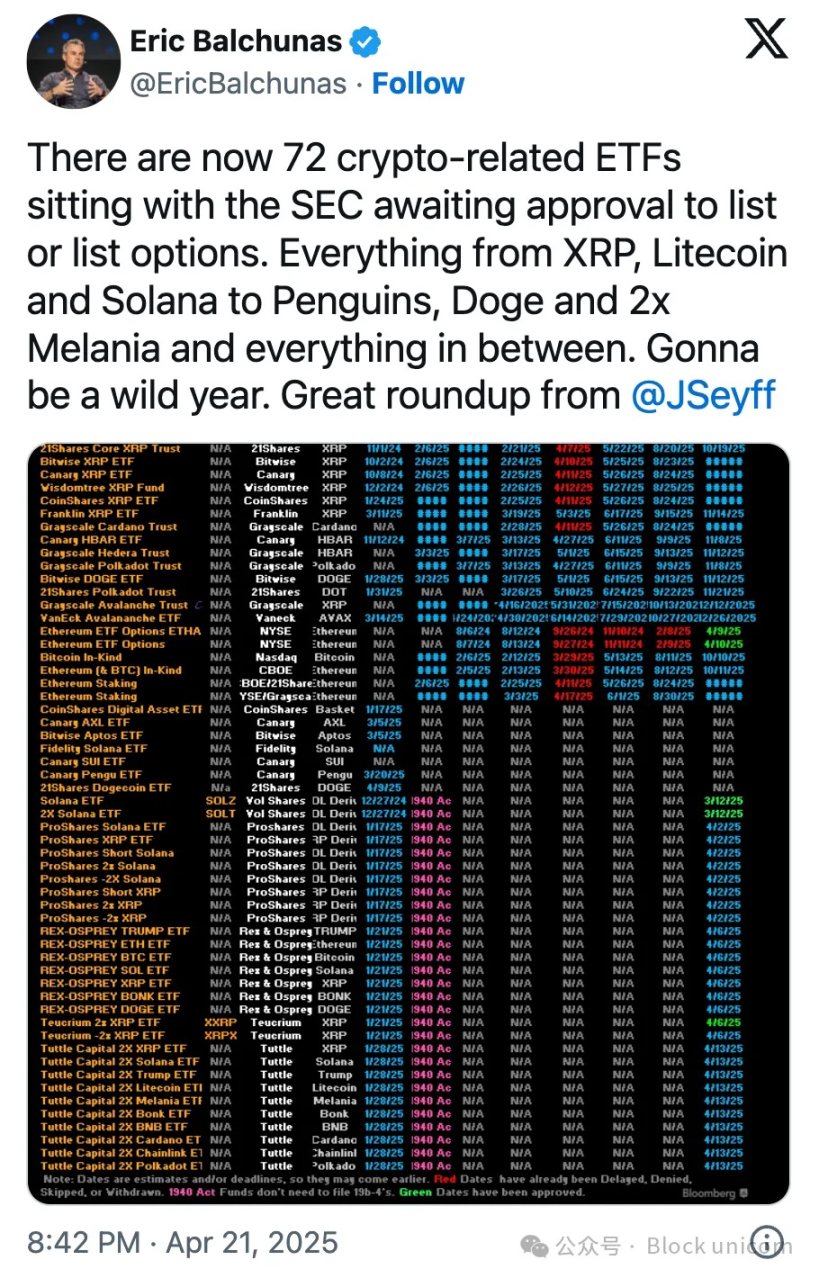

On January 11, 2024, the spot Bitcoin ETF began trading on Wall Street. About six months later, on July 23, 2024, the spot Ethereum ETF debuted. Fast forward eighteen months later, and the desk of the U.S. Securities and Exchange Commission (SEC) is filled with applications—72 crypto ETF applications and counting.

From Solana to Dogecoin, Ripple (XRP) and even PENGU, asset managers are racing to package every possible digital asset into regulated products. Bloomberg analysts Eric Balchunas and James Seyffart put the probability of approval for most applications at "90% or higher," suggesting we are about to witness the largest expansion of crypto investment products in history.

2024 is nothing like 2025. Back then it was a hard fight for recognition, now everyone wants a piece of the action.

Bitcoin's $107 billion fortune

To understand why altcoin ETFs are important, you first need to understand that the success of spot Bitcoin ETFs has far exceeded expectations. They have rewritten the entire playbook for asset management.

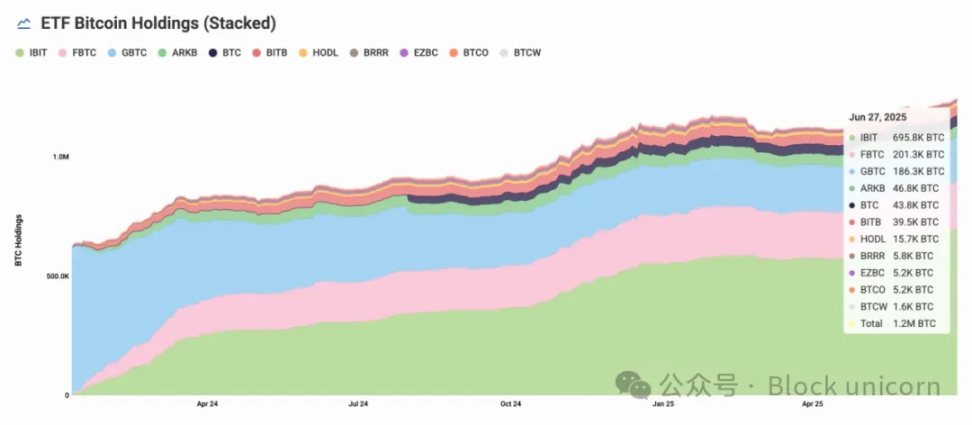

Within a year, the Bitcoin ETF attracted $107 billion, becoming the most successful ETF launch in history — and 18 months later, assets reached $133 billion.

BlackRock’s IBIT alone holds 694,400 bitcoins worth more than $74 billion. All ETFs combined control 1.23 million bitcoins — about 6.2% of all circulating supply.

When BlackRock’s Bitcoin ETF amassed $70 billion in assets faster than any fund in history, what did it prove? The demand for crypto exposure through traditional investment vehicles is real, huge, and under-tapped. Institutions, retail investors, just about everyone is lining up.

This success created a feedback loop that proved the concept: As ETFs siphoned Bitcoin supply, exchange trading balances fell. Institutional holdings accelerated. Bitcoin price stability improved. The entire cryptocurrency market gained unprecedented legitimacy. Institutional money continued to flow in, even during market volatility. These were not day traders or retail speculators, but pension funds, family offices, and sovereign wealth funds that viewed Bitcoin as a legitimate asset class.

Such is the success that as of April, there were approximately 72 altcoin applications lined up at the SEC.

Why do we need ETFs?

You can buy altcoins on crypto exchanges, so what is the use of ETFs? The core of market operation lies in mainstream acceptance. ETF status is a milestone for cryptocurrencies.

This legality allows them to exist on traditional stock exchanges under existing financial regulations. Crypto ETFs allow investors to buy and sell digital assets like stocks through regular brokerage accounts.

This is a lifesaver for retail investors who mostly don’t understand how cryptocurrencies work. There’s no need to set up a wallet, protect private keys, or deal with the technical details of blockchain. Even if you overcome the wallet hurdle, the risks remain – hacks, lost private keys, and exchange crashes. ETFs have custody and security managed on behalf of investors and offer highly liquid assets traded on major traditional exchanges.

Altcoin Gold Rush

These applications reveal what the future holds. Major institutions such as VanEck, Grayscale, Bitwise, and Franklin Templeton have submitted applications for the Solana ETF, with a 90% chance of approval. Nine independent issuers also want to compete for SOL, including newcomer Invesco Galaxy, whose proposed ticker is QSOL.

The Ripple (XRP) application followed closely behind, with multiple applications filed for the payments-focused cryptocurrency. ETFs for Cardano, Litecoin, and Avalanche are also under review.

Even memecoins are no exception. Major issuers have submitted ETFs for Dogecoin and PENGU.

“I’m surprised we haven’t seen a Fartcoin ETF application yet,” said Bloomberg’s Eric Balciunas on X.

Why is this happening now? It’s the result of a confluence of forces that have created the perfect environment for altcoin ETFs to proliferate. The Trump administration’s friendly approach to cryptocurrencies marks a dramatic shift in regulation, with new SEC Chairman Paul Atkins doing away with Gary Gensler’s “regulation through enforcement” approach and establishing a crypto task force to create clear rules.

The culmination of this regulatory thaw was the SEC’s recent clarification that “protocol staking activity” does not constitute a securities offering — a stark reversal of the previous administration’s aggressive pursuit of staking providers like Kraken and Coinbase.

Institutional recognition of Bitcoin and altcoins, combined with the craze for corporate cryptocurrency reserves and Bitwise research showing that 56% of financial advisors are now willing to allocate crypto assets, has created unprecedented demand for diversified crypto exposure beyond Bitcoin and Ethereum.

Economic reality check

While Bitcoin ETFs have demonstrated significant institutional demand, early analysis suggests that altcoin ETFs will have a very different take-up.

Katalin Tischhauser, head of research at Sygnum Bank, expects total inflows into altcoin ETFs to reach “hundreds of millions to $1 billion” — far below Bitcoin’s $107 billion achievement.

Even by the most optimistic estimates, total inflows into altcoin ETFs are less than 1% of what Bitcoin has achieved. This makes economic sense from a fundamental perspective.

Ethereum’s performance further highlights this disparity. Despite being the second-largest cryptocurrency, Ethereum’s ETF has attracted only about $4 billion in net inflows in 231 trading days—just 3% of Bitcoin’s $133.3 billion achievement. Even with an additional $1 billion in inflows in the last 15 trading days, Ethereum’s institutional appeal is still far less than Bitcoin’s, indicating that altcoin ETFs face a tougher challenge in attracting investor attention.

Bitcoin benefits from first-mover advantage, regulatory clarity, and a “digital gold” narrative that is easily understood by institutions.

Now, 72 applications are chasing a market that may only support a few winners.

Staking changes the rules of the game

One difference between altcoin ETFs and Bitcoin ETFs is that they earn returns through staking. The SEC’s staking approval opens the door for ETFs to pledge their holdings and distribute returns to investors.

Ethereum staking currently yields an annualized rate of return of between 2.5% and 2.7%. After deducting ETF fees and operating costs, investors may receive a net rate of return of 1.9% to 2.2% - not high by traditional fixed income standards, but significant when combined with potential price appreciation.

Solana staking offers similar opportunities.

This creates a new revenue model for ETF issuers and a new value proposition for investors. Instead of simply providing price exposure, pledged ETFs become yield-generating assets that can justify their fees while providing passive income.

Several Solana ETF applications explicitly include staking clauses, with issuers planning to stake 50-70% of their holdings while retaining liquidity reserves. Invesco Galaxy’s Solana ETF application specifically mentions the use of “trusted staking providers” to generate additional returns. But staking will increase operational complexity.

ETF managers who manage staked crypto assets face multiple challenges: they must balance keeping enough unstaked and liquid assets to meet investor redemptions while staking as much as possible to maximize returns. They also need to manage the risk of "slashing," which is the potential loss of funds if validators (nodes that help protect the network) make mistakes or break the rules. Running validators requires technical expertise and reliable infrastructure to ensure everything goes smoothly and securely. Therefore, it is not an easy risk to manage. Managing a staked crypto ETF is a complex balancing game. While not impossible, it is very difficult to operate.

For the Bitcoin and Ethereum ETFs that have been approved and launched, staking was not an option because the SEC, led by Gary Gensler, believed that staking violated securities laws and constituted an unregistered securities offering. This is no longer the case.

Cost compression is coming

The flood of applications all but guarantees fee compression. When 72 products compete for limited institutional money, pricing becomes the primary differentiator. Traditional cryptocurrency ETFs charge management fees of 0.15-1.5%, but competition could drive those fees down.

Some issuers may even use staking income to subsidize management fees and launch zero-fee or negative-fee products to attract assets. The Canadian market provides a precedent: several Solana ETFs waived management fees in their initial stages.

This fee compression is good for investors, but it also puts pressure on issuer profitability. Only the largest and most efficient operators will survive the inevitable consolidation. Expect mergers, closures, and transformations as the market sorts out winners and losers.

Our View

The craze for altcoin ETFs is changing the way people think about crypto investing.

Bitcoin ETFs have been a huge success. Ethereum ETFs offer a second option, but adoption has been tepid due to complexity and disappointing returns. Now, asset managers see different cryptocurrencies as having different uses.

Solana became a speed investment, XRP became a payments investment, Cardano sold itself on “academic rigor”, and even Dogecoin was seen as a mainstream adoption story. If you’re building a portfolio, this makes sense. Cryptocurrencies are no longer one weird asset class, but dozens of investments with different risk profiles and use cases.

Bitcoin, the largest cryptocurrency by market capitalization, has become an extension of the traditional portfolio for many regular investors who already participate in the stock market. For these investors, Bitcoin is seen as a complementary asset class that provides diversification and a hedge against market uncertainty. In contrast, Ethereum has not achieved the same mainstream integration. Despite being the second largest cryptocurrency, most retail and institutional investors do not consider Ethereum ETFs as a core part of their portfolios.

We need to see what differences altcoin ETFs will offer to avoid repeating the mistakes of the Ethereum ETF.

But it also shows how far crypto has strayed from its roots. When memecoins get ETF applications, when 72 products vie for attention, and when fees are compressed like any other commodity business, you are witnessing the complete mainstreaming of an industry.

The question is whether this is creating real value or just speculation wrapped in a regulatory veneer. It may depend on your perspective. Asset managers see new revenue streams in a crowded market. Investors gain easy crypto exposure through familiar products.

The market will decide who is right.